This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If only the Fed didn’t do X, our portfolio would have been much better” seems to be a terrible approach to managing assets for clients. 2020s : Remained on emergency footing post Covid, despite broad evidence of economic recovery. Following those March 2020 rate cuts, the Fed stayed at Zero until March 2022.

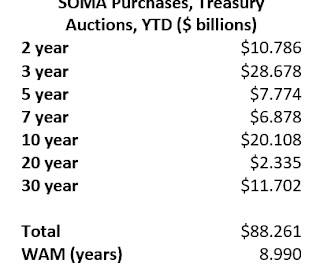

From housing economist Tom Lawler: From the beginning of 2020 to early June of 2022 the Federal Reserves balance sheet more than doubled to an almost inconceivable $8.9 Inquiring minds might want to know why the Federal Reserve did not achieve its balance sheet targets by selling longer maturity/duration assets it had previously purchased.

Let's dig in some more on Permanent Portfolio quadrant style. AQR Multi-Asset (AQRIX) used to be called Risk Parity and it also does some quadranty stuff. It had a big drawdown in the 2020 Pandemic Crash which, ok, something like that sure but it had a surprisingly big drawdown in 2022 as you can see at 13%.

What’s obvious is that cheaper is better than more expensive; that there are inherent costs in managing an active portfolio that include more than just trading and taxes but research, analysis, PMs, etc. But that is not the same as becoming one of the most dominant asset managers in the world. Concentrated portfolio risk.

Low Stakes : The most successful market timers are often those people who do not have actual assets at risk. Staying long through the 60-day 34% drop during the 2020 pandemic; getting out of the market ahead of the 2022 rate hiking cycle; and getting back in October 2022 for the next bull leg. It’s utterly laughable.

From the perspective of an asset management and financial planning firm, the challenge is getting people to ignore the day-to-day noise in favor of thinking about where prices will be a decade hence. Rather than accept the volatility of month-to-month economic datapoints — NFP, Consumer Spending, Manufacturing, Inflation, etc.

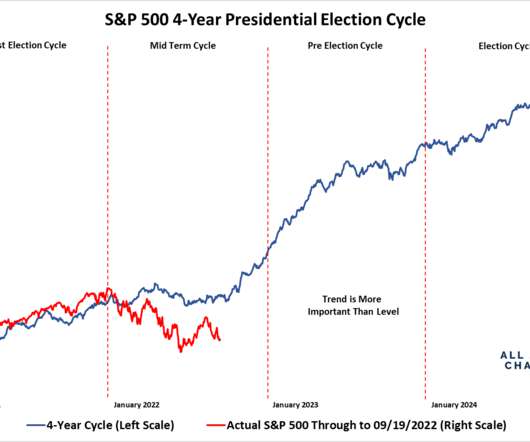

2020 : Pandemic crash of 34%, fastest top fall (but fastest recovery) 2022 : Stocks & bonds both down double digits since 1981 All of these meet the unofficial definition of a bear of a 20% move off of the peak. The GFC and the pandemic were global phenomena; the 2022 market was the worst since 1981 for a 60/40 portfolio.

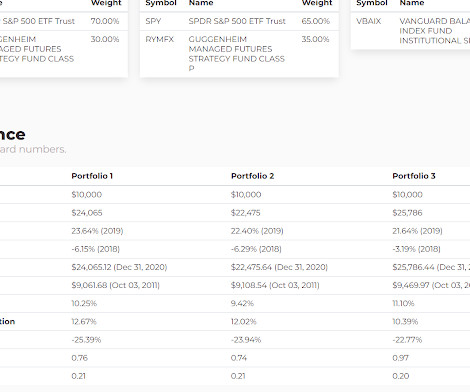

The asset mix is comprised of equities, REITs, gold, bonds and "diversified futures" which I take to mean managed futures. WAAV seems Permanent Portfolio inspired which is why I threw in AQRIX and PRPFX along with VBAIX as a proxy for a 60/40 portfolio makes sense as a benchmark. Or not, that's the reason to dig in a little.

