This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S.,

Meaning, you do not get the 8-10% long-term gains without living through a significant number of market events, ranging from cyclical drawdowns to longer secular bear markets, and full-on crashes. 2000-13 : Secular bear market did not make new highs until March 2013 2018 : ~20% pullback as the economy slowed, FOMC hiked.

When putting away for retirement, we often dream about all the things we’ll be able to do with that money – traveling, going out to eat, maybe trying new hobbies. . Of course, there are always the everyday household expenses to account for in your post-retirement budget. 1 It’s a number that just keeps rising, too.

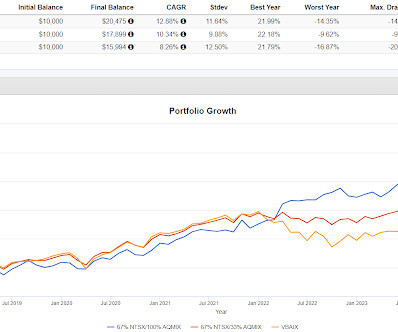

Looking at AQMIX on your statement kind of going nowhere for 10 years could be difficult but clearly a portfolio with the allocation in Portfolio 3 would have kept up just fine and if they had focused on the bottom line number and not the line items, it would not have been difficult. It only back tests to 2018 but here's what you get.

At 50 though, you do need to have some context for how viable your idea of retirement is. That's the number you need to cover. These are all things to incorporate into retirement planning in case every assumption we make at 40 or 50 turns out to be wrong. Do your various, projected income sources cover that?

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. In 2018, the brackets dropped to 10%, 12%, 22%, 24%, 32%, 35%, and 37%. In recent years, a number of states developed a sort of workaround for business owners to navigate the SALT cap.

Ray Dalio, multibillionaire and founder of Bridgewater Associates—the largest hedge fund in the world—retired in October of last year to great fanfare, with much lauding from his and his firm about the transition. In 2018, Bridgewater pledged to shift control of the firm from the founder (Dalio) to top employees. .

So I take that as a good number to study for this blog post. In 2018 you can see that two of them helped with just a few basis points. A year like 2018 constitutes down a little and is probably less important than protecting against down a lot like in 2022. I chose the three alts randomly, only two are part of the AQR filing.

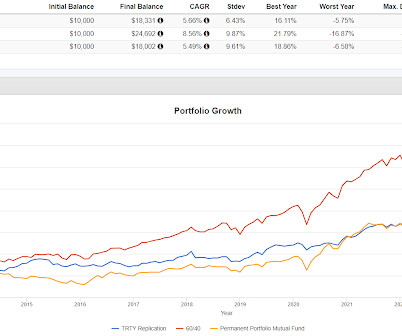

It's growth rate since inception is 3.58% going back to September, 2018 but a lot of that comes from a 15% lift in 2021 (numbers per testfol.io). RPAR is indexed and I think that fund's result shows that risk parity doesn't lend itself to an indexed approach. TRTY is a tough hold.

The 1987 crash was partly attributed to selling portfolio insurance and there was the so called Volmageddon of 2018. 2018 was not 1987 and if there is another event where volatility ends up being a major determent then it will be different than the other two but with some overlap. Events don't repeat but the can rhyme.

In 2018, 52% of all participants at Vanguard were invested in a single target-date fund. In 2018, two out of three new participants were in plans that adopted automatic enrollment. These numbers are pretty encouraging. Six in ten people making more than $150,000 contributed the maximum account in 2018.

Portfolio 3's worst year was 2018 when it fell 7.76%. Portfolio 2 had two years where it was down 5% (those were the worst two) and the leveraged version's worst year was 2018 when it fell 12.26%. The Calmar Ratios for all three are much higher than VBAIX but the kurtosis numbers a slightly inferior.

It's only down year was 2018 with a decline of 7.91%. Both True North portfolios also held up relatively well in the 2020 Pandemic Crash which are the max drawdown numbers in the chart. Despite all the leverage, Portfolio 1 has a very smooth ride including up a lot in 2022.

Do you even remember why stocks crashed in late 2018? There will be future events that result in some sort of drop, black swans to you or not, and these become more important as you get closer to retiring in terms of sequence of return risk. Any retirement plan runs the risk of coming up short for any number of reasons.

Picture retiring in 2010 versus 2020. As we say all the time, whereas stocks are the thing that goes up the most, most of the time in the modern era I would want more than 25% in equities for anyone needing normal stock market growth for their retirement plan to work. There are expectations embedded in these numbers.

