This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Saving for retirement is a major undertaking for most of us. Health savings accounts (HSA) provide another vehicle to save for retirement. Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. The rising cost of healthcare in retirement .

A new bill would make many parts of the Tax Cuts and Jobs Act of 2017 permanent, including its changes to tax brackets, the higher standard deduction, and the cap on state and local tax deductions. What advisory firms can do to make the most out of client testimonials and avoid negative reviews on third-party websites.

Recall last week , we were discussing thinking about the impact of retiring Baby Boomers on the equity markets and of rising rates on housing. The demographic question touches on a big issue: $6 trillion dollars in 650,000 (401k) retirementplans held by 10s of millions of Americans. appeared first on The Big Picture.

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. But when they get market timing wrong, they lose subscribers.

One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). Many states also exempt retirement income, which may include Social Security. million range for not utilizing the current exemption amount before it reverts to the 2017 inflation adjusted amount.

The 4% rule is generally the accepted standard for a safe withdrawal rate in retirement to ensure the assets last for 30 years. Bengen retired as a financial advisor in 2013 but he also considers himself a researcher. He basically ran the numbers for someone retiring in 1926 and then each each up into the 1970's.

More Generation X retirement doom today from both Bloomberg and Yahoo. million for retirement which is up from $1.7 To the idea of a goal for retirement savings, I've never had one. If you are at least 50, I think it is reasonable to have some understanding of what your expenses are likely to be once you hit retirement age?

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. At that point, many provisions will revert to 2017 levels, adjusted for inflation. For example, in 2017, the marginal tax brackets were 10%, 15%, 25%, 28%, 33%, 25%, and 39.6%.

According to the most recent 2017 Census of Agriculture, the average age of a U.S. Those numbers make it clear that farmers are generally not retiring at age 65. Yet even though many farmers lack a “plan” for retirement in the traditional sense, farmers still need the help of financial professionals.

For example, as reported by Dimensional Fund Advisors, $1 invested in the S&P 500 Index from 1926–2017 would have grown to $533 worth of purchasing power by the end of 2017, after adjusting for Inflation. What If You’re Retired? Unfortunately, we believe such substitutes detract from effective retirementplanning.

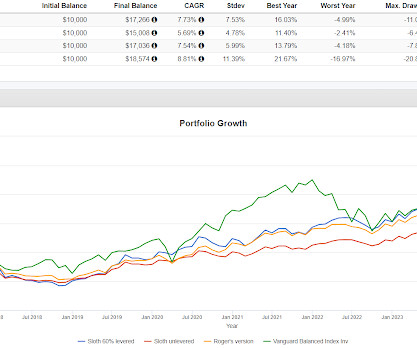

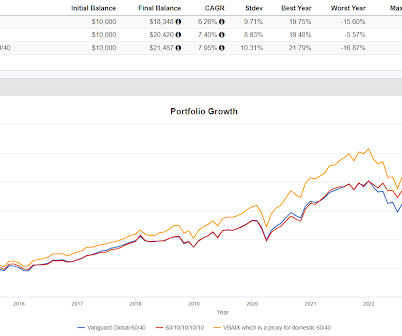

In 2017, as assembled, The Cockroach Portfolio went up 62% versus 21% for 100% SPY and 13% for VBAIX. Note 2017 was even better for Cockroach so the returns are lumpy. That 62% gain, primarily from 4% to GBTC does a lot of heavy lifting for the entire period studied. Interesting that the standard deviation isn't higher.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. At that point, many provisions will revert to 2017 levels, adjusted for inflation. For example, in 2017, the marginal tax brackets were 10%, 15%, 25%, 28%, 33%, 25%, and 39.6%.

You can see in 2017, the blue line for Cockroach with Bitcoin went parabolic. 2020 was also a very good year for Portfolio 1 thanks to Bitcoin but it wasn't as big as 2017. It is important to understand how that happened though. You can see, other than those two years, Portfolio 1 was very unremarkable.

