This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The rising cost of healthcare in retirement . According to Fidelity an average couple both aged 65 will spend $300,000 on medical costs in retirement. This is up from $285,000 in 2019, from $275,000 in 2017 and from $220,000 in 2014. The money goes into the account on a pre-tax basis much like a traditional 401(k) or IRA.

A new bill would make many parts of the Tax Cuts and Jobs Act of 2017 permanent, including its changes to tax brackets, the higher standard deduction, and the cap on state and local tax deductions. What advisory firms can do to make the most out of client testimonials and avoid negative reviews on third-party websites.

That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). AGI impacts multiple other tax considerations.

The 2017Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. At that point, many provisions will revert to 2017 levels, adjusted for inflation. For example, in 2017, the marginal tax brackets were 10%, 15%, 25%, 28%, 33%, 25%, and 39.6%.

equity valuations: “Baby-boomers’ huge flow of 401K plan contributions helped to drive equities higher; now that ~70 million Boomers are retiring, when do demographics flip this from a huge positive to a net drag?” This demographic cohort is simply not a seller due to retirement – the tax expenses would be too great.

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. When you get it wrong, it crushes your retirementplans. Let’s add some color to the discussion on timing itself and add a little nuance.1

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. One of the Roth IRA’s most compelling features?

Where Sam writes about FIRE, he asked Bengen what a safe withdrawal rate would be for someone who retired, planning to need the money to last for 50 years instead of the typical 30 used for planning purposes. I took the above picture in 2017. The answer is no but I feel like there's a lesson in here somewhere.

The 2017Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. At that point, many provisions will revert to 2017 levels, adjusted for inflation. For example, in 2017, the marginal tax brackets were 10%, 15%, 25%, 28%, 33%, 25%, and 39.6%.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. Life happens. You buy a business.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . Tax-Planning Possibilities.

FINANCIAL PLANNINGTax and Financial Planning Ideas For 2023 Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Additionally, the government has made changes to tax rules, further prompting Americans to reevaluate their tax and financial strategies. Retirement Savings Accounts .

As a company founder, early startup employee, or small business owner, you may find yourself in a higher tax bracket as your business grows or you realize gains from equity compensation. But that doesn’t mean you simply have to accept a higher tax bill. Here are 20 tax-efficient actions to consider when filing your taxes in 2024.

Yep, it’s about that time—tax time, of course. . The sun’s out a little longer, we shed a few layers, the first blooms of the season are on full display, and taxes are due smack dab in the middle of it all. This year, your 2021 taxes are due on April 18th, 2022. This year, let’s make taxes fun! Let’s take a look.

You can see in 2017, the blue line for Cockroach with Bitcoin went parabolic. 2020 was also a very good year for Portfolio 1 thanks to Bitcoin but it wasn't as big as 2017. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

I bought 100 shares on its first or second day of trading last fall for $2017 and I sold it today for $2114 which includes reinvesting the dividends. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

For example, as reported by Dimensional Fund Advisors, $1 invested in the S&P 500 Index from 1926–2017 would have grown to $533 worth of purchasing power by the end of 2017, after adjusting for Inflation. Unfortunately, we believe such substitutes detract from effective retirementplanning.

We believe that the current environment offers a number of strategic planning opportunities to improve your financial plan, enhance wealth transfers to heirs or charities, minimize the impact of income taxes and broadly help you advance your progress toward long-term goals. tax code that are not permanent.

We believe that the current environment offers a number of strategic planning opportunities to improve your financial plan, enhance wealth transfers to heirs or charities, minimize the impact of income taxes and broadly help you advance your progress toward long-term goals. tax code that are not permanent.

A point we've made many times here is that no matter what your goal is/was or what someone or some website calculator once told you that you need to retire, once you get to retirement age, the only thing that matters is how much you have at that time. Working backwards, $1.8 We went through this exercise recently.

It only goes back to 2018 because in 2017, Bitcoin went up an amount that may not be repeatable. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Portfolios 1 and 3 both concentrate the risk into narrow slices of the portfolio.

SRRIX lost -11.35% in 2017, -6.14% in 2018 and -4.47% in 2019." They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. It is an unusual exposure, I am not aware of any other funds that are just reinsurance but if you know otherwise please comment.

was signed into law December 29th, 2022, bringing more major changes to tax law. Here are the top five Roth-related retirement changes following the passing of Secure Act 2.0. 529 plan to Roth IRA rollovers. The individual must be the designated beneficiary of the 529 plan and move funds to a Roth IRA in their name.

Trade Brains was founded by Kritesh Abhishek, an NIT Warangal graduate, in Jan 2017. You can read a number of interesting articles regarding stock investing, mutual funds, real estate, income tax, personal finance, etc on this blog. 8 Best Indian stock market Blogs to Follow. Trade Brains. Get Money Rich (GMR). Dr. Vijay Malik.

