This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mike McGlothlin , CFP, CLU, ChFC, LUTCF, NSSA, Executive Vice President, Retirement, at Ash Brokerage , is the 2024 recipient of the Kenneth Black Jr. McGlothlin served on the Society of FSP National Executive Committee from 2018 to 2021 and was National President in 2020-2021. Leadership Award.

At 50 though, you do need to have some context for how viable your idea of retirement is. My reasoning is as it has always been, my income is levered to the ups and downs of the stock market, I don't ever want to retire, we have been living below our means for ages and now all the more so having just paid off our mortgage.

In 1974, Congress passed the Employee Retirement Income Security Act (ERISA) that, among many other provisions, provided for the implementation of the Individual Retirement Arrangement. Amounts rolled over from employer retirementplans are entirely exempt. billion in the first year (1975). billion by 1981.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement. One option is to contribute to a Roth IRA.

In 2018, the brackets dropped to 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Mortgage interest will once again be tax-deductible on larger loans As a result of the 2017 legislation, between 2018 and 2025, interest on new mortgages is only tax-deductible up to $750,000 of mortgage debt on a primary or second home.

Let’s take a deep look at both plans, and particularly at where each stands out. It’s one of the best strategies to supercharge your retirement savings, especially for early retirement. There's no time like the present to begin preparing for your retirement. of providing tax-free income in retirement.

In its annual Retirement Confidence Survey of current workers and retirees, the Employee Benefit Research Institute found that workers’ confidence in their ability to fund retirement fell by the largest extent since the financial crisis of 2008, to levels not seen since 2018.

Picture retiring in 2010 versus 2020. As we say all the time, whereas stocks are the thing that goes up the most, most of the time in the modern era I would want more than 25% in equities for anyone needing normal stock market growth for their retirementplan to work. This is in the neighborhood of sequence of return.

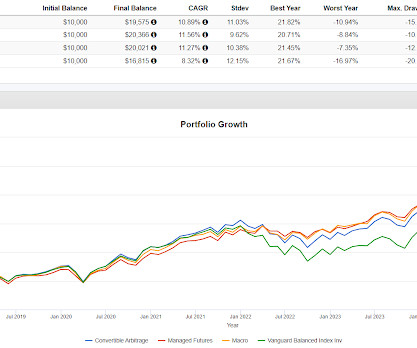

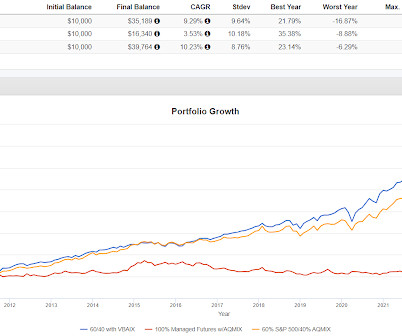

In 2018 you can see that two of them helped with just a few basis points. A year like 2018 constitutes down a little and is probably less important than protecting against down a lot like in 2022. In terms of crisis alpha in rough times, convertible arb didn't really help in 2022 but managed futures and macro did.

Do you even remember why stocks crashed in late 2018? There will be future events that result in some sort of drop, black swans to you or not, and these become more important as you get closer to retiring in terms of sequence of return risk. Any retirementplan runs the risk of coming up short for any number of reasons.

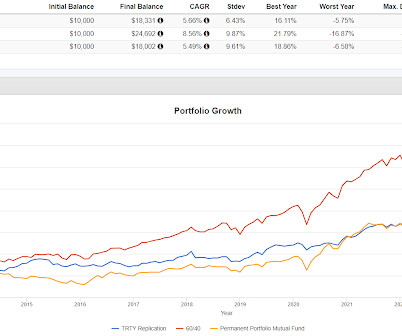

It's growth rate since inception is 3.58% going back to September, 2018 but a lot of that comes from a 15% lift in 2021 (numbers per testfol.io). RPAR is indexed and I think that fund's result shows that risk parity doesn't lend itself to an indexed approach. TRTY is a tough hold.