Forty years ago, the federal government lengthened Social Security’s full retirement age (FRA) from 65 to 67, and increased the delayed retirement credit. Since 1980 through 2014, workers with retirement plans that included a pension fell from 39% to 13%, a 200% decline. Is it the change we want?

I don't know whether those weightings can vary but the numbers come off the home page for the fund. TRTY only goes back to late 2018 so I build the following to try to replicate it with exposure I believe to be consistent with what TRTY owns. I'd bet that Hussman anecdote from above came from a place of emotion given the timing of it.

It’s one of the best strategies to supercharge your retirement savings, especially for early retirement. There's no time like the present to begin preparing for your retirement. This is always true when neither you nor your spouse are covered by an employer-sponsored retirement plan. Ads by Money.

In 2018, there were approximately 52.4 Some studies also show that by 2034, the number of older adults will outnumber children. Due to the lack of technological know-how in the older generation, many scammers use new-age methods, such as obtaining passwords, account numbers, Social Security numbers, etc.,

I was “The Man Who Retired at 30”, and it was so unusual that it would show up in news headlines all over the place. My story was a nine-year working career, and retirement at 30. So at the end of year one, Curelop’s portfolio looked like this: 2018: Bought a second house for $343,000 ($27k down including some upgrades).

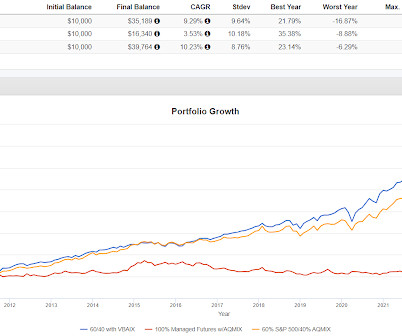

In 2018 the S&P 500 was down a little over 4% and managed futures was down about 8%. Those aren't big numbers so a portfolio that was 80% equities and 20% managed futures that year would have been down 5.4%. But what if the numbers were bigger? Ok, no big deal, it happens. Ok, no big deal, it happens.

In addition, the overall limit on deducting mortgage interest has been reduced to $750,000 for new loans since 2018. Being aware of shifting preferences and needs is especially important if you’re envisioning the second home as a future retirement home. Perhaps you opt to rent the home for the season and travel elsewhere.

He also hosts the Stay Wealthy Retirement Show , which has been ranked on Forbes Top 10 Retirement Podcasts. In 2018, a company even offered to pay him $10 million for his website. Steve Gresham is the CEO of The Execution Project , a consulting firm that helps financial companies rethink “retirement” and get better results.

The numbers for Portfolios 1 and 3 add up to 105% because I am replicating 5% into a 2x bitcoin fund. It only goes back to 2018 because in 2017, Bitcoin went up an amount that may not be repeatable. We'll use CAOS for tail risk and what has more asymmetric opportunity than Bitcoin?

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. In 2018, the brackets dropped to 10%, 12%, 22%, 24%, 32%, 35%, and 37%. In recent years, a number of states developed a sort of workaround for business owners to navigate the SALT cap.

The Trinity Replication captures some of the effect of the market longer term, maybe enough, maybe not enough, you can look at the other post to get more numbers, but that is what real diversification looks like. Also, 2023 it noteworthy. One take away is that nothing can be best for all times. We say that repeatedly here.

The general ideas being explored by a small number of market participants at this point are useful and I think we're going to see a lot more investment products and conversations about these concepts and strategies. Number 2 was to move from market cap weighting to minimum volatility equity exposure. Number 5 is to increase leverage.

In the partial year 2018, the very leveraged version lagged by a lot in a year that was very difficult for managed futures. There's a good chance of getting essentially the same effect with much less risk of being vulnerable to something breaking or at least bending a lot like managed futures in 2018. Closing out with a theory.

The Permanent Portfolio (PRPFX) which purports to be all weather (even if just in design, not sure if they say that in their literature) put in some interesting numbers over the last couple of years. in 2018 when VBAIX dropped 2.8%, not very all weatherish. This year RDMIX is down about 1%. In 2022 it was down 5.5%

If I change the date to start in 2018, the numbers get a little more interesting. It has the best CAGR of the three with a lower standard deviation than SPY but not VBAIX. A lot of the return for Portfolio 1 though came in 2017 when it was up 46% versus 21% for the S&P 500.

The way that number went up though, I don't know if it was a real number or not. The other meaningful monetization was my side gig AdvisorShares which lasted for about four years until 2018. There were articles that may have been written just by Seeking Alpha staff or friends of founder David Jackson.

As baby boomers continue to retire, financial advisors across the country have started targeting the younger generations, Generation X and millennials , to varying degrees of success. According to one recent report , the number of independent broker-dealer firms has been in a steady decline for the past decade, resulting in 819 firms in 2018.