The transcript from this week’s, MiB: Elizabeth Burton, Goldman Sachs Asset Management , is below. Elizabeth Burton is Goldman Sachs asset management’s client investment strategist. Her job is portfolio and product solutions and that means she could go anywhere in the world and do anything. Elizabeth Burton : Hi Barry.

Johnson joined the firm in 1988 and held leadership roles in all its major divisions before becoming CEO in February 2020. She also led the historic acquisition of Legg Mason in 2020, and Putnam in 2023, with the organization now managing more than $1.5 trillion globally.

During times of economic, financial, and political uncertainty, investors often wonder where to invest or what changes to make to their portfolio. On one hand, youre getting a lower rate on your mortgage, but on the other, you may own mortgage-backed securities as part of your bond portfolio. How do bonds perform during a recession?

Full transcript below. ~~~ About this week’s guest: Ari Rosenbaum serves as the Director of Private Wealth Solutions at O’Shaughnessy Asset Management , now part of investing giant Franklin Templeton. After-tax equity returns from your non-tax-exempt portfolios. So we, for practical purposes, remove those from the portfolio.

The basic summary is that they blended together a bunch of asset classes, of which only gold had negative correlation to US large cap, and that blend lagged in 2023. We work on theoretical portfolios here all the time that blend in strategies that really are negatively correlated or at least very little correlation. On to today's post.

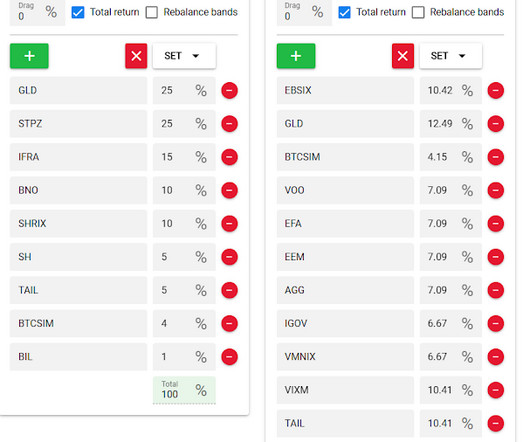

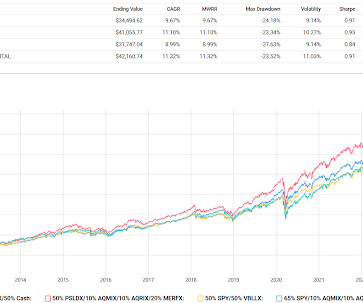

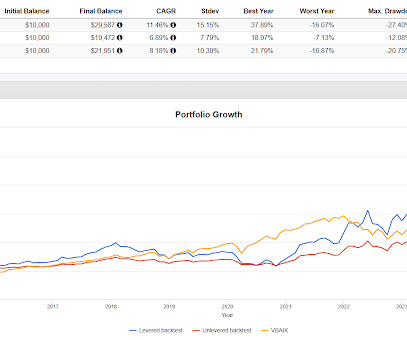

Portfolio 1 is 70% allocated to a low vol equity proxy and 30% to an alternative strategy that is intended to look like a horizontal line that tilts upward. Portfolio 2 is 100% Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 portfolio and Portfolio 3 is the SPDR S&P 500 (SPY).

After a strong finish in 2020 and very solid returns in 2021, we’ve seen a lot of market volatility so far in 2022. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risk tolerance. Also assess your feelings about your portfolio’s performance.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

Ages ago I wrote a couple of posts about Boston University professor Zvi Bodie and his belief that stocks actually get riskier the longer you hold them and his belief in allocating a lot to TIPS, with just a little allocated to risk assets. Bodie still believes in this, here's a paper he wrote in 2020 , doubling down.

The idea is that you get the full beta (stocks and bonds) return with just a portion of the portfolio often with futures or some other form of leverage, leaving dollars left over to add alternatives all in pursuit of better nominal returns or better risk adjusted returns. The fourth portfolio more closely aligns with what we do here.

Early this week, I referenced a comment by Meb Faber that essentially said, you did what you did to try to protect your portfolio, hopefully it's working but that this point you just need to sit back and relax. I will say, I do think I'm pretty good at remembering cross asset dynamics from those previous events.