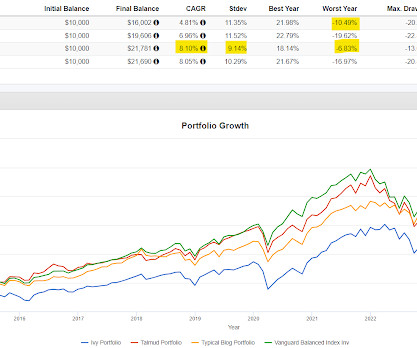

Someone retiring on Dec 31, 2021 being all in on traditional 60/40 had a real problem from an adverse sequence of returns. Someone retiring on Dec 31, 2021 with one of the managed futures-heavy portfolios had no such problem. It only back tests to 2018 but here's what you get. 90/40 was down 1.56% and Portfolio 3 was up 3.25%.

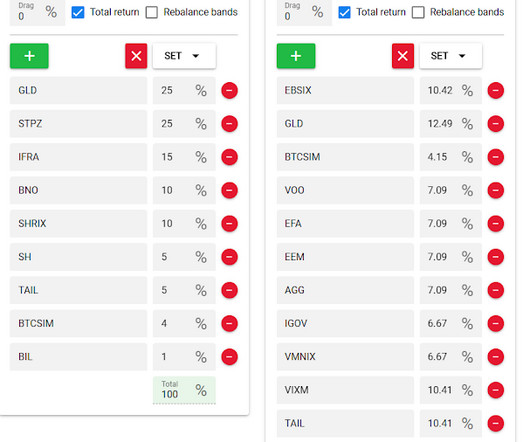

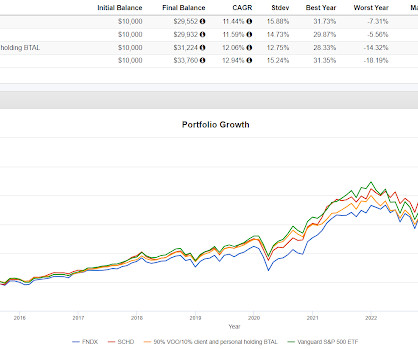

In late 2018 OCRP moved up when the market had a fast drop. OCRP will have 50% in CBOE Holdings (CBOE) and 50% in AGFiQ US Market Neutral Anti Beta ETF (BTAL) which are both client and personal holdings. If they can have single stock ETFs why not an ETF with just two holdings? I threw tail in as well as the S&P 500.

The 1987 crash was partly attributed to selling portfolio insurance and there was the so called Volmageddon of 2018. 2018 was not 1987 and if there is another event where volatility ends up being a major determent then it will be different than the other two but with some overlap. Events don't repeat but the can rhyme.

Over the past 10 years through the third quarter of 2018, the average high-fee option delivered an average annual return of 10.61% after expenses, while the low-fee option averaged 12.26%—a difference of 1.65 They say: "Consider the performance difference between high-fee and low-fee active funds focused on large-cap U.S.

Portfolio 3's worst year was 2018 when it fell 7.76%. Portfolio 2 had two years where it was down 5% (those were the worst two) and the leveraged version's worst year was 2018 when it fell 12.26%. The alts in the leverage sleeve all have a low to negative correlation to equities and to each other. BTAL is a client and personal holding.

It's only down year was 2018 with a decline of 7.91%. These portfolios don't really look anything like what we usually play around with here but the results are interesting. Despite all the leverage, Portfolio 1 has a very smooth ride including up a lot in 2022. I'm not a fan of leverage but that doesn't mean it can't be used effectively.

I think that is attributable to a terrible year for 100/100 in 2018. Terrible year in 2018 or 2022? 2018 was still lousy and 2022 was very good. I am more open to RSST as a core position than I was but 2018 is a good example of how it can go poorly. Notice though that the standard deviation for 100/100 is much higher.

I added SH for clients a little while and have been holding BTAL for them and personally since 2018. Relative to a day or two, the timing was very lucky. BTAL and SH are clearly first responder defensives. Gold can be a first responder, it often is but it's not quite as reliable as BTAL and SH.

