This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Throughout 2017, our meetings and conversations with clients very frequently focused on the topic of risk. While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Fri, 03/30/2018 - 11:57.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is not particularly notable.

Thu, 06/01/2017 - 02:47. Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. stocks as of the end of 2015 on an EV/EBITDA basis; that gap widened to 20% by the end of April 2017.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks. In non-U.S.

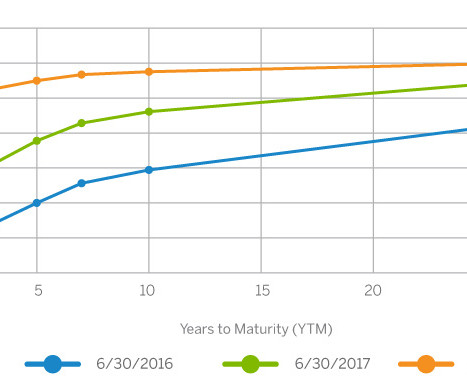

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. In the U.S.,

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. In the U.S., Risks in Bonds.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. That’s actually research that was done by JP Morgan as of 2017. Now my observation was twofold.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy.

The most egregious example appears to be in 2015 (green line) when the Committee expected interest rates in 2017 to be above 3.5%, when in actuality they were closer to 0.50% that year. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from FactSet.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

EOG is poised to breakout and trades at bargain valuation of about nine times earnings (relative to the S&P at 23 times earnings and a touch under the overall energy sector of 12 times earnings). That said, it loses early in round one simply due to us believing it’s close to full valuation and due for a breather.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Source: BLOOMBERG.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Source: BLOOMBERG.

ESG and the Stock-Picker’s Dilemma achen Fri, 09/22/2017 - 12:58 One of the greatest challenges that public equities investors face to integrating environmental, social, and governance (ESG) data into their decision making is the lack of proof that real – not hypothetical – investment strategies can use ESG factors to enhance performance.

Fri, 09/22/2017 - 12:58. Research firms lack standardization on the ESG issues they cover and the systems they use to quantify those issues into a score or rating for a company (Bose and Springsteel, 2017). ESG and the Stock-Picker’s Dilemma. Though a relationship may exist it can be difficult to show correlation through the noise.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. Reasons for this tendency are varied. In short, every situation is different.

Wed, 06/21/2017 - 12:35. On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations.

And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from assetvaluation. I mean the valuation is the future cash flow discounted at a risk-free rate plus a risk premium. But I would add, we had just gone public at the time, 2017.

In June 2017, Dent predicted a “ once in a lifetime ” crash in the stock market, the economy, and in real estate over the following three years. 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.” 2020 : “[E]xtreme valuations.

Investment Perspectives | “Undoing” the Fed’s Balance Sheet achen Tue, 11/14/2017 - 16:18 These days, it seems like all eyes are on the Federal Reserve. Meanwhile, we continue to focus on security selection. the broad markets are largely efficient. A number of thoughts are swirling in the wake of these policy and leadership shifts.

Tue, 11/14/2017 - 16:18. While this shift in monetary policy may ultimately have important implications for assetallocation and other investment decisions, we’re not convinced that its near-term impact will be particularly significant. Investment Perspectives | “Undoing” the Fed’s Balance Sheet.

And it’s funny ’cause that was a pandemic purchase, a very inexpensive 2017 Panama four s, which everybody walked away. He wasn’t tactical assetallocator. It’s about long-term planning and strategic assetallocation and, and just understanding how markets work and how behavior comes into the mix.

Outlook for 2017 | Balance in an Uncertain Time achen Fri, 02/03/2017 - 14:19 With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. Provide our assetallocation perspective as it stands at the beginning of 2017—also based on a longer-term view.

Outlook for 2017 | Balance in an Uncertain Time. Fri, 02/03/2017 - 14:19. With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. Provide our assetallocation perspective as it stands at the beginning of 2017—also based on a longer-term view.

And one of the worst performing factors has been valuation. So we’re now in an environment where all the 45-year-old portfolio managers out there have been, have worked their entire careers in these momentum fueled markets, and they’ve been trained to believe that valuation doesn’t matter.

00:21:21 [Speaker Changed] So this story came out that, oh, value is defensive because it has this valuation buffer to it 00:21:28 [Speaker Changed] In that one example. Most clients, whether they’re individuals or institutions, have some sort of benchmark, a policy portfolio, some strategic assetallocation that they start with.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content