This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72.

Also in industry news this week: A survey indicates that while financial advisors remain the most trusted source of financial advice, they might increasingly encounter client questions and ideas that originated from social media Following the transition of advisors and clients from TD Ameritrade and amid competition from competing RIA custodians, Charles (..)

In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirement planning. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges.

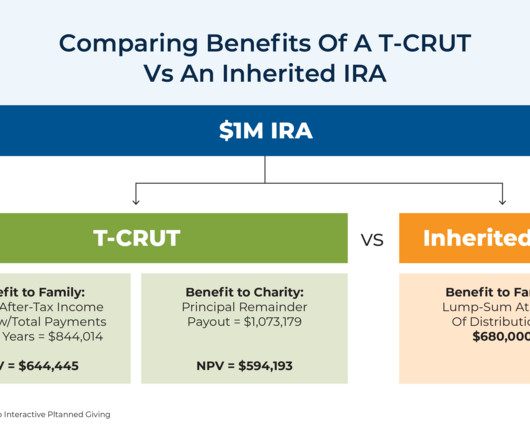

Below are some insights from Richard Morris, Executive Vice President and Director of Tax Services, and Alex Seleznev, Senior Investment Advisor and Chief Operating Officer of MBI, LLC. And depending on your specific tax situation, you may be paying between 15% and 20% or even more in capital gain taxes.

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts.

And while the holidays are traditionally a time to reflect on our blessings and help those less fortunate than ourselves, there’s another factor influencing the timing of these donations — and that’s the goal of minimizing a tax bill. Three Tax-Advantaged Donation Strategies to Consider. Create a donor-advised fund (DAF).

Here are some taxplanning strategies to consider when you should start drawing from your IRA. Taxplanning strategies for required minimum distributions Taxplanning shouldn’t stop when you retire. Retirees in a low tax bracket for the year have several planning options to consider.

The change won’t impact anyone who inherited a retirement account during 2019 or years prior. That said, for tax purposes, taking a large lump sum in year 10 should generally be avoided. More planning strategies and tax implications below. If there’s a mix of pre-tax and Roth funds, RMDs will apply.

The passing of the 2019 Secure Act changed the rules about when non-spouse beneficiaries must begin taking money from inherited retirement accounts. The central change the IRS is proposing would impact beneficiaries who inherited an IRA from a non-spouse who were subject to RMDs on the date of death and passed away after 12/31/2019.

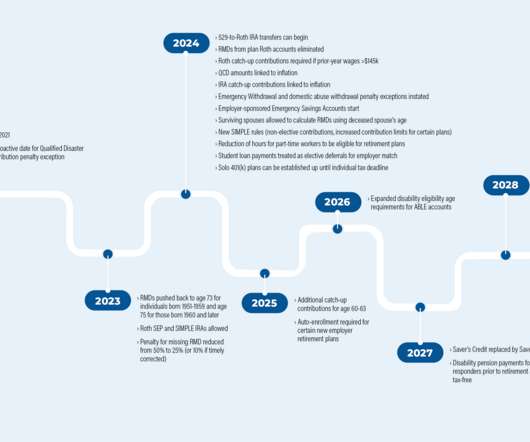

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. After the passing of the original Secure Act in 2019 , lawmakers have been working on enacting more changes. would, for the second time since 2019, increase the RMD age. 529 plan to Roth IRA rollovers.

Stay tuned for next week. – Andres Disclosure: This page is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accounting, tax, legal or financial advisors. The observations of industry trends should not be read as recommendations for stocks or sectors.

was signed into law December 29th, 2022, bringing more major changes to tax law. 529 plan to Roth IRA rollovers. The individual must be the designated beneficiary of the 529 plan and move funds to a Roth IRA in their name. Amount rolled over is tax-free (not included in beneficiary’s income) and penalty-free.

Stay tuned for next week. – Andres Disclosure: This page is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accounting, tax, legal or financial advisors. The observations of industry trends should not be read as recommendations for stocks or sectors.