Starting in 2018 causes the performance to change as follows. Both Portfolio 1 (Cockroach) and Portfolio 2 (the 3 fund mix I made up the other day) each have ways in which they are superior over the period studied from 2018 on. In 2017, as assembled, The Cockroach Portfolio went up 62% versus 21% for 100% SPY and 13% for VBAIX.

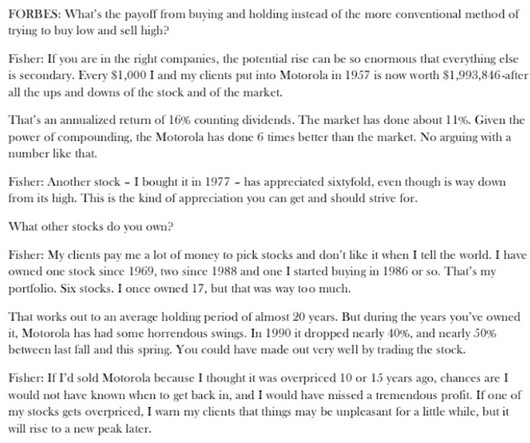

In 2018, Nvidia was down 30% versus 4% for the S&P 500 and in 2022 it was cut in half versus 18% for the S&P 500. In 2018, the 50/50 blend was up 12% versus a 4% drop for the S&P 500. Holding a stock for than long will be challenging. The Nvidia example ties right in with the Fisher quote.

The momentum funds also did not provide early warning for the downturn in late 2018. When the stock market started falling in September 2018, QMOM provided no early warning like I said, but it fell much more into the December 24th, 2018 bottom, 31% vs 19% for the S&P 500 and 20% for MTUM. Here's the last year.

The MAGI is used to determine the amount, if any, of your Traditional IRA contribution that is deductible if you or your spouse is covered by an employer retirementplan. Subtract any income from the AGI that is the result of IRA funds to a Roth IRA, or from a rollover conversion from a qualified employer retirementplan to a Roth IRA.

Portfoliovisualizer shows the annual decline at 1.55% but taking out 2018 when it was up 15% and 2022 when it was up 20% and it would have been noticeably worse. The managed futures blends' worst years in this study were 2011 when they were down slightly versus up 4.31% for VBAIX and 2018 when they were down 5.5%-6%

He also hosts the Stay Wealthy Retirement Show , which has been ranked on Forbes Top 10 Retirement Podcasts. In 2018, a company even offered to pay him $10 million for his website. Steve Gresham is the CEO of The Execution Project , a consulting firm that helps financial companies rethink “retirement” and get better results.

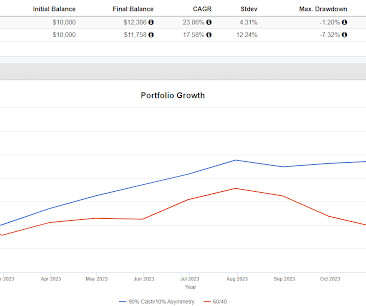

I started with a very small position in late 2018 with the intention of letting it grow into a lifechanging piece of money or letting it fail and I still own it. The tradeoff for the asymmetry is pretty wild volatility which came on with bad intentions in the last few days.

Forty years ago, the federal government lengthened Social Security’s full retirement age (FRA) from 65 to 67, and increased the delayed retirement credit. Since 1980 through 2014, workers with retirementplans that included a pension fell from 39% to 13%, a 200% decline. Is it the change we want?

Ditto the Christmas Crash in 2018. The general idea is that selling puts can lower portfolio volatility (I use a different fund, with a much different put strategy that does this) and help manage the downside but not during crashes. PUTW got pasted in the 2020 Pandemic Crash.

In 2018, the brackets dropped to 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Mortgage interest will once again be tax-deductible on larger loans As a result of the 2017 legislation, between 2018 and 2025, interest on new mortgages is only tax-deductible up to $750,000 of mortgage debt on a primary or second home.

In 2018 when VBAIX was down 2.82%, Portfolios 1 and 2 were down 3.36% and 3.17% respectively. One way to look at this is using inverse fixed income funds "worked" when markets were down a lot in 2022 but not when they were down a little in 2018. Again, there is something to this but it is not infallible.

