This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

below the July 2019 tally. pts vs. July 2019. pts vs. July 2019), while Midweek occupancy reached 79.1% (up 4.5 pts vs. July 2019). ahead of last July and over 26% above July 2019 while RevPAR approached $134 for the month, +10.8% over July 2019 Click on graph for larger image. compared to July 2019.

hotel performance fell slightly from the previous week, but showed improved comparisons with 2019, according to STR‘s latest data through Aug. Dashed purple is 2019 (STR is comparing to a strong year for hotels). emphasis added The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

hotel performance increased from the previous week and showed improved comparisons with 2019, according to STR‘s latest data through Sept. Dashed purple is 2019 (STR is comparing to a strong year for hotels). From CoStar: STR: US Weekly Hotel Occupancy Reaches 70% U.S. Click on graph for larger image.

5-11, 2023 (percentage change from comparable week in 2019*): • Occupancy: 57.8% (-8.7%) • Average daily rate (ADR): $150.97 (+13.4%) • Revenue per available room (RevPAR): $87.21 (+3.6%) *Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019. Click on graph for larger image.

19-25, 2023 (percentage change from comparable week in 2019*): • Occupancy: 64.2% (-1.5%) • Average daily rate (ADR): US$156.51 (+22.2%) • Revenue per available room (RevPAR): US$100.43 (+20.3%) *Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019. Click on graph for larger image.

hotel performance rose from the previous week and showed mixed comparisons against 2019, according to STR‘s latest data through Jan. Dashed purple is 2019 (STR is comparing to a strong year for hotels). From CoStar: STR: Weekly US Hotel Occupancy Fails To Reach 55%, but Rates Stay High U.S. Click on graph for larger image.

YoY and nearly matching Mar 2019. Overall ADR exceeded $213, breaking the record from just a few months ago (Oct 2022, $208) and surpassing Mar 2022 and Mar 2019 by +30.7% over Mar 2019 Click on graph for larger image. compared to the same month in 2019. compared to March 2019, and up 56.0% in Mar 2023, up +9.6%

Today, in the Calculated Risk Real Estate Newsletter: 1st Look at Local Housing Markets in November with Comparison to 2019 A brief excerpt: NOTE: The tables for active listings, new listings and closed sales all include a comparison to November 2019 for each local market (some 2019 data is not available).

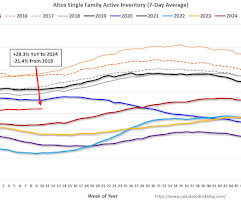

The black line is for 2019. compared to the same week in 2019 (last week it was down 23.3%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels has closed significantly! Click on graph for larger image. The red line is for 2024. Inventory was up 24.8%

Today, in the Calculated Risk Real Estate Newsletter: 1st Look at Local Housing Markets in January A brief excerpt: NOTE: The tables for active listings, new listings and closed sales all include a comparison to January 2019 for each local market (some 2019 data is not available). Im tracking over 40 local housing markets in the US.

million SAAR in December; Months-of-Supply above December 2019 Excerpt: Sales Year-over-Year and Not Seasonally Adjusted (NSA) The fourth graph shows existing home sales by month for 2022 and 2023. Today, in the CalculatedRisk Real Estate Newsletter: NAR: Existing-Home Sales Decreased to 3.78 Sales declined 6.2%

compared to the 2017 to 2019 same month levels. What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For February, Realtor.com reported inventory was up 27.5% YoY, but still down 22.9%

Today, in the Calculated Risk Real Estate Newsletter: 2nd Look at Local Housing Markets in October A brief excerpt: NOTE: The tables for active listings, new listings and closed sales all include a comparison to October 2019 for each local market (some 2019 data is not available). This is the second look at local markets in October.

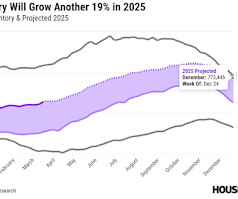

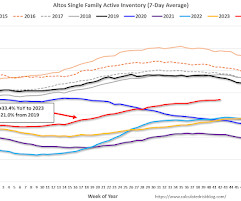

The black line is for 2019. compared to the same week in 2019 (last week it was down 17.4%). Inventory will pass 2020 levels soon, and it now appears inventory will be close to 2019 levels towards the end of 2025. The red line is for 2025. Inventory was up 33.4% This second inventory graph is courtesy of Altos Research.

