This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

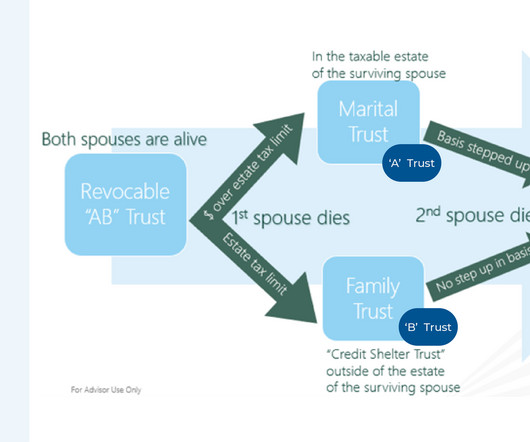

In recent years, the Internal Revenue Code (IRC) has endured some drastic changes resulting from legislative action that have altered the strategies estateplanning professionals have recommended to clients. For instance, prior to the 2017 Tax Cuts and Jobs Act (TCJA), "A/B trusts" had become ubiquitous for spousal estate tax planning.

Petersen, CPA, CFP ® , CP, Affluent Wealth Planning The holidays are upon us! That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA).

That occasion marked an agreement with the IRS on a $156 million value on Prince’s real estate and recordings for the artist who died in April 2016—without a will. What can we learn from celebrity estateplanning disasters like this? Such cautionary tales prove the value of proper planning. It turns out, plenty.

Accordingly, just as I did last year, and in 2020, 2019, 2018, 2017, 2016, 2015, and 2014, I've compiled for you this Highlights List of our top 20 articles in 2022 that you might have missed , along with a few of our most popular episodes of ‘Kitces & Carl’ and the ‘Financial Advisor Success’ podcasts.

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. For average earners or those with modest-sized estates, doing so will not create a federal estate tax event for their estate or inheritors. .

covers some of the top estateplanning trends that tax advisors should be tracking during the second half of 2024. Now that the mid-point of 2024 has passed, we are faced with an environment where little has changed with respect to the wait-and-see posture of estate and wealth transfer planning. citizens and residents.

2017 Year-End Planning Letter. Mon, 12/04/2017 - 13:10. The outcome of the tax reform debate is likely to impact how we advise clients on tax planning, estateplanning and a host of other topics. We are closing 2017 with nearly the same stance as last year. Spotlights for Prudent Planning in 2017.

It’s a simple, human act – one that seems like it shouldn’t take too much planning to do it correctly. What do you need to consider about gifting as it relates to your overall estateplan? Let’s take a closer look at estate and gift taxes and how you can approach them with a financial planning mindset.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. At that point, many provisions will revert to 2017 levels, adjusted for inflation. For example, in 2017, the marginal tax brackets were 10%, 15%, 25%, 28%, 33%, 25%, and 39.6%.

Brought to you exclusively by NAIFA and the Society of FSP, this essential webinar delves deep into the time-sensitive implications of provisions in the Tax Cuts and Jobs Act (TCJA) of 2017 that are scheduled to sunset by 2025.

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Tax season has begun, and it’s not too early to think about planning for the 2023 tax year. One strategy is to accumulate deductions that a client would normally take over 2 years into a single year.

If you’ve already maxed out a 401(k) and IRA, you may also wish to explore investing in a health savings account (HSA) provided you have a qualifying high-deductible health plan. The exclusion may reduce back to pre-2017 levels of $5M after 2025. Estateplanning. if you are married filing jointly). at the federal level.

2019 Year-End Planning Letter. Each year, we send a letter to clients to help guide year-end planning discussions and to offer ideas for them to consider with their other advisors. Market conditions may be volatile, but our planning efforts are, as always, focused on stability and consistency. Fri, 11/01/2019 - 13:44.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. But tax planning isn’t just for your investments.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . But tax planning isn’t just for your investments.

2018 Year-End Planning Letter. Each year, we send a letter to clients to help guide our year-end planning discussions with them and to offer ideas for them to consider with their other advisors. As we discuss below, the new tax law offers a number of opportunities for adjusting long-term plans. Wed, 11/28/2018 - 08:38.

Here are a few more reasons to apply it in your financial planning practice. So, how can you leverage gratitude in your financial planning practice? To continue learning about how to apply financial psychology in your practice, read our guide to Tapping into the Emotional Side of Financial Planning. Sources: 1. Emmons, Robert.

When those changes involve tax law, it is extremely important for clients to meet with their financial professional, tax advisor, and legal advisor to discuss any adjustments that may need to be made to their financial, retirement, or estateplan.

When those changes involve tax law, it is extremely important for clients to meet with their financial professional, tax advisor, and legal advisor to discuss any adjustments that may need to be made to their financial, retirement, or estateplan.

Whether you’re building equity in a primary residence or buying a vacation home or investment property, understanding how to best prepare for, and manage, a real estate purchase is a critical piece of any personal financial plan. and Financial Planning for EstatePlanning.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. At that point, many provisions will revert to 2017 levels, adjusted for inflation. For example, in 2017, the marginal tax brackets were 10%, 15%, 25%, 28%, 33%, 25%, and 39.6%.

