This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

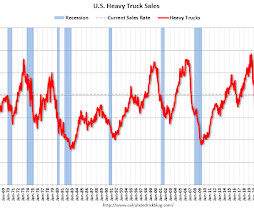

Heavy truck sales declined sharply at the beginning of the pandemic, falling to a low of 288 thousand SAAR in May 2020. Note: "Heavy trucks - trucks more than 14,000 pounds gross vehicle weight." Heavy truck sales were at 403 thousand SAAR in March, down from 436 thousand in February, and down 12.1% from 459 thousand SAAR in February 2025.

Inventory is now above the levels for the same week in 2020 (milestone 3 below). from 426 thousand, and compared to the same week in 2020 inventory is up 1.1% Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Two years ago (in 2020) inventory was declining all year.

Today, in the Calculated Risk Real Estate Newsletter: Single Family Built-for-Rent Almost Doubled Since 2020 A brief excerpt: Along with the monthly housing starts report for January released last week, the Census Bureau also released Housing Units Started by Purpose and Design through Q4 2023.

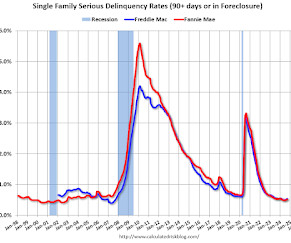

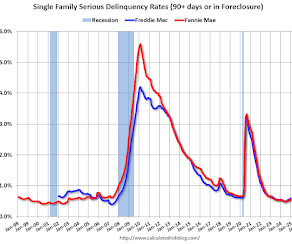

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic. The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

Preparing for the unexpected and pivoting at a moment’s notice were valuable lessons many global companies learned in 2020 and 2021. As we move through 2022, companies are eager to retain a competitive advantage and continue on the path of success and adaptability.

compared with last year, and it was the highest since July 2020 in the early days of the COVID-19 Pandemic. For the 29th straight week, there were more homes listed for sale versus the prior year, giving homebuyers more options. This past week, the inventory of homes for sale grew by 36.5% year-over-year increase in inventory in April. •

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic.Fannie Mae reported that the Single-Family serious delinquency rate in September was 0.52%, up from 0.50% in August. This is below the pre-pandemic lows. There is much more in the article.

In fact, last week saw the highest number of homes for sale since August 2020 , a significant milestone. For the 27th straight week, there were more homes listed for sale versus the prior year, giving homebuyers more options.

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic. The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

This is down from the record high in April 2020 of 22.9% level in February 2020 (pre-pandemic). These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 7.5% in the previous month. and up from the lowest level on record (seasonally adjusted) in December 2022 (6.6%).

It also covers many types of investments, including annuities, fixed-indexed annuities, CDs and other banking products, digital assets, commodities, and real estate, whereas previous rules like Reg BI and PTE 2020-02 applied only to securities like stocks, bonds, and funds.

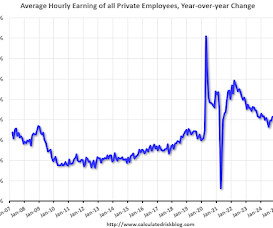

The second graph shows that goods prices started to increase year-over-year (YoY) in 2020 and accelerated in 2021 due to both strong demand and supply chain disruptions. Services were up 3.7% YoY as of March 2025, down from 4.1% YoY in February. Services less rent of shelter was up 3.3% YoY in March, down from 3.8% YoY in February.

The sharp increase in 2020 in the 90-day bucket was due to loans in forbearance (included as delinquent, but not reported to the credit bureaus). percent of all loans outstanding at the end of the third quarter of 2024 compared to one year ago, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey.

economy will likely perform in 2025, and if there are surprises - like in 2020 with the pandemic - to adjust my thinking. in February 2020. These are just questions; I'll follow up with some thoughts on each of these questions. The purpose of these questions is to provide a framework of how the U.S. by 2033 due to demographics.

