This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

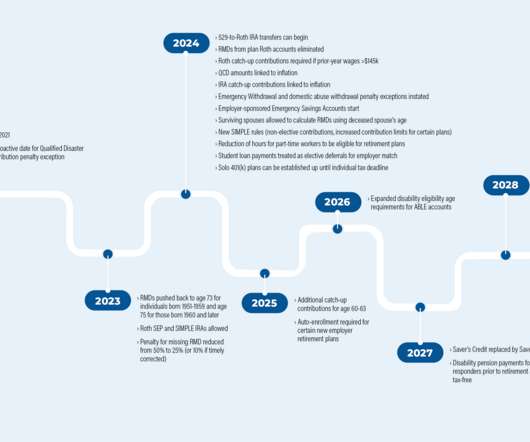

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 backdoor Roth conversions).

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0 backdoor Roth conversions).

Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. This is up from $285,000 in 2019, from $275,000 in 2017 and from $220,000 in 2014. High deductible health insurance plans . The estimate was $190,000 in their 2005 survey.

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirement planning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the shift in financial advice from pure investment management to comprehensive financial planning continues, with more individuals becoming CFP professionals than CFAs in the past few years as consumers increasing the diversity (..)

equity valuations: “Baby-boomers’ huge flow of 401K plan contributions helped to drive equities higher; now that ~70 million Boomers are retiring, when do demographics flip this from a huge positive to a net drag?” This demographic cohort is simply not a seller due to retirement – the tax expenses would be too great.

Consider these columns going back to 2013 pointing out the foolishness of tax-payer subsidized corporate welfare queens (2013), and why median wages were rising ( 2016 , 2017 , 2018 , 2018 , 2019 ). The 2010s monetary rescue plan benefitted anybody who owned capital assets: Stocks, Bonds, and Real Estate.

They continued to drift lower, until 2019, when Schwab became the first major firm to offer free trading. And even still, fund fees and taxes remained a major cost element. In 1978, Congress enacted Internal Revenue Code Section 401(k), which allowed tax-deferred savings through a company-administered plan.

The transcript from this week’s, MiB: Peter Mallouk, Creative Planning CEO , is below. He has since built Creative Planning into one of the nation’s largest RIAs and an absolute powerhouse running over $300 billion. What was the plan for your career with that combo? What can I say about Peter Mallouk? I’m having fun.

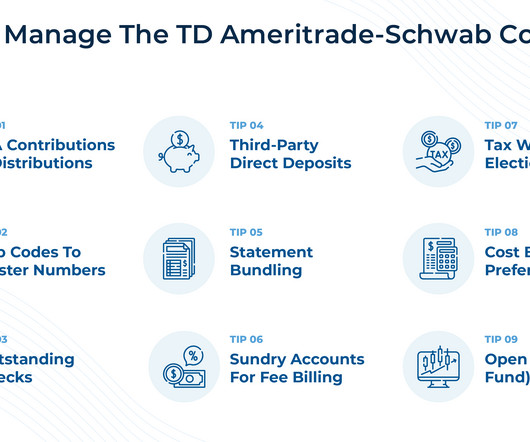

The announcement of the merger between Charles Schwab and TD Ameritrade in November 2019 kicked off a marathon of preparation for advisory firms to transition their clients on the TD Ameritrade custodial platform to Schwab.

A major decision in retirement planning is whether to make pre-tax or Roth (after-tax) 401k contributions. Pre-tax contributions go into your retirement account with money that has not been taxed, and then taxes will be paid when the funds are withdrawn in retirement.

Financial bloggers often portray the traditional IRA vs. the 401(k) plan as a debate, as if one plan is better than the other. In truth, they’re very different plans, and they fill very different needs. If you can, you should plan to have both. This is especially true if your 401(k) plan is fairly restrictive.

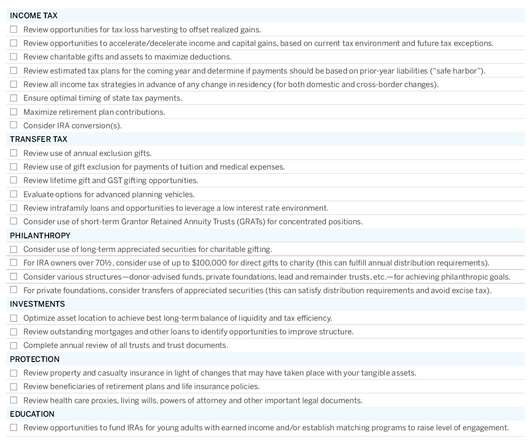

2019 Year-End Planning Letter. Fri, 11/01/2019 - 13:44. Each year, we send a letter to clients to help guide year-end planning discussions and to offer ideas for them to consider with their other advisors. Market conditions may be volatile, but our planning efforts are, as always, focused on stability and consistency.

