This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

American Prospect ) see also Six Ways Existing Economic Models Are Killing the Economy : The alleged science doesn’t match up to the real world. million that cast ballots in the 2020 race when there was also a presidential primary. His textbook “ Investment Valuation ” is the standard in the field. More than 1.7

I have been fairly vocal that inflation has peaked , the Fed has already overtightened, and they run the risk of doing too much economic damage fighting a demon that has already been exorcised. Maybe this economic slowing results in a mild shallow recession, maybe not. Not So Fast (April 3, 2020). 50% chance ). Countertrend?

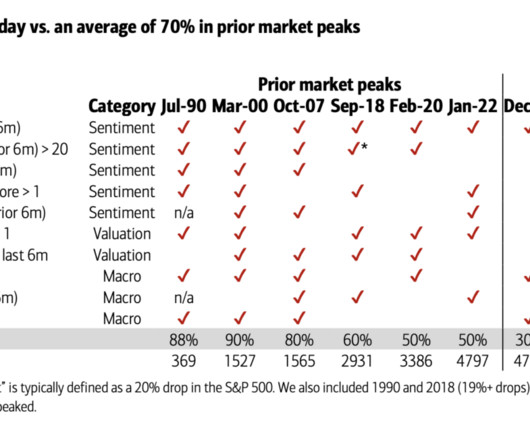

She observes it is less about the things investors tend to focus on — “technical analysis, geopolitics, behavioral finance and even skirt hemline trends” — and more about specific measures she tracks in sentiment, valuation, macro-economic areas. The table above shows the major market peaks going back to 1990.

After a monstrous 68% recovery from the March 2020 pandemic low, and another nearly 30% gain in 2021, markets decided to have one of their all-too-regular spasms. Recall John Kenneth Galbraith’s observation: “The only function of economic forecasting is to make astrology look respectable.” Blame whatever you want – Too far, too fast?

Global Leaders Investment Letter - Q4 2020 jharrison Mon, 02/01/2021 - 08:25 Just want the PDF? One of the most important investing reminders of 2020 was around one of the few sources of investment edge: time. When does crowd psychology take hope for economic return beyond what valuation can support? What is Space?

Global Leaders Investment Letter - Q4 2020. One of the most important investing reminders of 2020 was around one of the few sources of investment edge: time. The power of our clear and disciplined process was evident throughout 2020 as it enabled us to focus on our long investment horizon during a stressful and uncertain period.

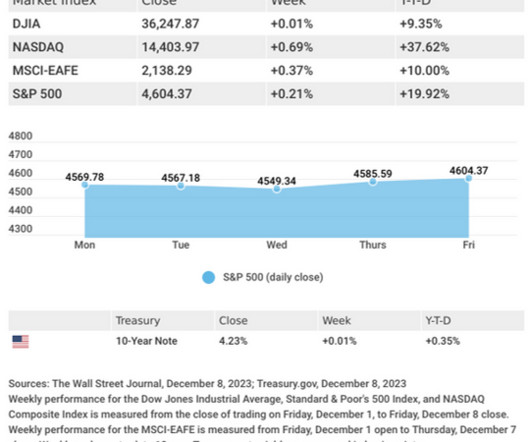

The Dow registered its worst losing streak since 2020. 8 This Week: Key Economic Data Tuesday: Federal Open Market Committee (FOMC) Meeting Begins. Source: I nvestors Business Daily – Econoday economic calendar ; December 10, 2024 The Econoday economic calendar lists upcoming U.S. Retail Sales. Business Inventories.

The Chinese market has struggled since 2020 due to COVID-19, real estate issues, and tech company crackdowns. Additionally, foreign investors are shifting funds from India to China, attracted by lower valuations. These valuations reflect different economic conditions and investor sentiments in each country.

You graduate Harvard in 1990, with an Economics and Computer Science degree, perfect for the explosion of the Internet; a PhD from MIT and Information Technology in ‘96. So along those lines, there are some venture firms that don’t really seem to care a lot about valuations and others seem to focus on a little bit.

What I mean by that is that we’re currently navigating the economic bust portion of the cycle where inflation is a falling risk and credit deflation risk arises, in large part, because the Fed has reacted so quickly to bring inflation in. The 2020 and 2021 inflation was the tsunami. You don’t have to pick just one.

Not only was the economy more open last year, but those quarters benefited from consumers making up for low spending in 2020 and from large amounts of government aid. . Valuations Could Move to a More Normal Range . The decline in the equity market pushed valuations down to levels in line with the period between 2015 and 2020.

million, the lowest level since May 2020 [Figure 1]. The National Association of Home Builders (NAHB) index, another important housing metric, fell in August to below 50 for the first time since May 2020. Traffic of prospective buyers, a leading indicator of future sales, also fell to its lowest since May 2020.

