This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S.,

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. One of the Roth IRA’s most compelling features?

In 1974, Congress passed the Employee Retirement Income Security Act (ERISA) that, among many other provisions, provided for the implementation of the Individual Retirement Arrangement. Non-deductible contributions were also allowed, for those individuals above the income limits, providing tax-deferred growth within the account.

When putting away for retirement, we often dream about all the things we’ll be able to do with that money – traveling, going out to eat, maybe trying new hobbies. . Of course, there are always the everyday household expenses to account for in your post-retirement budget. Ways to Start Planning Early for Retirement Health Care Costs.

At 50 though, you do need to have some context for how viable your idea of retirement is. My reasoning is as it has always been, my income is levered to the ups and downs of the stock market, I don't ever want to retire, we have been living below our means for ages and now all the more so having just paid off our mortgage.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement. The answer may be yes.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

In its annual Retirement Confidence Survey of current workers and retirees, the Employee Benefit Research Institute found that workers’ confidence in their ability to fund retirement fell by the largest extent since the financial crisis of 2008, to levels not seen since 2018.

It’s one of the best strategies to supercharge your retirement savings, especially for early retirement. That will give you a combined contribution of $13,000, which will also be fully tax-deductible. There's no time like the present to begin preparing for your retirement. Ads by Money.

529 Plans And The New Tax Code ajackson Tue, 07/17/2018 - 11:30 You Can Now Use 529s for K-12 Costs—But Should You? The cost of college is growing at an astronomical rate, and Section 529 plans have long helped individuals and families grow assets earmarked for education in a tax-efficient manner.

529 Plans And The New Tax Code. Tue, 07/17/2018 - 11:30. The cost of college is growing at an astronomical rate, and Section 529 plans have long helped individuals and families grow assets earmarked for education in a tax-efficient manner. The 2018tax overhaul expanded the reach of 529 plans beyond college.

In 2018 you can see that two of them helped with just a few basis points. A year like 2018 constitutes down a little and is probably less important than protecting against down a lot like in 2022. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

Property taxes For example, in certain locations such as sought-after vacation destinations, property taxes can be quite high. Property taxes For example, in certain locations such as sought-after vacation destinations, property taxes can be quite high. It’s all relative though.

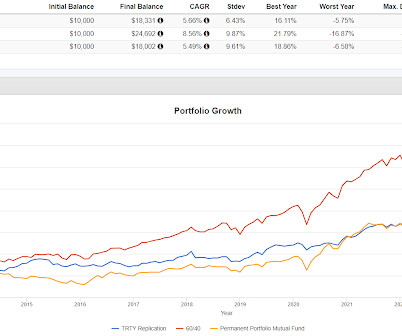

It's growth rate since inception is 3.58% going back to September, 2018 but a lot of that comes from a 15% lift in 2021 (numbers per testfol.io). They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. TRTY is a tough hold.

In late 2018 OCRP moved up when the market had a fast drop. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. If they can have single stock ETFs why not an ETF with just two holdings? I threw tail in as well as the S&P 500.

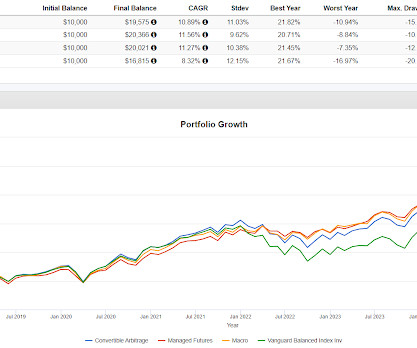

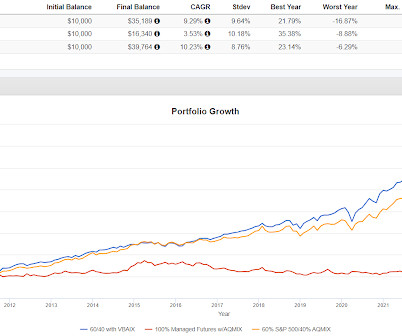

Someone retiring on Dec 31, 2021 being all in on traditional 60/40 had a real problem from an adverse sequence of returns. Someone retiring on Dec 31, 2021 with one of the managed futures-heavy portfolios had no such problem. It only back tests to 2018 but here's what you get. 90/40 was down 1.56% and Portfolio 3 was up 3.25%.

It's only down year was 2018 with a decline of 7.91%. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. These portfolios don't really look anything like what we usually play around with here but the results are interesting.

The 1987 crash was partly attributed to selling portfolio insurance and there was the so called Volmageddon of 2018. 2018 was not 1987 and if there is another event where volatility ends up being a major determent then it will be different than the other two but with some overlap. Events don't repeat but the can rhyme.

I added SH for clients a little while and have been holding BTAL for them and personally since 2018. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Relative to a day or two, the timing was very lucky.

I think that is attributable to a terrible year for 100/100 in 2018. Terrible year in 2018 or 2022? 2018 was still lousy and 2022 was very good. I am more open to RSST as a core position than I was but 2018 is a good example of how it can go poorly. Notice though that the standard deviation for 100/100 is much higher.

Forty years ago, the federal government lengthened Social Security’s full retirement age (FRA) from 65 to 67, and increased the delayed retirement credit. Since 1980 through 2014, workers with retirement plans that included a pension fell from 39% to 13%, a 200% decline. Is it the change we want?