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts.

In this fundamental Analysis of Exide Industries, we read about its history, operating segments, industry, financials and future plans. 2019 14720.88 It has been serving India for as long as we received our Independence. Fundamental Analysis of Exide Industries We will read in brief about its history and its current capabilities.

A highlight of the future plans of both the companies and a summary conclude the article at the end. However, the figures of Gujarat Fluorochemicals are not comparable historically because of exception tax treatment in base year FY19. Next, we’ll learn about the two businesses. Next, we’ll race through the financials of both stocks.

The article concludes with a highlight of future plans and a summary. The table below shows the total income and net profit of Gujarat Pipavav Port for 5 financial years: Year Total income (₹ In crores) Profit after tax (₹ In crores) 2023 967.95 Following that, we’ll go into the stock’s financials. million MT.

The article concludes with a highlight of future plans and a summary. The table below shows the Total income and net profit of Siyaram Silk Mills for 5 financial years: Year Total income (In crores) Profit after tax (In crores) 2023 ₹2272 ₹250 2022 ₹1939 ₹216 2021 ₹1130 ₹3.5 million handloom workers across the country.

The article concludes with a highlight of future plans and a summary. Year Total Revenue (Rs in Crores) Profit after tax (Rs in Crores) 2019 514.02 This also suggests that the company has the capacity to borrow additional capital for expansion and growth Year Debt to Equity (x) Interest Coverage Ratios (X) 2019 0.26

A highlight of the future plans & recent developments and a summary conclude the article at the end. The capital expense for modernization and new infrastructure has grown by 57% since 2019 to Rs 1.62 Higher income translated into higher profit after tax for the company. 2019 3,214 16.6 (Net lakh crore in 2023-24.

A highlight of the future plans of the company and a summary conclude the article at the end. The table below showcases the improvement in EBITDA margin and profit after tax (PAT) margin for the past few years. Future Plans of Tata Chemicals So far we looked at the previous fiscals’ data for our fundamental analysis of Tata Chemicals.

What are its future plans? A highlight of the future plans and a summary conclude the article at the end. On a positive note, it’s trailing twelve months (TTM) after the quarter ending December 2022 income and profit exhibited growth with Rs 356 crore profit after tax on income of Rs 2,999 crore.

Lastly, a highlight of their future plans and a summary conclude the article. DNL’s profit after tax was low on account of weak demand and margin compression. Particulars 2023 2022 2021 2020 2019 DNL - EBITDA Margin 16.8 Particulars 2023 2022 2021 2020 2019 DNL - Debt/Equity 0.0 Next, we’ll go through their financials.

A highlight of the future plans and a summary conclude the article at the end. During the same period, the profit after tax grew at a much sharper rate of 27.64% to Rs 256 crore. Future Plans Of Laxmi Organic Industries So far we looked at previous years’ data for our fundamental analysis of Laxmi Organic Industries.

And while the holidays are traditionally a time to reflect on our blessings and help those less fortunate than ourselves, there’s another factor influencing the timing of these donations — and that’s the goal of minimizing a tax bill. Three Tax-Advantaged Donation Strategies to Consider. Create a donor-advised fund (DAF).

Below are some insights from Richard Morris, Executive Vice President and Director of Tax Services, and Alex Seleznev, Senior Investment Advisor and Chief Operating Officer of MBI, LLC. And depending on your specific tax situation, you may be paying between 15% and 20% or even more in capital gain taxes.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. After the passing of the original Secure Act in 2019 , lawmakers have been working on enacting more changes. would, for the second time since 2019, increase the RMD age. 529 plan to Roth IRA rollovers.

The Roth IRA vs traditional IRA – they’re basically the same plan, right? While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirement plans. Not exactly. The most basic requirement is that you have earned income.

The importance of getting women into financial planning feels like it should go without saying. Alicia’s Experience One of my earliest experiences when I first decided to get into financial planning was participating in the Financial Planning Association’s Externship Program in the summer of 2020.