Retirement Savings Accounts . In 2023, Internal Revenue Service (IRS) will increase the contribution limit for multiple types of retirement accounts, including: . For those participating in 401(k), 403(b), and most 457 plans, the limit has risen to $22,500. It can also be helpful to consider your age. Health Savings Accounts .

I bought 100 shares on its first or second day of trading last fall for $2017 and I sold it today for $2114 which includes reinvesting the dividends. First, an update on my test drive of the Defiance NASDAQ 100 Enhanced Option Income ETF (QQQY).

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

Allocate a significant portion of any new wealth to tax-sheltered retirement accounts. Ideally, your succession plan has been in place for years prior, to position your business for a tax-efficient transfer. You retire. You decide to work part-time in retirement. You receive a financial windfall, such as an inheritance.

Allocate a significant portion of any new wealth to tax-sheltered retirement accounts. Ideally, your succession plan has been in place for years prior, to position your business for a tax-efficient transfer. You retire. . You decide to work part-time in retirement. Ditto for those executive compensation benefits.)

It only goes back to 2018 because in 2017, Bitcoin went up an amount that may not be repeatable. Since CAOS hasn't had a real test of going up in a serious decline, if we replace it with more T-bills to get a longer backtest, the results are similar. Portfolios 1 and 3 both concentrate the risk into narrow slices of the portfolio.

Retirement contributions Individuals can take advantage of various tax-related retirementplanning strategies to reduce their taxable income today and post-retirement. By working with a tax professional, you can apply tax strategies to reduce your taxable income or defer paying taxes.

Trade Brains was founded by Kritesh Abhishek, an NIT Warangal graduate, in Jan 2017. Stable Investor also provides various financial services like financial planning, retirementplanning, children’s future planning, etc. 8 Best Indian stock market Blogs to Follow. Trade Brains. Dr. Vijay Malik.

Bond investing and interest rates (again) : You may recall, interest rates did tick upward in 2017–2018, creating concerns similar to those we’re hearing today. in 2017, outperforming the Vanguard Intermediate-Term Treasury Index ETF (VGIT), which returned 1.7% and the Vanguard Short-Term Treasury Index ETF (VGSH), which returned 0.0%.

SRRIX lost -11.35% in 2017, -6.14% in 2018 and -4.47% in 2019." It is an unusual exposure, I am not aware of any other funds that are just reinsurance but if you know otherwise please comment. He notes " after three strong returns in its first three years (2014-16) came a string of losses.

A lot of the return for Portfolio 1 though came in 2017 when it was up 46% versus 21% for the S&P 500. The Sortino Ratio is impressive and the correlation dropped to 80%. It has the best CAGR of the three with a lower standard deviation than SPY but not VBAIX.

Here are the top five Roth-related retirement changes following the passing of Secure Act 2.0. 529 plan to Roth IRA rollovers. Starting with the 2017 Tax Cuts and Jobs Act, then the 2019 Secure Act 1.0, it’s clear that investors need to be adaptive in tax planning. 5 new changes to Roth accounts in Secure Act 2.0.

Yeah, that lot that talks about terms like compounding, risk profile, returns, retirementplanning, budgeting, Investing, and whatnot! Top Mutual Funds For SIP #4 – HDFC Retirement Savings Fund Equity Plan Direct-Growth Fund Company HDFC Asset Management Company Size (AUM in Cr) 2,659 3-yr returns (CAGR) 23.41

Much of the boost in annualized CAGR comes from huge outperformance of GBTC in 2017 which is important to understand. The CAGR for Portfolio 1 is far superior to the other two and it's standard deviation is only slightly higher than Portfolio 3.

The iShares Momentum ETF (MTUM) outperformed only one of those four, in 2017. Intuitively you might think that momentum would outperform when the S&P 500 is up a lot. From 2015 forward, the S&P 500 was up 20% or more four times. In 2018, the S&P 500 was up 18% and MTUM outperformed and it is outperforming so far in 2024.