Portfolio 3's worst year was 2018 when it fell 7.76%. Portfolio 2 had two years where it was down 5% (those were the worst two) and the leveraged version's worst year was 2018 when it fell 12.26%. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

Index funds have become popular among the FIRE (financial independence, retire early) crowd, and for a good reason. 2018: – 6.24%. From there, you’ll pay a 0.25% annual investing fee to access multiple portfolio options, advanced tax-savings tools, automatic portfolio rebalancing, and other perks. Invest in Farmland.

In 2018, Nvidia was down 30% versus 4% for the S&P 500 and in 2022 it was cut in half versus 18% for the S&P 500. In 2018, the 50/50 blend was up 12% versus a 4% drop for the S&P 500. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

Picture retiring in 2010 versus 2020. As we say all the time, whereas stocks are the thing that goes up the most, most of the time in the modern era I would want more than 25% in equities for anyone needing normal stock market growth for their retirement plan to work. This is in the neighborhood of sequence of return.

To implement these strategies successfully, we must first understand the difference between claiming the standard tax deduction and itemizing deductions. In this blog post, we will explore three charitable giving strategies intended for a tax deduction, minimizing record keeping, and increasing donations to charity.

Portfoliovisualizer shows the annual decline at 1.55% but taking out 2018 when it was up 15% and 2022 when it was up 20% and it would have been noticeably worse. The managed futures blends' worst years in this study were 2011 when they were down slightly versus up 4.31% for VBAIX and 2018 when they were down 5.5%-6%

I was “The Man Who Retired at 30”, and it was so unusual that it would show up in news headlines all over the place. My story was a nine-year working career, and retirement at 30. So at the end of year one, Curelop’s portfolio looked like this: 2018: Bought a second house for $343,000 ($27k down including some upgrades).

I started with a very small position in late 2018 with the intention of letting it grow into a lifechanging piece of money or letting it fail and I still own it. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

Accumulating wealth refers to growing investments, paying down debt, and saving for retirement. Financial freedom advances to long-term care and children’s education, as well as retirement savings and vacations. It is not meant to be, and should not be taken as financial, legal, tax or other professional advice.

There are a number of temporary income tax provisions in the CARES Act that will be of interest to our private clients. PROVISIONS AFFECTING INDIVIDUALS AND FAMILIES Recovery Rebate for Individual Taxpayers – Tax Credit. Relaxation of Penalties on Early Retirement Account Withdrawals for Virus Related Hardship.

There are a number of temporary income tax provisions in the CARES Act that will be of interest to our private clients. Recovery Rebate for Individual Taxpayers – Tax Credit. Eligibility for the one-time payment will be calculated using taxpayer’s income/filing status as reported on their 2019 income tax return.

In the backtest it was down 3.65% in 2015, that worst year was 2018 and in 2022 it was only down 2.72%. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. I am surprised how closely it tracks to VBAIX.

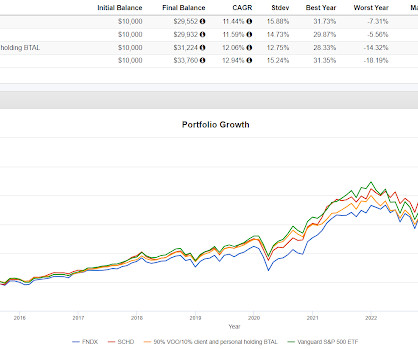

Depending on your tax situation though, more dividends may not be better. In the mini crash at the end of 2018, FNDX and SPHQ did worse than the S&P 500, SPYV was about the same as market cap weighting and SCHD was the best performer for that event. The reader was right for ten years. This table captures ten years.

It only goes back to 2018 because in 2017, Bitcoin went up an amount that may not be repeatable. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Portfolios 1 and 3 both concentrate the risk into narrow slices of the portfolio.

In 2018, there were approximately 52.4 This is a common way to target an individual’s retirement savings. Retirement savings are a limited pool of money, and keeping track of expenditure can ensure optimal utilization and establish sensible spending habits. The elderly population in the United States is on the rise.

The MAGI is used to determine the amount, if any, of your Traditional IRA contribution that is deductible if you or your spouse is covered by an employer retirement plan. Subtract any income from the AGI that is the result of IRA funds to a Roth IRA, or from a rollover conversion from a qualified employer retirement plan to a Roth IRA.

You willingly forgo income today with the faith that your company will survive many years into the future to make good on this liability to you—all for a tax benefit that tips the odds in your favor. The longer the tax deferral is in place, the more valuable this is. Behold the power of compounded tax-free gains!

In the partial year 2018, the very leveraged version lagged by a lot in a year that was very difficult for managed futures. There's a good chance of getting essentially the same effect with much less risk of being vulnerable to something breaking or at least bending a lot like managed futures in 2018. Closing out with a theory.

In 2018 the S&P 500 was down a little over 4% and managed futures was down about 8%. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

Siemens offers eligible employees a 409(a) Nonqualified Deferred Compensation Plan (DCP) which provides those employees with a fairly straightforward opportunity: willingly forgo income today for a tax benefit. Benefits of the Siemens DCP include tax benefits and the benefit of a company match. Tax Benefits.

TRTY only goes back to late 2018 so I build the following to try to replicate it with exposure I believe to be consistent with what TRTY owns. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content