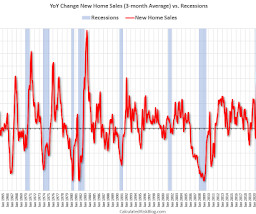

New home sales peaked in 2020 as pandemic buying soared. Another exception was in late 2021 - we saw a significant YoY decline in new home sales related to the pandemic and the surge in new home sales in the second half of 2020. Note that Residential Investment is quarterly and single-family starts and new home sales are monthly.

This is down from the record high in April 2020 of 22.9% level in February 2020 (pre-pandemic). These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 7.9% in the previous month. and up from the lowest level on record (seasonally adjusted) in December 2022 (6.6%).

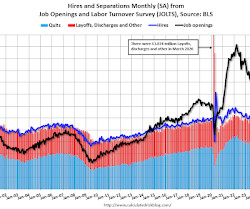

The spike in layoffs and discharges in March 2020 is labeled, but off the chart to better show the usual data. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs. Jobs openings decreased in December to 7.60 million from 8.12 million in November.

New home sales peaked in 2020 as pandemic buying soared. Another exception was in late 2021 - we saw a significant YoY decline in new home sales related to the pandemic and the surge in new home sales in the second half of 2020. Note that Residential Investment is quarterly and single-family starts and new home sales are monthly.

The spike in layoffs and discharges in March 2020 is labeled, but off the chart to better show the usual data. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs. Jobs openings decreased in February to 7.57 million from 7.76 million in January.

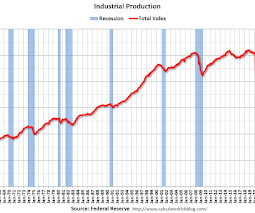

This series is up from the record low set in April 2020, and close to the level in February 2020 (pre-pandemic). Capacity utilization stepped up to 77.8 percent , a rate that is 1.8 percentage points below its long-run (19722024) average. emphasis added Click on graph for larger image. This graph shows Capacity Utilization.

The second graph shows that goods prices started to increase year-over-year (YoY) in 2020 and accelerated in 2021 due to both strong demand and supply chain disruptions. Services less rent of shelter was up 3.8% YoY in February, down from 3.9% YoY in January. Durables were at -1.2% YoY as of February 2025, unchanged from -1.2% YoY in January.

This is down from the record high in April 2020 of 22.9% level in February 2020 (pre-pandemic). These workers are included in the alternate measure of labor underutilization (U-6) that was unchanged at 7.5% in the previous month. and up from the lowest level on record (seasonally adjusted) in December 2022 (6.6%).

This series is up from the record low set in April 2020, and close to the level in February 2020 (pre-pandemic). Capacity utilization stepped down to 77.8 percent , a rate that is 1.8 percentage points below its long-run (19722024) average. emphasis added Click on graph for larger image. This graph shows Capacity Utilization.

Note: In 2020, prices increased late into the year and peaked in October, but prices peaked in June for all the other years. Change in Median House Price from January to June 2018 2019 2020 2021 2022 2023 January to June 13.7% The NAR reported the median price was $396,900 in January 2025, down 7.0% from $426,900 in June 2024.

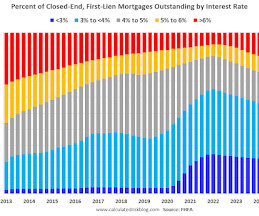

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Here is some data showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q4 2024.

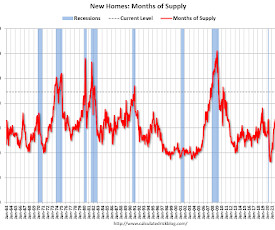

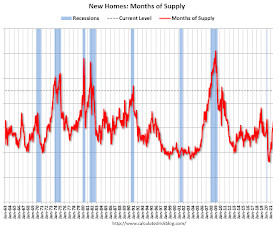

months in August 2020. The months of supply decreased in November to 8.9 months from 9.2 months in October. The all-time record high was 12.2 months of supply in January 2009. The all-time record low was 3.3 This is well above the top of the normal range (about 4 to 6 months of supply is normal).

from 428 thousand, and compared to the same week in 2020 inventory is down only 0.3% Here is a graph of the inventory change vs 2021, 2020 (milestone 3 above) and 2019 (milestone 4). Two years ago (in 2020) inventory was declining all year. Active inventory increased for the 3rd consecutive week, increasing 0.8% year-over-year.