The Invenomic Institutional Fund (BIVIX/BIVRX) is a long/short equity fund that has been around since mid-2017. A new, interesting and expensive fund popped up on my radar from something I saw on Twitter, yes I am still calling it Twitter. The fund's literature goes out of its way to note that it only positions in domestic stocks.

For example, the filing dates for reporting foreign gifts and foreign accounts will move from March 15 and June 30, respectively, to April 15 for tax years 2016 and beyond (to be clear, these deadlines won’t change this year, the changes take effect in 2017 for 2016 returns). Accelerate or postpone deductions to maximize tax advantages.

I could have gone back further than 2018 but Bitcoin skyrocketed in 2017 so I wanted to take that out in case that sort of year never repeats again. LFMIX and QGMIX both have very low volatility but are complex funds and complexity has its risks and drawbacks too.

It got a lot of it's return in 2017 likely from Bitcoin. I would also add that Portfoliovisualizer says Cockroach's correlation to the S&P 500 is -0.01 The Cockroach should not be expected to keep up with equities but it sort of has and done so with a very similar standard deviation but no correlation. What gives?

The mortgage interest on your home loan: If you bought your house after December 16, 2017, you can deduct the interest you paid on the first $750,000 of the loan. . You may be able to earn some money on the side, stash it away for retirement, and get a tax break if you’re eligible to invest in a SEP-IRA. Look Into a SEP-IRA.

TAIL is the newest fund but goes back to 2017 so we get a decent backtest. He is big on the ReturnStacked Fund suite but they are all so new that backtesting with them doesn't tell us much but we can replicate them on Portfoliovisualizer and still capture the leverage. First up is the allocation of The Sloth.

I didn't want to backtest too far back because Bitcoin had massive gains in 2017 and 2020 that might not be repeatable. SPBC owns 100% S&P 500 plus 10% in Grayscale Bitcoin Trust (GBTC) so the 10% to SPBC means 1% of that portfolio is in Bitcoin. I used BTCFX in Portfolio 2 to backtest a little further than we could with an ETF.

Helping parents send their kids to college, care for an aging parent and retire with financial independence are literally what gets him up every day. He has presented papers at conferences on topics such as investment fraud, risk management, and retirementplanning. 2017, January 18 th ). Lee holds a Ph.D.

I swapped in the Merger Fund because it backtests a full ten years versus Absolute Convertible Arbitrage which only goes back to 2017. A reader left a comment with a work around combining BND and BNDW so I reran it and compared it to 60/10/10/10/10 as follows going back ten years. And an updated 60/10/10/10/10.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing.

Wed, 06/21/2017 - 12:35. We understand and appreciate this approach, which is particularly common among endowments, foundations and retirementplans for which tax considerations are not relevant. Investment Perspectives - The Great Debate.

The personal exemption for 2025 remains at $0 (eliminating the personal exemption was part of the Tax Cuts and Jobs Act of 2017 (TCJA)) Long-term capital gains rates and brackets: The maximum child tax credit is still $2,000 per qualifying child and was not adjusted for inflation.

Qualified Charitable Distributions (QCDs) Your distributions from your retirementplans are reported on your 1099-R form , but the form doesnt specify how much went to a QCD. The pre-2018 two-year carryback rule generally does not apply to NOLs from tax years ending after December 31, 2017.

So Nathan pay is a retirementplan consultant, and he’s here today to talk about the experience of being an Edward Jones financial advisor. Okay, everybody. A, welcome to the show. NATE PENHA: Hey, Sarah, thanks for having me.

A Contributory IRA, otherwise known as a traditional IRA , is a retirement savings account that allows individuals to make contributions from their earned income. The contribution limit may be reduced or eliminated for individuals who have high incomes or who participate in an employer-sponsored retirementplan.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content