Strategic Planning in Volatile Markets ajackson Wed, 04/01/2020 - 09:31 Our conversations with clients usually cover topics that range beyond investment and financial affairs. Possible future increases in income and wealth transfer taxes, including the potential reversion of certain elements of the U.S. tax code that are not permanent.

Strategic Planning in Volatile Markets. Of course, given the market volatility that has accompanied this outbreak, we are also reviewing where we stand in relation to the goals we are helping you pursue and the plans we have helped you implement. Wed, 04/01/2020 - 09:31. tax code that are not permanent.

Strategic Advisory Letter | 2015 Year-End Planning Checklist. As 2015 comes to a close, we remind our clients and friends of how important it is take time to review new tax rules, consider tax-saving opportunities and review investment and asset-protection plans before year’s end. Thu, 11/12/2015 - 11:10.

I help my dad with his finances and pay his bills, but especially over the last couple of years, he has been increasingly forgetful and makes impulsive decisions that aren’t part of MY plan! Well, it used to be our plan, but he often doesn’t remember. This is a great reminder to take a breath and focus on communication.

Will you end up paying too much in ordinary income taxes for company stock in your 401(k) plan? With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirement planning. This appreciation becomes critical when considering tax implications upon withdrawal.

Retirement contributions Individuals can take advantage of various tax-related retirement planning strategies to reduce their taxable income today and post-retirement. Health Savings Accounts (HSAs) HSAs are available to individuals enrolled in high-deductible health plans (HDHPs).

Family Wealth Transfer Options achen Mon, 10/16/2017 - 10:49 Families can use a variety of strategies to reduce their estate tax burden. By using various exemptions and exclusions, you can gift a certain amount of assets to your family members without triggering gift taxes, thereby reducing the size of your taxable estate.

Mon, 10/16/2017 - 10:49. Families can use a variety of strategies to reduce their estate tax burden. By using various exemptions and exclusions, you can gift a certain amount of assets to your family members without triggering gift taxes, thereby reducing the size of your taxable estate. Family Wealth Transfer Options.

The HNI population in India has grown at a Compound annual growth rate(CAGR) of 21% from 2017 to 2022. The company also provides holistic services like estateplanning and succession planning without charging clients. There has been an increase in the amount of investments in the Equity Mutual fund, i.e. from 6.7%

Uniting Around a Legacy: Generational Wealth Transfer achen Mon, 02/13/2017 - 14:02 Young investors face a critical set of decision points in their early years of independence. In these situations, clients are best served by a planning approach that carefully considers both their income statement and their balance sheet.

Mon, 02/13/2017 - 14:02. At times, younger clients benefit from the careful planning of their parents; their inherited wealth can come in many forms, such as LLC interests, private equity holdings, or income from family trusts. With a well-vetted business plan, she came to us for guidance on how to proceed.

The idea centered on the concepts of simplicity, keeping total investment costs and taxes extremely low and developing a custom investment plan for each client using low-cost asset class and index funds. James is the father of three energetic boys and 1 Bernadoodle: Oliver, Henry, William, and Louie; and husband to Anya Giles since 2017.

In 2017, the SEC approved the role of trusted contact person as part of a FINRA Rule 4512 amendment. This makes sense, since you may inadvertently name a “bad” player … or others may be able to contest the POA you’ve established. Don’t wait until it’s too late. Trusted Contact Person(s) The Basics.

In 2017, the SEC approved the role of trusted contact person as part of a FINRA Rule 4512 amendment. This makes sense, since you may inadvertently name a “bad” player … or others may be able to contest the POA you’ve established. Don’t wait until it’s too late. . Trusted Contact Person(s). The Basics.

So Nathan pay is a retirement plan consultant, and he’s here today to talk about the experience of being an Edward Jones financial advisor. Okay, everybody. A, welcome to the show. NATE PENHA: Hey, Sarah, thanks for having me.

2020 Year-End Planning Letter. Each year, we send a letter to clients to help guide year-end planning discussions and to offer ideas for consideration with their other advisors. There are issues and uncertainties to consider every year when revisiting one’s plans, but 2020 has been a uniquely challenging year on many fronts.

Gift/Estate/GST Tax. An acceleration to 2022 of the rollback of the gift/estate and GST lifetime exemptions from current levels (set in 2017) to the levels under prior law ($5 million exemption indexed for inflation starting in 2010). Corporate Income Tax. An increase of the top corporate tax rate from 21% to 26.5%.

Whats less common, but just as important, is outlining a specific plan for this transfer and updating it as circumstances change. If its been some time since you established your estateplan, you may want to think about giving it a review. How will this affect your overall plan? million.

2016 Year-End Planning Letter. While there will not be any firm proposals until 2017 at the earliest, we will be looking for and analyzing changes that may have an impact on our clients. As we noted in our midyear letter, it is helpful to build long-term plans on a foundation of stable, incremental yearly steps. Takeaways.

However, the $1 million limit still applies to mortgages taken out before December 15, 2017. Contributions to these plans are tax-deductible and can reduce taxable income. In addition to working with a tax professional, there are also online resources available to help freelancers and small business owners with tax planning.

What are the changes to 529 plans in 2025? Higher 401(k) contribution limits: Starting in 2025, individuals can contribute up to $23,500 to their 401(k) plans, marking an increase from the 2024 limit of $23,000. This adjustment also applies to participants in 403(b) plans, governmental 457 plans, and the Federal Thrift Savings Plan.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content