from 433 thousand, however compared to the same week in 2020 inventory is down 1.9% Here is a graph of the inventory change vs 2021, 2020 (milestone 3 above) and 2019 (milestone 4). Two years ago (in 2020) inventory was declining all year, so the two-year comparison will get easier all year. More than double! year-over-year.

from 424 thousand, and compared to the same week in 2020 inventory is up 2.1% Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ? Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Active inventory increased again, hitting a new peak for the year.

from 385 thousand, and compared to the same week in 2020 inventory is up 10.6% Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ? Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Altos reports inventory is down 0.5% week-over-week and down 1.5%

months in August 2020. The months of supply increased in January to 9.0 months from 8.0 months in December. The all-time record high was 12.2 months of supply in January 2009. The all-time record low was 3.3 This is well above the top of the normal range (about 4 to 6 months of supply is normal).

from 339 thousand, and compared to the same week in 2020 inventory is up 14.3% Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅ 4. Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Active inventory decreased last week. from 468 thousand.

from 375 thousand, and compared to the same week in 2020 inventory is up 12.9% Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ? Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Altos reports inventory is down 0.8% week-over-week and down 2.3%

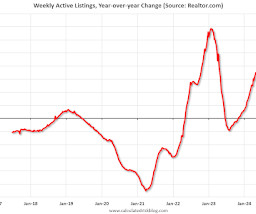

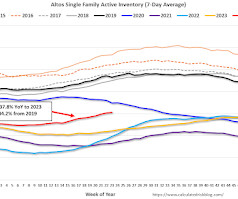

Inventory will pass 2020 levels soon, and it now appears inventory will be close to 2019 levels towards the end of 2025. Inventory was up 33.4% compared to the same week in 2024 (last week it was up 34.7%), and down 17.5% compared to the same week in 2019 (last week it was down 17.4%).

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red). Black is 2020, Blue is 2021 and Red is 2022. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Blue is for 2020.

from 326 thousand, and compared to the same week in 2020 inventory is up 15.0% Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅ 4. Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4). Active inventory decreased last week. from 454 thousand.

from the February bottom, and at the highest level since August 2020. Inventory should be above 2020 levels for the same week in the next couple of months. Altos reports that active single-family inventory was up 1.1% week-over-week. Inventory is now up 23.8% Click on graph for larger image. Inventory was up 37.8%

This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue), 2022 (Orange) and 2023 (Red). Black is 2020, Blue is 2021 and Red is 2022. The red line is for 2023, black is 2020, blue is the median, and dashed light blue is for 2022. Blue is for 2020.

The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic). This graph shows light vehicle sales since 2006 from the BEA (blue) and Wards Auto's estimate for October (red).

Inventory will pass 2020 levels soon, and it now appears inventory will be close to 2019 levels towards the end of 2025. Inventory was up 34.7% compared to the same week in 2024 (last week it was up 30.6%), and down 17.4% compared to the same week in 2019 (last week it was down 19.0%).

This is down from the record high in April 2020 of 22.9% level in February 2020 (pre-pandemic). These workers are included in the alternate measure of labor underutilization (U-6) that increased to 8.0% in the previous month. and up from the lowest level on record (seasonally adjusted) in December 2022 (6.6%).

The impact of COVID-19 was significant, and April 2020 was the worst month. After April 2020, sales increased, and were close to sales in 2019 (the year before the pandemic). Click on graph for larger image. This graph shows light vehicle sales since 2006 from the BEA (blue) and BEA's estimate for May (red).

2018 2019 2020 2021 2022 Peak Month June June Oct June June December -7.0% -3.8% -0.7% -2.2% -11.3% N/A In 2020, prices increased late into the year and only decline slightly seasonally (the start of the pandemic buying boom), and in 2021, median prices only declined about 3% from peak to bottom. January -8.9% -6.7% -1.2% -3.4%

This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic). Capacity utilization moved up 0.2 percentage point in September to 80.3 percent , a rate that is 0.7 percentage point above its long-run (1972–2021) average. emphasis added Click on graph for larger image.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content