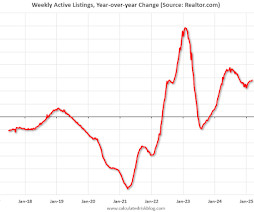

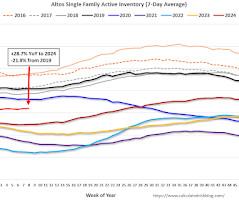

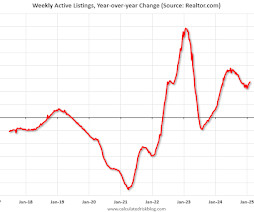

The black line is for 2019. compared to the same week in 2019 (last week it was down 22.1%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels has closed significantly! Click on graph for larger image. The red line is for 2025. Inventory was up 28.7%

The black line is for 2019. compared to the same week in 2019 (last week it was down 19.0%). Inventory will pass 2020 levels soon, and it now appears inventory will be close to 2019 levels towards the end of 2025. The red line is for 2025. Inventory was up 34.7% This second inventory graph is courtesy of Altos Research.

Altos Research put out an updated inventory projection last week showing that inventory might end the year at 2019 levels! If inventory is close to 2019 levels by the end of 2025, and sales remain sluggish, months-of-supply will move up sharply. And net legal immigration will slow sharply.

compared to the 2017 to 2019 same month levels. What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For January, Realtor.com reported inventory was up 24.6% YoY, but still down 24.8%

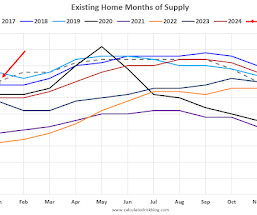

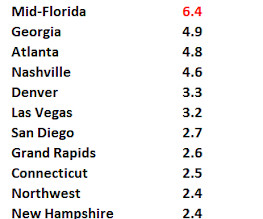

months in January 2019. Note that months-of-supply is higher than 6 of the last 8 years, and at the same level as in 2017. Months-of-supply was at 3.5 months in January 2025, up from 3.0 months in January 2024, and down from 3.8 Note that December and January usually have the lowest months-of-supply.

The first graph shows visitor traffic for 2019 (Black), 2020 (dark blue), 2021 (light blue), 2022 (light orange), 2023 (orange), 2024 (dark orange) and 2025 (red). compared to February 2019. compared to January 2019. compared to January 2019. ADR for the month reached $186 (25% YoY) with RevPAR of $150 (28% YoY).

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red). The dashed line is the percent of 2019 for the seven-day average. from the same day in 2019 (90.9% Dashed purple is 2019 (STR is comparing to a strong year for hotels).

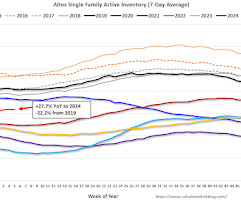

The black line is for 2019. compared to the same week in 2019 (last week it was down 23.0%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels has closed significantly! Click on graph for larger image. The red line is for 2024. Inventory was up 27.7%

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red). The dashed line is the percent of 2019 for the seven-day average. from the same day in 2019 (88.9% Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red). The dashed line is the percent of 2019 for the seven-day average. from the same day in 2019 (90.9% Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red). The dashed line is the percent of 2019 for the seven-day average. from the same day in 2019 (89.0% Dashed purple is 2019 (STR is comparing to a strong year for hotels).

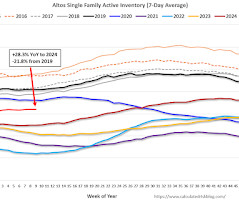

The black line is for 2019. compared to the same week in 2019 (last week it was down 21.9%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels has closed significantly! Click on graph for larger image. The red line is for 2025. Inventory was up 28.3%

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red). The dashed line is the percent of 2019 for the seven-day average. from the same day in 2019 (90.9% Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red). The dashed line is the percent of 2019 for the seven-day average. below the same week in 2019 (92.2% Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue), 2022 (Orange) and 2023 (Red). The dashed line is the percent of 2019 for the seven-day average. The 7-day average is at the same level as the same week in 2019 (100.5% Blue is for 2020.

