This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A reader asks: My assetallocation has been pretty conservative since the market run-up in 2020. My basic thesis is that the market is overvalued, and the only way I can keep myself in equities at all is to have a 60/40 stock/bond allocation. I have nagging doubts that my alloc.

But in some ways, those events, and we saw it again in March of 2020, we saw it again around where you see these big moments where it draws people together. So what we find, and then of course we have a multi-asset solutions business where we talk to clients about the entirety of their portfolio, their strategic assetallocation models.

Indian households traditionally invested most savings in physical assets. However, financial assetallocation increased recently. Its revenue surged from ₹3,508 crore in March 2020 to ₹14,780 crore in March 2024. It increased from ₹1,885 crore in March 2020 to ₹8,306 crore in March 2024. in March 2020 to ₹167.79

The liquidity support since 2008 and massive stimulus post March 2020 has inflated all the asset prices be it equity, debt, or real estate. However, we can think of three possible scenarios ahead: Irrespective of what scenario will pan out, equity valuations inevitably have to adjust according to the principle of mean reversion.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: Well, he sort of — yeah, he thought about it.

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. from its August 2020 lows and has already seen the biggest move higher in yields since 1987, when rates moved higher by 3.2%.

Remember that global pandemic back in 2020 called COVID-19 that killed over 350,000 people in the U.S.? What did the stock market actually do in 2020? That same year, the unemployment rate reached a sky-high level of 14.9% (vs. most recently) and the economy went into recession with GDP (Gross Domestic Product) declining by -2.2%.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

In good times i.e. when the market valuations are usually very high, everyone agrees to the logic of buying low and selling high. Not understanding the role & importance of tactical assetallocation (overweight debt in euphoric times and overweight equity in a time of acute pessimism) in creating superior returns over the long term.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. At the same time, the resilience of the U.S.

One equity market debate discussed frequently in the LPL Research Strategic & Tactical AssetAllocation Committee (STAAC) is the growth vs. value style reversal experienced the past 12 months. Increasing the discount rate, which lowers the present value of future cash flows, and company valuations.

over the last 20 years, pre-2020. Retailer valuations have also taken a hit, as the forward (next 12 months) P/E multiple has contracted ~20% year to date, from ~27x to ~22x currently. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from Bloomberg.

Total employment has returned to pre-pandemic levels in February 2020 but not back to pre-pandemic trends [ Figure 1 ]. percentage points below February 2020, and the largest gaps were for those of high school and college age and those 55 years old and up [ Figure 2 ]. Overall, the July labor force participation rate was 1.3

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. 00:04:02 That’s what value add software was originally. Otherwise, why not just buy passive?

As I pointed out last month, we are coming off a heroic advance over the last three years (2019/2020/2021) with the S&P 500 soaring +90%. They certainly could, but valuations remain attractive given where interest rates currently stand. Source: Yardeni.com. Could the headwinds previously described cause prices to go lower?

So they’d give individual assetallocation to people and they’d go invest their money. The unrated piece yielded 2020 5% where the rated piece would yield three to 5%. What happened over the last year and a half or so is rates went up and valuations went down. This was gonna be a multi-strategy vehicle.

I did it during the coronavirus collapse in 2020, and I did it again in 2022. I think it’s very hard to say stocks are objectively cheap because all of these valuation metrics have, have become unreliable over the decades as the nature of the stock market has changed. I did it in 2000, 2002. I did it in 2008 in oh nine.

EOG is poised to breakout and trades at bargain valuation of about nine times earnings (relative to the S&P at 23 times earnings and a touch under the overall energy sector of 12 times earnings). That said, it loses early in round one simply due to us believing it’s close to full valuation and due for a breather.

So there’s been a big push for folks to get the appropriate level of assetallocation in a highly diversified, low cost way. DAVIS: Where international equities, because of valuations, probably 7% to 7.5%. RITHOLTZ: So let’s talk about that, because that gap in valuation has persisted for a long time.