The SECURE Act was passed in late 2019 and became law as of Jan. Among other things, the SECURE Act imposed a 10-year payout rule for an individual beneficiary who is not an Eligible Designated Beneficiary (EDB) and who inherits after 2019. An important taxplanning rule is to try to pay taxes at the lowest possible rate.

The Roth IRA can be a reliable and tax-efficient way to save for your future. A Roth IRA can provide you with tax-free growth, flexible contributions, and many investment options. Retirement planning accounts like the Roth and Traditional IRAs are among two of the most commonly used instruments for retirement savings.

The intent of stock option compensation is to align the interests of the employees with that of the company: The employee’s compensation increases as the stock price increases. Stock options can be either qualified or non-qualified, and the primary difference is how they are taxed.

While it may seem like a luxury that is only available to the wealthy, anyone is capable of building an effective financial plan and putting it into action. Without effective personal financial management, you risk losing money to poor budgeting, poor taxplanning, or even just to inflation.

The Long Game: Roth Conversions & Legacy Planning ajackson Thu, 08/01/2019 - 14:51 Legacy planning is all about transferring wealth to descendants as efficiently as possible. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

The Long Game: Roth Conversions & Legacy Planning. Thu, 08/01/2019 - 14:51. Legacy planning is all about transferring wealth to descendants as efficiently as possible. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

It’s important to note, severance payouts are taxed, and taxed as ordinary income in the year of payout. So, if you separate from the company near the end of the year, earning both a full year of salary plus severance payouts, you could be pushed into a higher tax bracket. Taxplanning for a transition out of Intel is critical.

Source: Levels.fyi Planning opportunities with salary: Contribute to your 401(k), HSA, and (for those Level 67+) Deferred Compensation accounts to reduce your taxes today. Restricted Stock Units vest over time and are taxed as income at vesting. Incorporate taxplanning with your RSU vesting schedule to minimize taxes.

Planning opportunities with salary: Contribute to your 401(k), HSA, and (for those Level 67+) Deferred Compensation accounts to reduce your taxes today. Restricted Stock Units vest over time and are taxed as income. Planning opportunities with RSUs: Use RSU income to maximize contributions to other benefits programs.

409(a) Nonqualified Deferred Compensation Plans present one of these opportunities. You willingly forgo income today with the faith that your company will survive many years into the future to make good on this liability to you—all for a tax benefit that tips the odds in your favor. Behold the power of compounded tax-free gains!

Over the years, the CFP exam has undergone refinements in line with the evolution of the financial planning profession. The most recent revision occurred in 2019, resulting in the current computer-based test format. Take time to review the exam blueprint and syllabus to gain clarity on the topics and domains covered.

December 6, 2019 – I made the best decision I have ever made in my professional life to move my clients to the independent side of the wealth management industry. My ability to build relationships, focus on taxplanning and provide transparency for every step in the financial planning process. The Home Page.

Financial Planning: This involves creating a comprehensive financial plan, considering all aspects of your financial situation. This plan may cover estate and retirement planning, college savings, debt management, and more. Tax services provided through Harness Tax LLC.

In this blog, we’ll be utilizing data found by Fidelity Investments Millionaire Outlook Study from 2019. Unfortunately, in 2019, this index went into the negatives for the first time. More than 8% of US adults fit the bill by this definition. How Financially Stressed Are Millionaires? But wait, there’s more.

In fact, I’m one of the oldest of the millennial generation and I need help from my advisor with all of the following: Retirement planning. Taxplanning. College planning for my kids. Long-term care planning. Estate planning. As millennials get older, their financial complexity keeps growing. Life insurance.

So for a taxable investor, hedge funds generally aren’t tax efficient. And when you look at the assets that are invested, the three trillion in hedge funds, I would guess that north of 90% of that are in institutions that don’t pay taxes. It’s part of their own taxplanning. I like Buffett’s idea.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content