When I was working on yesterday's post I stumbled back into the Return Stacked 60/40 Absolute Return Index which is a portfolio funds blended together with a lot of embedded leverage in pursuit of capital efficiency. It's a very sophisticated portfolio. Here's what it is in the portfolio and the notional exposures.

The more exciting your portfolio, the worse your performance is in this bear market. This is in stark contrast to the FOMO days of 2020 and 2021 when it felt like the only place to put your money was the. Boring is better this year in the markets.

Torsten Slok blogged about how ineffective bonds have been in terms of providing any return or diversification benefits lately in the context of a 60/40 portfolio. The third portfolio is just the Vanguard Balanced Index Fund (VBAIX). Despite all the leverage, Portfolio 1 has a very smooth ride including up a lot in 2022.

Johnson joined the firm in 1988 and held leadership roles in all its major divisions before becoming CEO in February 2020. She also led the historic acquisition of Legg Mason in 2020, and Putnam in 2023, with the organization now managing more than $1.5 trillion globally.

If one stock makes up more than 10% of your overall asset allocation, it’s probably too much. A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Diversifying Around It: Balancing the portfolio by investing in assets that offset the concentrated position’s risk.

Barron's wrote about the difficulty of spending down accumulated assets in retirement. As is often the case for this subject, someone talked about building a dividend portfolio and living off the dividends. The yields of Portfolios 1 and 2 are now higher than SCHD due primarily to XYLD having a higher payout than it used to.

interest rates since 2020. wsj.com) Fund management What are the most owned private companies in mutual fund portfolios? morningstar.com) Breaking down which assets are still ripe for active management. citywireusa.com) Women are still not making much headway in the asset management business. Think Elon Musk.

Kansas City won the 2020 game and the market had an up year in spite of the impact of COVID-19. What impact have the solid stock market gains of the past three years had on your portfolio? Perhaps it’s time to rebalance and to rethink your ongoing asset allocation. View all accounts as part of a total portfolio.

After a significant drop in March of 2020 in the wake of the pandemic, the S&P 500 has staged an amazing recovery. The index finished 2020 with a gain in excess of 18%. This is the time to review your portfolio allocation and rebalance if needed. Manage your portfolio with an eye towards downside risk. Click To Tweet.

( Wall Street Journal ) see also Five Revealing Pictures : Professional money managers do well on their “slower”, buying decisions (actually well enough to beat benchmark portfolios!). trillion dollar in client assets. She has been CEO since February 2020. It should become a public resource available to all. (

. ~~~ About Jeremy Schwartz: Jeremy Schwartz is Global Chief Investment Officer of WisdomTree, leading the firm’s investment strategy team in the construction of equity Indexes, quantitative active strategies, and multi-asset Model Portfolios. But when you buy a broad market portfolio, You’re getting that diversification.

drop in the first 48 trading days of the year marks its worst start since 2020, such declines are not unprecedented. Right now, your clients dont just need portfolio management; they need perspective. For context, Phil Blancato, chief market strategist at Osaic, points out that while the S&P 500s 6.1% They need to hear from you.

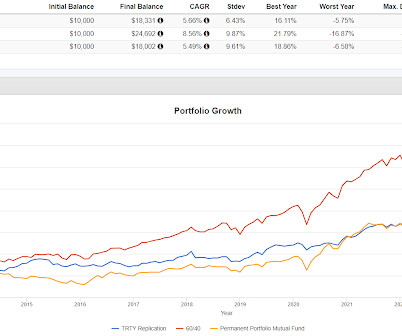

The starting point today is the that Rational ReSolve Adaptive Asset Allocation Fund (RDMIX) has gone through a strategy change, renaming as the ReturnStacked Balanced Allocation & Systematic Macro Fund and keeping the same symbol. " I backtested as follows with Portfolio 3 below being Vanguard Balanced Index Fund (VBAIX).

My back-to-work morning train WFH reads: • Big Investors Are Giving Up on Crypto Markets Going Mainstream : Bitcoin as a portfolio diversifier hasn’t worked for investors Crypto won’t ‘find a home in institutional asset allocation’. Bloomberg ). Wall Street Journal ). • Morningstar ). Institutional Investor ). USA Today ).