Strategic Advisory Letter | 2015 Year-End Planning Checklist. As 2015 comes to a close, we remind our clients and friends of how important it is take time to review new tax rules, consider tax-saving opportunities and review investment and asset-protection plans before year’s end. Thu, 11/12/2015 - 11:10.

The iShares Momentum ETF (MTUM) outperformed only one of those four, in 2017. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Intuitively you might think that momentum would outperform when the S&P 500 is up a lot.

The Invenomic Institutional Fund (BIVIX/BIVRX) is a long/short equity fund that has been around since mid-2017. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

Bond investing and interest rates (again) : You may recall, interest rates did tick upward in 2017–2018, creating concerns similar to those we’re hearing today. in 2017, outperforming the Vanguard Intermediate-Term Treasury Index ETF (VGIT), which returned 1.7% and the Vanguard Short-Term Treasury Index ETF (VGSH), which returned 0.0%.

According to the most recent 2017 Census of Agriculture, the average age of a U.S. Those numbers make it clear that farmers are generally not retiring at age 65. These are all various retirement savings vehicles with the added benefit of allowing them to defer current income taxes. farmer is approximately 57.5

I could have gone back further than 2018 but Bitcoin skyrocketed in 2017 so I wanted to take that out in case that sort of year never repeats again. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

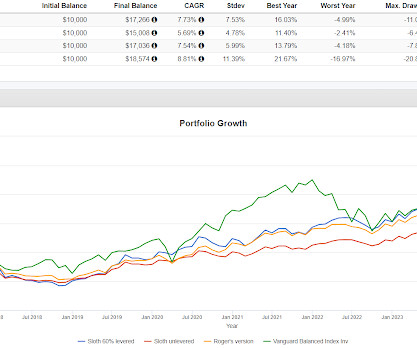

TAIL is the newest fund but goes back to 2017 so we get a decent backtest. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. First up is the allocation of The Sloth. BTAL is a client and personal holding.

Yeah, that lot that talks about terms like compounding, risk profile, returns, retirementplanning, budgeting, Investing, and whatnot! Top Mutual Funds For SIP #2 – IDFC Tax Advantage (ELSS) Direct Plan-Growth Fund Company IDFC Asset Management Company Ltd Size (AUM in Cr) 4,033 3-yr returns (CAGR) 22.56

I didn't want to backtest too far back because Bitcoin had massive gains in 2017 and 2020 that might not be repeatable. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Even the gain in 2023 might not be repeatable but it's the best we can do.

I swapped in the Merger Fund because it backtests a full ten years versus Absolute Convertible Arbitrage which only goes back to 2017. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. And an updated 60/10/10/10/10.

The maximum amount of earnings subject to Social Security tax (taxable maximum) will increase to $176,100 from $168,600. The individual tax brackets for ordinary income have been adjusted by inflation. On average, tax parameters that are adjusted for inflation will increase about 2.80%.

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

in Financial and Retirement Income Planning from The American College of Financial Services, where he was named the Sievert-Sternberg Doctoral Research Fellow, and is currently pursuing a Doctor of Criminal Justice degree from Northcentral University. 2017, January 18 th ). Lee holds a Ph.D. link] Schnase, Lorna A.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing.

Wed, 06/21/2017 - 12:35. We understand and appreciate this approach, which is particularly common among endowments, foundations and retirementplans for which tax considerations are not relevant. Investment Perspectives - The Great Debate.

Even if a client believes they would not be subject to estate or gift tax under current law, you may want to re-examine the value of their assets to determine whether they exceed a lower exemption amount. Tax season has begun, and it’s not too early to think about planning for the 2023 tax year.

The maximum amount of earnings subject to Social Security tax (taxable maximum) will increase to $168,600 from $160,200. More Information If you would like to read more about the 2024 changes from the IRS here is the IRS Publication and summary at the Tax Foundation website.

A Contributory IRA, otherwise known as a traditional IRA , is a retirement savings account that allows individuals to make contributions from their earned income. The contribution limit may be reduced or eliminated for individuals who have high incomes or who participate in an employer-sponsored retirementplan.

Opening a Roth IRA can be a smart move if you want to invest for retirement and save money on taxes later in life. Contributions to a Roth IRA are made with after-tax dollars, which means your money can grow tax-free. You can also contribute to your IRA up until tax day of the following year. Fund Distributions.

By Ryan Egolf, EA, Senior Tax Planner As the New Year quickly approaches, it’s time to put a bow on your 2023 financial plan. In some cases, those payments are tax-free. Check into your employer’s short- and long-term disability plans, as they are usually the most affordable options.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content