However, compared to 3 years ago (2019), inventory is down 35.2% Inventory up compared to 2019 (currently down 35.2%). Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Altos reports inventory is down 0.5% week-over-week and down 1.5% from the peak on October 28th.

The black line is for 2019. compared to the same week in 2019 (last week it was down 27.5%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels is slowly closing. The second graph shows the seasonal pattern for active single-family inventory since 2015.

However, compared to 3 years ago (2019), inventory is down 34.8% Inventory up compared to 2019 (currently down 34.1%). Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Active inventory decreased last week. Altos reports inventory is down 2.6% from 468 thousand.

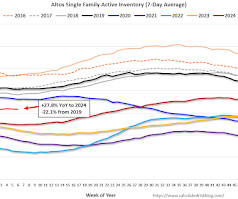

The black line is for 2019. compared to the same week in 2019 (last week it was down 21.4%). The first graph shows the seasonal pattern for active single-family inventory since 2015. Click on graph for larger image. The red line is for 2025. Inventory was up 29.3% The gap to more normal inventory levels has closed significantly!

The black line is for 2019. compared to the same week in 2019 (last week it was down 21.8%). The first graph shows the seasonal pattern for active single-family inventory since 2015. Click on graph for larger image. The red line is for 2025. Inventory was up 28.3% The gap to more normal inventory levels has closed significantly!

However, compared to 3 years ago (2019), inventory is down 34.4% Inventory up compared to 2019 (currently down 34.4%). Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Altos reports inventory is down 0.8% week-over-week and down 2.3% from the peak on October 28th.

The black line is for 2019. compared to the same week in 2019 (last week it was down 35.7%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels is slowly closing. The second graph shows the seasonal pattern for active single-family inventory since 2015.

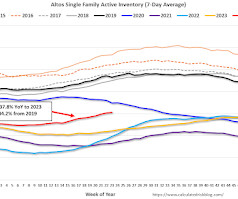

The black line is for 2019. compared to the same week in 2019 (last week it was down 37.2%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels is slowly closing. The red line is for 2024. Inventory was up 31.8% Mike Simonsen discusses this data regularly on Youtube.

The black line is for 2019. compared to the same week in 2019 (last week it was down 36.8%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels is slowly closing. The second graph shows the seasonal pattern for active single-family inventory since 2015.

Inventory up compared to 2019 (currently down 39.5%). Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019. Altos reports inventory is up 33.7%

Today, in the Calculated Risk Real Estate Newsletter: 2nd Look at Local Housing Markets in February A brief excerpt: NOTE: The tables for active listings, new listings and closed sales all include a comparison to February 2019 for each local market (some 2019 data is not available). Im tracking over 40 local housing markets in the US.

Inventory up compared to 2019 (currently down 44.6%). Here is a graph of the inventory change vs 2021, 2020 (milestone 3 above) and 2019 (milestone 4). The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019. More than double! Altos reports inventory is up 32.3%

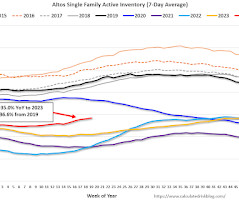

The black line is for 2019. compared to the same week in 2019 (last week it was down 22.6%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels is closing. Click on graph for larger image. The red line is for 2024. Inventory was up 33.4%

However, compared to 3 years ago (2019), inventory is down 35.0% Inventory up compared to 2019 (currently down 35.0%). Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Active inventory decreased last week. Altos reports inventory is down 2.5% from 454 thousand.

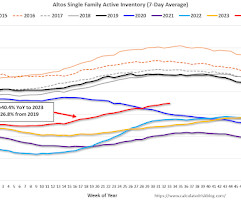

The black line is for 2019. compared to the same week in 2019 (last week it was down 22.2%). Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels has closed significantly! Click on graph for larger image. The red line is for 2024. Inventory was up 27.8%

147

147

Input your email to sign up, or if you already have an account, log in here!

Enter your email address to reset your password. A temporary password will be e‑mailed to you.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content