T he stock market has been like a rocket ship over the last three years 2019/2020/2021, advancing +90% as measured by the S&P 500 index, and +136% for the NASDAQ. After this meteoric multi-year rise, stock values started to come back to earth in 2022, and the rocket ship turned into a roller coaster during January.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Dates: 1/31/1995 to 9/30/2020.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Dates: 1/31/1995 to 9/30/2020.

Managing Liquidity in the Coronavirus Market ajackson Mon, 03/30/2020 - 16:04 This article was written by Sid Ahl, Taylor Graff, Adam King and J.R. Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.”

Mon, 03/30/2020 - 16:04. Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” 3/16/2020. Source: BLOOMBERG as of 3/31/2020. Managing Liquidity in the Coronavirus Market. Harsh Reaction.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Valuations are elevated but nowhere near the bubble levels of the late 1990s. GDP than it was 100 years ago.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Valuations are elevated but nowhere near the bubble levels of the late 1990s. GDP than it was 100 years ago.

Dent got a big market decline in 2020, but because of Covid, not for any of the reasons he cited. 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.” 2020 : “[E]xtreme valuations. ” The S&P earned 15.89 2015 : “Exit now.”

He wasn’t tactical assetallocator. It’s about long-term planning and strategic assetallocation and, and just understanding how markets work and how behavior comes into the mix. It’s money that represents the cash needs or the, the, the liquidity side of, of assetallocation.

He launched his own firm right into the teeth of the collapse in ’09, which turned out to be quite a fortuitous time to launch an asset management shop. Everybody wants to sell a company when they get a good valuation. RITHOLTZ: — heading into 2020? So we do a lot of valuation work. BERNSTEIN: Correct.

It’s just a fascinating conversation about looking at the world from both bottoms up and top-down, as well as thinking about what valuations are like, how likely are macro events, the impact you’re getting not just the return on capital, but as famously said in fixed income, a return of your capital. RITHOLTZ: Really quite fascinating.

Yeah, Mike Freno : It’s, it, it was a, I stepped in in November of 2020, so it’s ’cause a lot of things were going on during that period of time. The parent company handles all the asset liability management side of things. They give us assetallocations, we go ahead and and and and invest those dollars.

What, what was your experience during the first quarter of 2020 during the pandemic s and p down 34%. And one of the worst performing factors has been valuation. And I think that’s wrong because valuation does matter. And now we’re just assuming that’s gonna repeat over and over again.

And are you saying the recession in 2020 is similar to recession in the 1950s? 00:21:21 [Speaker Changed] So this story came out that, oh, value is defensive because it has this valuation buffer to it 00:21:28 [Speaker Changed] In that one example. 12, 14 even that not a lot of numbers. It’s such a different world.

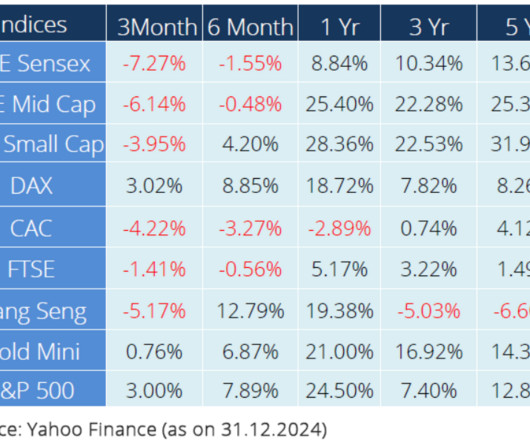

The FY25 earnings growth estimate has been reduced to ~5% now, the lowest since FY 2020. Overall, we maintain our underweight position to equity (check the assetallocation below) on the back of pricey markets- the current PE ratio of 22.7x Most of our portfolios include a small allocation to Chinese markets.

And so I worked a lot on the assetallocation side. Again, as I said, we’ve worked in assetallocation. And you know, it’s the same thing when valuation gets outta control too. It will come home to roost at some point, but doesn’t mean the valuation can’t get worse. They have yield.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content