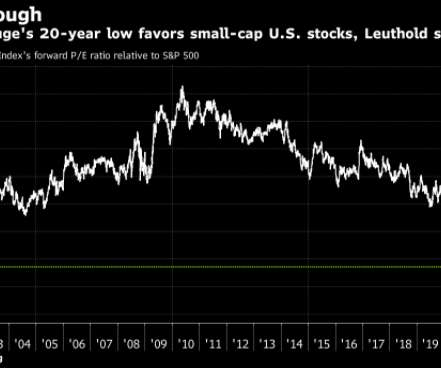

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. But generally starts with the economic cycle. Where are you in the economic cycle? I, I love that area.

With valuations still high, the threat of a recession still looms over the economy, ushering in a prolonged period of low returns across the market, from stocks and real estate to corporate profits, as well as elevated inflation and unemployment rates. But for long-term prosperity in the U.S.

Pockets of attractive valuations exist despite above-average valuations in some high-profile areas of the market. The measure is at 80.7%, exactly where it was a year ago and higher than at any point between July 2001 and February 2020. Following the huge 11.2% But does a strong labor market raise inflation concerns?

DOWNLOAD OUR 2024 MARKET OUTLOOK The Macroeconomic Backdrop As we look to the year ahead, our proprietary Leading Economic Index (LEI) indicates even lower odds of a recession than 2023. Our Market Views This economic environment should support solid earnings growth and improved margins, leading to a good year for markets.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Since 1995, there are four rather distinct periods during which forward earnings estimates for the S&P 500 Index declined, tied to a specific event and/or economic downturn. by year-end.

The railways, like the veins of the country, connect states, making it very economical to transport goods across India as well as to the ports, from where they will be exported to the world. The Dedicated Freight Corridor (DFC), which began operation in 2020 achieved the milestone of running one lakh trains. 2022 ₹1,181.74 ₹49.65

The official arbiter of business cycle dating is the National Bureau of Economic Research (NBER). had never before experienced the massive swings in economic activity during the 2020 pandemic, making even the current analysis more difficult. The economic growth outlook has weakened. Of course, the U.S.

Top economists, Federal Reserve governors and Wall Street strategists – many with PhDs and decades economics experience and education – didn’t see this coming. But at the start of the year, equity valuations were high and yields were historically low. The chart below shows the U.S. 10 Year Treasury around 1.5% less than a year ago.

This can be due to various reasons like global economic concerns or shifts in investment strategies. Years Amount (in crores) 2020 170260.39 High Valuations and Sector Underperformance which Disappointed FIIs Most of the FIIs sold Indian stocks due to high valuation concerns and sector-wise underperformance. 2021 25750.2

jump in productivity represented the fastest pace since the third quarter of 2020. 5 This Week: Key Economic Data Tuesday: Consumer Price Index (CPI). Source: Econoday, December 8, 2023 The Econoday economic calendar lists upcoming U.S. The report also showed unit labor costs falling at a 1.2% Jobless Claims.

Hiring also seems to have pulled back a lot, with the Job Openings and Labor Turnover Survey (JOLTS) telling us that the hiring rate (hires as a percent of the labor force) has pulled back to 3.3% — a rate we last saw in 2013 (excluding the peak pandemic months in 2020). Right now, that’s running at a 3-month annualized pace of 4.4%.

By Joe Nocera Entering into a crisis is not the time to figure out what you want to be By Jamie Dimon This burgeoning mass of defined-contribution assets will be ground zero for the upward redistribution of equity assets By William Bernstein The scars of 2008 run deep, not just for economic policymakers but also for their critics By George Pearkes (..)

Yearly dividend payouts have increased every year for the past 10 years, aside from a dip in 2020. As the equity market has struggled against economic headwinds, dividend stocks have gained popularity this year as investors look for a steady source of income that can withstand volatility. billion from the same period in 2021.

Remember that global pandemic back in 2020 called COVID-19 that killed over 350,000 people in the U.S.? What did the stock market actually do in 2020? Bad economic news turned out to be good news for stocks. That same year, the unemployment rate reached a sky-high level of 14.9% (vs. GDP was advancing at a reasonable +1.9%

With the Fed swiftly raising rates and the slowing of economic growth, small-cap stocks have gotten pummeled. That’s positive news for small-caps, especially as the pattern of underperforming before a recession and outperforming as a recession wanes is one that small-caps have followed in 1990, 2001, 2008, and 2020.

From 1980 to 2020, the gap between the economic output of developed and emerging markets has shrunk substantially, with the GDP per capita in emerging markets shooting from 20% to more than 50%. while last year it was 0.77.