It traded flat in the middle of the chart which isn't necessarily bad but that erosion of the price going into year-end 2018 was a 44% decline over those two years. In the Christmas 2018 crash, LAND fell about as much as the S&P 500 while FPI fared much worse. Both FPI and LAND offered protection in the Pandemic Crash of 2020.

TRTY only goes back to late 2018 so I build the following to try to replicate it with exposure I believe to be consistent with what TRTY owns. I don't know whether those weightings can vary but the numbers come off the home page for the fund.

In the backtest it was down 3.65% in 2015, that worst year was 2018 and in 2022 it was only down 2.72%. I am surprised how closely it tracks to VBAIX. It outperforms by a little, is a little less volatile but outperformed meaningfully in 2022.

It only goes back to 2018 because in 2017, Bitcoin went up an amount that may not be repeatable. Since CAOS hasn't had a real test of going up in a serious decline, if we replace it with more T-bills to get a longer backtest, the results are similar. Portfolios 1 and 3 both concentrate the risk into narrow slices of the portfolio.

In the partial year 2018, the very leveraged version lagged by a lot in a year that was very difficult for managed futures. There's a good chance of getting essentially the same effect with much less risk of being vulnerable to something breaking or at least bending a lot like managed futures in 2018. Closing out with a theory.

Trinity Replication though, offered more protection during the 2020 Pandemic Crash, In the very fast crash at the end of 2018, both portfolios above lagged 60/40. They have better upcapture than Trinity Replication but offered real diversification when it was most needed in 2022. One take away is that nothing can be best for all times.

In 2018 the S&P 500 was down a little over 4% and managed futures was down about 8%. To the notes above about the podcast, managed futures and several others we look at have differentiated return streams as opposed to being a different shade of the same color of large cap equities.

In the mini crash at the end of 2018, FNDX and SPHQ did worse than the S&P 500, SPYV was about the same as market cap weighting and SCHD was the best performer for that event. It did help some in the 2018 mini crash and helped a lot in the 2020 Pandemic Crash. The 90/10 blend outperformed SCHD and FNDX with less volatility.

I don't know but I can't refute it and chances are the value of your home was not effected by any of the flash crashes, the mini crash at the end of 2018 or any other stock market events that proved out to be insignificant including The Great Dip Of August, 2024. 2018 and 2020 were both fast events.

in 2018 when VBAIX dropped 2.8%, not very all weatherish. You're kind of waiting for the next calamity and even then, like 2018, there is no guarantee that this sort of all weather will work. Managed futures is great but it did badly in 2018, a down year for plain vanilla 60/40. If it did that once it can do it again.

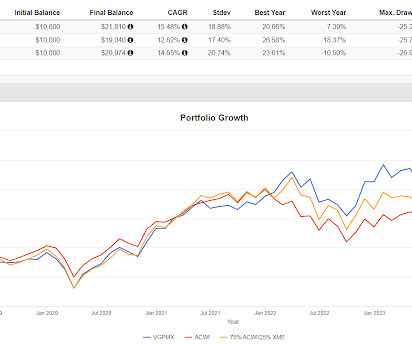

The fund goes back further than 2019 but the current manager started in 2018, so the period here gives us a clean slate to look at. I'm not really interested in the fund so much as an allocation implementation that is a holdover from when this fund used to be called the Vanguard Precious Metals and Mining Fund.

It briefly went to zero in 2018 and then came right back. If so then it becomes a way to harness volatility as an asset class and uncorrelated return stream which makes for good diversification when sized correctly. Per the above backtest, DSPX went up during market declines including a massive spike during the 2020 Pandemic Crash.

SRRIX lost -11.35% in 2017, -6.14% in 2018 and -4.47% in 2019." It is an unusual exposure, I am not aware of any other funds that are just reinsurance but if you know otherwise please comment. He notes " after three strong returns in its first three years (2014-16) came a string of losses.

I could have gone back further than 2018 but Bitcoin skyrocketed in 2017 so I wanted to take that out in case that sort of year never repeats again. Apparently LFMIX had a bad year in 2018, otherwise it's longer term result would be a little better.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content