There's no fact sheet yet and while the holdings are available, the asset allocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly). It did decline about 5% in the 2020 Pandemic Crash and in 2022 it was up 1.36%. The backtest runs from the start of 2011 to the end of 2020.

Fundamental Analysis of Ujjivan Small Finance Bank We will begin with understanding the services offered by the Bank, its Net Interest growth, and its Deposits & assets growth. Ujjivan SFB is majorly into micro banking, providing small credit facilities with an asset base of 17,401 Cr. These deposits grew by ~40%, from Rs.

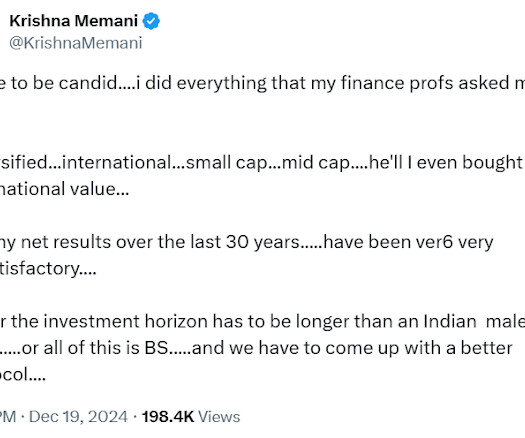

GAA stands for Global Asset Allocation and it has been lagging for 15 years. That leads to a Tweet from Krishna Memani who worked at Oppenheimer for a long time and who has been running the Endowment at Lafayette College since 2020. This slice of the portfolio will go down more often than not, it is a tool to smooth out the ride.

I want to continue the conversation with what I think turns out to be a different take on the traditional 60/40 portfolio with an assist from portfoliovisualizer. MENYX is an equity portfolio but the beta hovers around 0.7 Portfolio 2 is 100% SPY and Portfolio 3 is 100% VBAIX. And I set Portfolio 1 to rebalance annually.

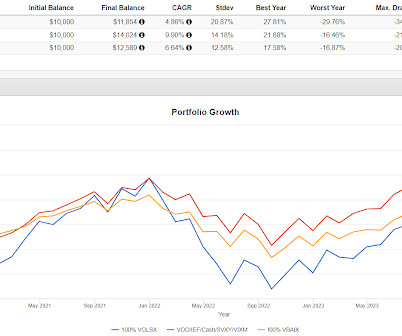

Some other alternatives do their own thing in such a way that they complement equity exposure to reduce volatility and drawdowns without lowering the long term growth of the portfolio. It offers this pie chart to show its current asset allocation. The time frame is so short because VOLSX only goes back to 2020.

MCW also did great in 2021, 2020 and 2019. A portfolio with an enormous weighting to one or two broad based factors is not really what I do but it clearly can work but just like any other strategy you can find, it won't always be optimal. Speaking of AI, Grok seems to like the portfolio. Occasionally of course, MCW gets pasted.

They run over $800 billion in client assets, and Kristen’s group, the North American Group, is responsible for about half of the revenue that that massive organization generates. BITTERLY MICHELL: … across asset classes is the way that I think about it. perspective, how you hold your assets is just as important as what you hold, right?

The idea of building an All-Weather portfolio of course has its appeal. The basic idea is to be much less volatile than the broad market or the typical 60/40 portfolio. It raises the question though of how much performance should an investor expect or be willing give up for the potential emotional comfort of an All-Weather portfolio.

New York Times ) see also Why the Right’s Bud Light Boycott Worked : After 2020, brand politics moved left—and some consumers revolted. He manages a diversified portfolio of late-stage growth equity in technology, consumer, health care, and financial services sectors. trillion in client assets.

I stumbled into an old podcast from Resolve Asset Management that looked at the lack of differentiation from most factors and how to seek out "orthogonality" to get better diversification. And because I think it's related, I wanted to put another simple, Permanent-inspired portfolio on the table to discuss with Portfolio 2.

The assets change, the companies change, the people change. The 2020 and 2021 inflation was the tsunami. Now, many people will look at the SIVB situation and blame their poor risk management of the securities portfolio. And the earthquake was the irrational boom that occurred in 2020/21. Markets change over time.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content