In addition to macroeconomic factors, rising COVID infections also risk slowing economic progress. Improving prospects against the pandemic as well as improved prospects for economic recovery should continue to help lift markets globally over time. Chart of the Week. Market Update. S&P sectors were mixed this week.

1 It’s interesting in the context of economic growth as we tend to think of economic growth across “cycles” or repeating ups and downs. But one of the great lessons I’ve learned over the course of my career studying financial markets and economics is that these things almost always take longer than we expect.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. All our economic actions are taking place across time.

The government’s strong emphasis on the Travel & Tourism sector, recognizing its substantial economic multiplier impact and employment generation potential, further bolsters the outlook. They will receive a direct stake in the new entity, along with an independent market-driven valuation.

As I pointed out last month, we are coming off a heroic advance over the last three years (2019/2020/2021) with the S&P 500 soaring +90%. The hangover from COVID has created significant supply chain disruptions and widespread economic shortages. Source: Trading Economics. Source: Trading Economics.

Commentators continue to shout the doom-and-gloom forecasts of a hard landing recession, but after an economic hurricane in 2022 there are some signs the financial clouds have begun to lift this year. Investors Waiting for Another Flood While the calls for a hard economic landing remain, healthy GDP growth ( +2.9% 1, 2023).

A strong health care sector is not only essential for the wellness of the people but also for strong economic growth. The size of the overall Indian Healthcare market was estimated at US$ 265 Billion in 2020. Revenue (Rs in Cr) 2018 2019 2020 2021 2022. Profit Margin ratios (Rs in Cr) 2018 2019 2020 2021 2022.

Industry Overview India’s GDP is projected to exhibit robust growth exceeding 6% for the fiscal year 2024, indicating a promising economic trajectory. 2020 -385.62 -361.04 2020 -8.6 -9.2 The company has only one line of business, i.e., financing and investment activities and has no activity outside India. 2019 93.99

After the strongest week for stocks since November 2020 , the S&P 500 is just a 16% rip away from taking out new highs. The narrative on the downside made a lot of sense; inflation isn't going away, inventory is building up, the fed has to cool demand, AKA cause a recession, valuations are normalizing, etc. I really don't.

India is a land of agriculture, and to revolutionize the farming sector, a company inspired by Mahatma Gandhi’s economic freedom began to manufacture tractors under the brand name “Swaraj” in the last seven decades. million in 2020, and it is expected to reach & 12,700.8 2020 0 6,555.40 2022 0 2,160.23

One of the most important investing reminders of 2020 was around one of the few sources of investment edge: time. The power of our clear and disciplined process was evident throughout 2020 as it enabled us to focus on our long investment horizon during a stressful and uncertain period. Download it here > What is Time? What is Space?

The S&P 500 Index enjoyed its best month since November 2020 and its best July in over 80 years. The rule of thumb is two quarters of negative GDP defines a recession, but the official definition by the National Bureau of Economic Research is broader than that. There was even a surprise out of Washington D.C.,

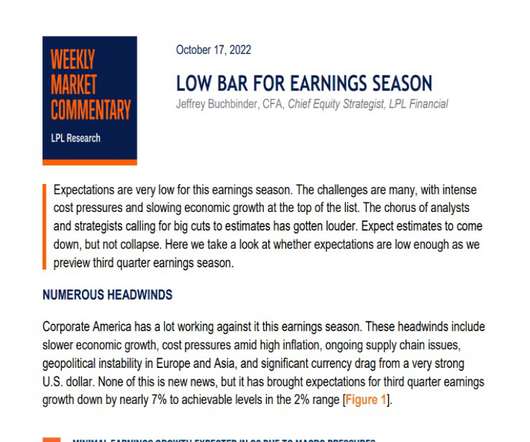

The challenges are many, with intense cost pressures and slowing economic growth at the top of the list. These headwinds include slower economic growth, cost pressures amid high inflation, ongoing supply chain issues, geopolitical instability in Europe and Asia, and significant currency drag from a very strong U.S. Numerous Headwinds.

Most valuation models start and end with the risk-free rate and any movement or even the perception of a change in future policy has an enormous impact on multiples and with-it equity prices. Morningstar is on record saying they expect 2023 to end with a fed funds rate of 1.75% well below where the rest of the street. and today is over 41%.

With a market valuation of ₹3.13 Although the company struggled in 2021-2022 due to high inflation, supply chain disruptions (specifically in the semiconductor industry), and economic uncertainty, the story in 2023 is quite different. The Indian automotive sector is projected to achieve a valuation of US$ 300 billion by 2026.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content