Among these are your longevity, lifestyle, comfort with market performance, sequence of return risk, current health, housing plan, proportion of fixed to variable expenses, proximity to children and so much more. Focus on Your Retirement Plan Rather Than a Magic Number. would be “How do I plan for retirement?“

If someone bought the Mystery Fund in late 2019, they wouldn't have been chasing heat even but a year later there probably would have been a ton of regret. The point is to understand that a portfolio that is valid for a long term investment plan will have periods where it lags in a frustrating manner.

just upended retirement planning…again. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. Here are some taxplanning strategies to consider when you should start drawing from your IRA. The Secure Act 2.0 But just because you can doesn’t mean you should.

The passing of the 2019 Secure Act changed the rules about when non-spouse beneficiaries must begin taking money from inherited retirement accounts. The central change the IRS is proposing would impact beneficiaries who inherited an IRA from a non-spouse who were subject to RMDs on the date of death and passed away after 12/31/2019.

Whether your client has young children of their own, teenage grandkids heading to college, or wants to help finance college for someone else in the family, it’s wise to encourage your clients to create a financial plan for doing so. Savings Plans: 529, Coverdell, UGMA. Tax considerations. Overall financial planning.

Stepchildren, remarriages, and ex-spouses: For the modern wealth management client with a blended family, planning to transfer wealth presents a web of complexity. Fortunately, financial professionals have tools and wealth transfer strategies that can help couples be intentional about the use of their assets in an estate plan.

Act has passed, making it the largest retirement legislation since the original Secure Act hit in the late 2019. As 55% of Americans say they don’t have enough saved for retirement, this bipartisan legislation primarily seeks to make it easier to contribute to retirement plans and use those funds appropriately for their needs in retirement.

This original IRA was not deductible from income for tax purposes, and the annual contribution limit was the lesser of $1,500 or 15% of household income. The Economic Recovery Tax Act (ERTA) of 1981 allowed for the IRA to become universally available as a savings incentive to all workers under age 70 1/2. billion by 1981.

The American Rescue plan signed in March, 2021 requires the IRS to pay out ½ of enhanced Child Tax Credits (CTC) to eligible taxpayers beginning this month. One to help ensure you will get your Child Tax Credit if you are a non-filer and a second one to opt out of the monthly payments. What everyone should know. IRS web-sites.

– Andres Disclosure: This page is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accounting, tax, legal or financial advisors. Let us connect you with the best financial advisor for you to understand the implications of the markets in your personal financial plan.

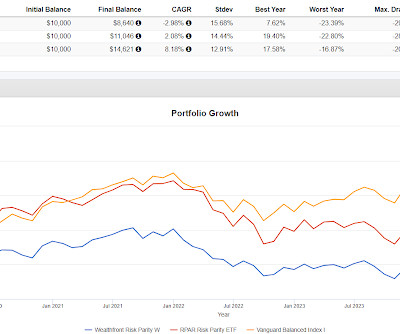

WFRPX did well in 2019 but lagged VBAIX by a lot in every other year of its existence. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Before then, RPAR tracked VBAIX pretty closely.

The change won’t impact anyone who inherited a retirement account during 2019 or years prior. That said, for tax purposes, taking a large lump sum in year 10 should generally be avoided. More planning strategies and tax implications below. If there’s a mix of pre-tax and Roth funds, RMDs will apply.

The contributions made to the account may be tax-deductible or non-deductible, depending on the individual’s income level and participation in an employer-sponsored retirement plan. Tax-deductible contributions reduce the individual’s taxable income, while non-deductible contributions do not.

Matt Kory, Vice President, Retirement Programs As a retirement income vehicle, the 401(k) is second in popularity only to Social Security – and as CNBC reported in 2019 the number of 401(k) millionaires is at an all-time high. A million dollars breaks down into an annual amount of about $30,000 over 30 years (not counting taxes, etc.).

The article concludes with a highlight of future plans and a summary. Year Revenue (in Crores) Profit after tax (in Crores) 2019 ₹ 88.5 ₹ 3 2020 ₹ 87.44 ₹ 0.81 Year ROE (%) RoCE (%) 2019 8.70% 12.95% 2020 2.23% 7.31% 2021 2.4% Year Debt to Equity (x) Interest Coverage Ratios (X) 2019 0.43 Crores in FY23.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content