This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When you get it wrong, it crushes your retirement plans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. But when they get market timing wrong, they lose subscribers. By Jeff Sommer New York Times, Nov. More on this later.

First, is the math right based on my numbers? I didn't want to backtest too far back because Bitcoin had massive gains in 2017 and 2020 that might not be repeatable. If we guess just 2 billion people, and that is just a guess, and divide that into the 15.2 How can it solve anyone's problem?

Little MM and me self-educating with some Orson Scott Card, way back in 2017. Because of the Internet, and to be honest a damned large dose of privilege due to having two educated parents always available because we were retired before he was even born, he has been able to feed his thirst for knowledge with incredible efficiency.

You still had 2012 to 2017 to finish the bet. RITHOLTZ: So hold the duration risk aside with those two, but just for an investor in treasuries, I know you’ve done the math before. Let’s jump to my favorite questions that I ask all of my guests, some of which I think I’m ready to retire. RITHOLTZ: Right.

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. People earn wages, whether it’s a retirement account or a tax deferred account or just an investment account.

ANAT ADMATI, PROFESSOR OF FIANCE AND ECONOMICS, STANFORD GRADUATE SCHOOL OF BUSINESS: So, my journey starts where I took a lot of math. I was good in math and I love the math. So, I was kind of, in my romantic mind when I was in my early 20s, I was going to take but not give back to math, that kind of thing.

So it may be surprising to hear that a Roth IRA—a vehicle ostensibly intended for retirement income—can be a powerful mechanism for next-generation wealth transfer. Background Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs.

So it may be surprising to hear that a Roth IRA—a vehicle ostensibly intended for retirement income—can be a powerful mechanism for next-generation wealth transfer. Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs.

Quick math: If you have $1.828 million in the bank. And , you have to do the math by hand. 2017, Nov 15). To What If Analysis, what if I pay… So I’m doing my cash flow planning in my retirement plan, and I say, You know, I don’t wanna have to pay for in as a retirement. The Impact of AG49.

Subscribe now Share The Better Letter Get more from Bob Seawright in the Substack app Available for iOS and Android Get the app TRIGGER WARNING: I’m going to do some sports math nerding-out this week. Brady is now retired as a seven-time Super Bowl champion, five-time Super Bowl MVP, 15-time Pro Bowler, and three-time NFL MVP.

I’m good at math and science and you know, I always had an idea what go into business, but I felt that electrical engineering would be a good foundation. You know, I, it always, I I see different numbers all the time, so it’s always kinda like, who’s math if you will? 00:02:16 [Speaker Changed] Me too.

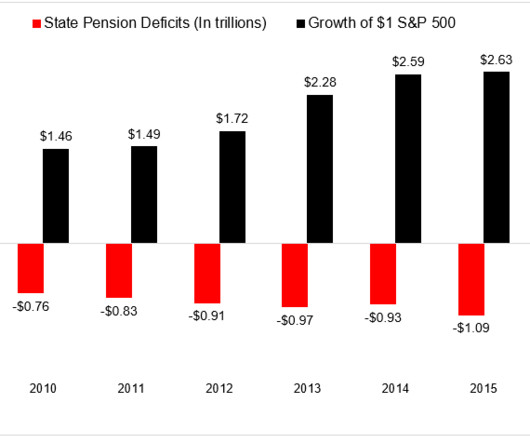

The median retirement account balance of people ages 56 to 61 is just $25,000. Whatever else happened, retired policemen and firefighters and teachers would be paid. workers participate in an employer-sponsored retirement plan. ( If you're curious to learn how the math behind this, read this piece from Econompic.

And we go through long periods, a good example would be post GFC through 2017 where values tough. If you’re anywhere from an individual to a pension fund, saying how much do I have to save to retire? My mom was a math teacher so — RITHOLTZ: Okay. My mom was a math teacher so — RITHOLTZ: Okay.

So, I did the math, 20 million times a hundred. So, let me just repeat the math. And so, again, I went through this simple math. We got it passed in Canada in 2017, in the U.K. And so, it wasn’t just a fishing boat, it was an oceangoing factory, very impressive. How many do you have in your fleet?

So you end up teaching at the University of Missouri, Kansas City for 18 years, from 1999 to 2017. Barry Ritholtz : So what brought you in 2017 to my alma mater, SUNY Stony Brook. Wasn’t the Excel spreadsheet error, which changed their math. And my trajectory changed to economics by accident. That’s right.

RITHOLTZ: So wait, you’re, I’m trying to do the math, if you were 24 in ‘08, so you got this watch in 2000, 99? CLYMER: This is an IWC that we did in 2017. CLYMER: And I guarantee you when I retire from whatever this is, that’s the watch I will wear every day. When I was 16 years old, it was my only nice watch.

And I, and I really like the application of math and statistics and computer science to markets. You learn the math that can help you with, with market making operations. It’s just not smart on a math basis to do that. And I just caught the bug. Become options market makers. You learn the technology.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content