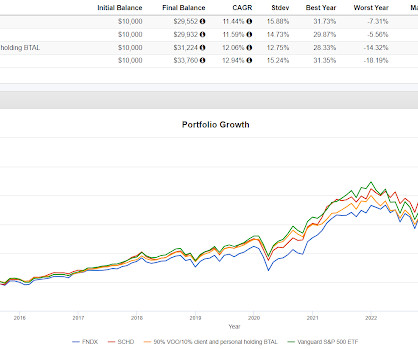

In the mini crash at the end of 2018, FNDX and SPHQ did worse than the S&P 500, SPYV was about the same as market cap weighting and SCHD was the best performer for that event. Looking at the ten year compounding numbers, I wouldn't dismiss any of these, they are all valid, and will capture the effect for the most part.

It briefly went to zero in 2018 and then came right back. If there was some number of shares and the index went to zero but shares still existed then when the index came back, the shares would have value again. Per the above backtest, DSPX went up during market declines including a massive spike during the 2020 Pandemic Crash.

In 2018, Portfolio 1 was down 18.62% while VBAIX was down 2.82% and VOO dropped 4.50%. That was the best way I could figure to back test the idea, ASFYX is a client and personal holding. VBAIX is a proxy for a 60/40 portfolio. The results. Big outperformance obviously but significantly greater volatility. Is the effort worth it?

Those three symbols are the BDCs that were mentioned in the article and I threw levered fund TQQQ in there because the volume number blocked the percentages for the BDCs in comparison the S&P 500. In the Christmas Crash of 2018, two of the three were very similar to the S&P 500 and one did quite a bit worse. Ditto BDCs.

When you buy a bond, you are essentially lending your money to a corporation or a government that is raising money for any number of reasons. The bond will have a price or “face value,” an interest rate, and a set term, which is the number of years you will receive payments. 2 FINRA.org, “Market Cap, Explained” April 26, 2018.

Shifting Generations As baby boomers continue to retire, financial advisors across the country have started targeting the younger generations, Generation X and millennials, to varying degrees of success. Meanwhile, the number of RIA firms has increased from 9,538 to 15,645 over the same time period. Do these numbers excite you?

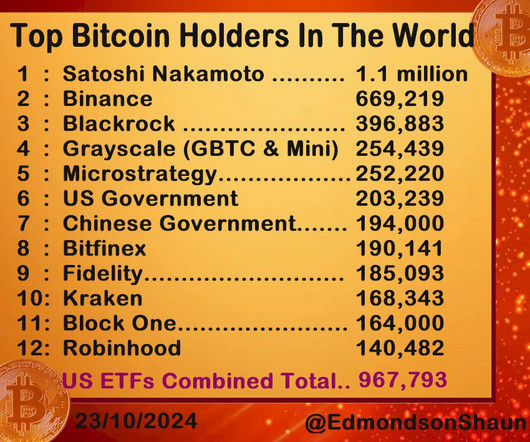

That number is from a Bankrate article I found on a Google search. I'd be curious to hear if anyone else does the same search and finds a different number of lost coins. I had a very lucky purchase in late 2018 and although I have rearranged how/where I own it, I haven't sold. First, is the math right based on my numbers?

The CAGR is close to 60/40, the yellow line, but avoids interest rate risk and worst year/max drawdown numbers are much better than the S&P 500 or 60/40. It's kind of a short/long fund if you will although there have been a couple of stretches since I bought it in 2018 where it has gone up when stocks go up.

Chamber is advocating for—and rallying the business community to push for—federal and state policy changes that will help train more Americans for in-demand jobs, remove barriers to work, and double the number of visas available for legal immigrants. in 2018─2019. And the U.S. available workers per job. Source: St.

DBC also went down in the 2018 Christmas Crash again, taking longer to come back. and that is the number I will assume. ARBIX could be replaced by any number of other funds targeting different strategies toward the same type of result. I imagine the effect there is both stocks and commodities are both pro-cyclical.

There are a number of temporary income tax provisions in the CARES Act that will be of interest to our private clients. If the 2019 return has not been filed, eligibility for the payment will be based on taxpayer’s 2018 income tax return information. The discussion below highlights some of them. Enhanced Charitable Deductions in 2020.

There are a number of temporary income tax provisions in the CARES Act that will be of interest to our private clients. If the 2019 return has not been filed, eligibility for the payment will be based on taxpayer’s 2018 income tax return information. The discussion below highlights some of them. Enhanced Charitable Deductions in 2020.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content