This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Staying long through the 60-day 34% drop during the 2020 pandemic; getting out of the market ahead of the 2022 rate hiking cycle; and getting back in October 2022 for the next bull leg. Consider what you would have had to do over the past 2 decades to be a successful timer. By Jeff Sommer New York Times, Nov. More on this later.

Morgan Housel Finance types tend to focus on attributes like intelligence, math skills and computer programming. We’re going to discuss how to make sure your behavior is not getting in the way of your portfolio. How you behave with money matters more than what you know about money. He is the author of “The Psychology of Money.”

This piece was inspired by this fantastic Josh Brown rant on CNBC about how the 60/40 stock/bond portfolio isn’t dead. The 60/40 stock/bond portfolio is the gold standard of portfolios. The math on the 40% slice is much cleaner. Give it a watch. I don’t love a standalone bond aggregate as a 40% bond slice.

First, is the math right based on my numbers? I think it can be a productive portfolio addition betting on the asymmetry which of course argues for starting very small. The above two portfolios are pretty consistent with a lot of the work we do here. How can it solve anyone's problem?

A portfolio that goes narrower than an S&P 500 500 or total market fund probably has some exposure to low vol, dividends and the others. And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out.

My back-to-work morning train WFH reads: • Ken Griffin’s Hand-Picked Math Prodigy Runs Market-Making Empire : Citadel Securities CEO Peng Zhao left for college at age 14, caught Griffin’s eye early in his career and built systems now mopping up market share. TKer ) • The Debt Ceiling Dispute Raises the Risks for ‘Risk-Free’ U.S.

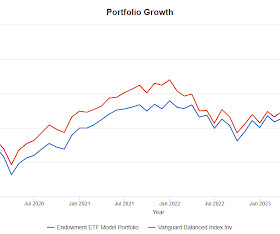

The "endowment" result is very close to red line VBAIX every year except 2020 when it lagged by almost 600 basis point and 2022 when it outperformed by about 500 basis points. If any of us had constructed this portfolio and implemented it for ourselves, it would have been a very acceptable result.

So I took it upon myself to go off and took a course in bond math, took another course in derivatives and realized the underlying fundamental concepts were barely, I mean, it wasn’t even high school math in most cases. I didn’t know what any of these terms meant. And there was a problem with 168 of them at the end of 2008.

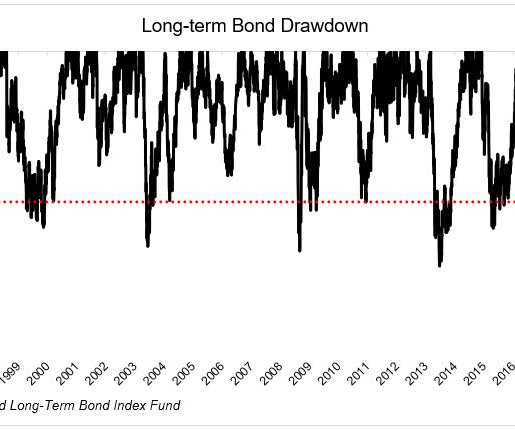

This blog has pretty much evolved into 100 ways to build a portfolio without bonds. The article devoted a good amount of space to bond market math, focusing on the pain of owning the iShares 20+ Year Treasury ETF (TLT) and bond funds in general. There is nothing that says TLT must get back to the $171 dollars it traded at in 2020.

My Two-for-Tuesday morning train WFH reads: • Stock Pickers Never Had a Chance Against Hard Math of the Market : In years like this one, when just a few big companies outperform, it’s hard to assemble a winning portfolio. 2020 Pandemic Panic ?!? ( Businessweek ) but see With cash earning 5%, why risk money on the stock market?

Two of the three strategies have traded sideways in the 2020's. Simple math, it looks like the carry index has compounded at less than 3%. If you use the fund in the manner that I think they intend, a blow up for the stocks and managed futures ETF would be a setback for a portfolio but not a catastrophe.

Here's a quote I saw attributed to Barry Ritholtz: “The Best Portfolio is probably the one which sacrifices a bit of performance, but helps you sleep at night.” Over the last five years, it missed out on the stock market rally until late 2020 when it went parabolic, then drifted lower for much 2021. Cannot be done?

But last year, 2020, how do you look at these breaking new stories and all the buzz and mania around an IPO for both good and bad? RITHOLTZ: So let’s talk about some imbalances, and I’m thinking about the sort of meme stock mania that began in 2020, when everybody was stuck at home during the pandemic, and just exploded in 2021.

It doesn't look like an investment grade bond proxy and I would note that on a price basis it essentially fell the same amount as the NASDAQ during the pandemic crash in March 2020. PUTW maybe snapped back half of what the S&P 500 did in March/April 2020. The nucleus of non-gameover portfolios will always be equities.

That is correct, technically but whatever you're looking for from REITs, or private equity or any of the others, you're not going to see it impact the portfolio as part of an index fund. Mistakes during those types of events are what managing portfolios is all about.

As a quick reminder, a 67% allocation to 90/60 generally equates to a 100% allocation to a 60/40 portfolio like you might get from Vanguard Balanced Index Fund (VBAIX). For this post I assembled a less dramatic portfolio more in line with Krom's thinking. The math shows the NTSX/ARBIX/BTAL combo would be down 14.7%

I — I loved math, but really, I was going to go down that literature route more than anything else and — and study Spanish literature. And so, getting to your question about equities where we’re positioned right now, equities absolutely can conserve an important part in the portfolio. I was econ and kind of geeky.

Her job is portfolio and product solutions and that means she could go anywhere in the world and do anything. One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics.

WENGER: Well, we reserve a lot of funds for follow-on, and we have a very sort of, I think, sophisticated reserves methodology that we’ve honed over many funds cycles now, where we actually built kind of a Monte Carlo analysis of the portfolio to see how much money we think we need to keep in reserve. RITHOLTZ: Right. There you go.

You would offer three of their stock picks where they were probably touting stocks they wanted to unload from their portfolio. But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. That’s exactly right.

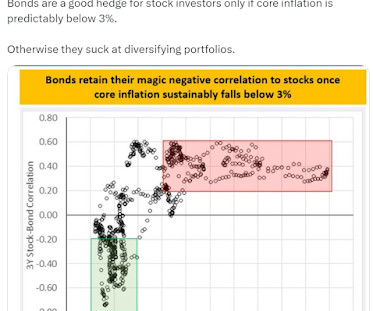

A little more specifically the need for diversified portfolios persists with the implication that bonds are the way to get this done. This chart contributes to the logic supporting a 60/40 portfolio. The blue line is equities and the red line is bonds up until the end of 2020. Portfolio 2 above has 65% in growth.

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. Initially I joined to help them manage their equity portfolio. It was the exact same trade. I buy everything.

Risk parity portfolios are particularly vulnerable when their active weighting algorithms fail to predict shifts in asset correlations." In the same period Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 portfolio compounded at 10.89% with a standard deviation of 12.43%. The table/chart goes back to FAPYX' inception.

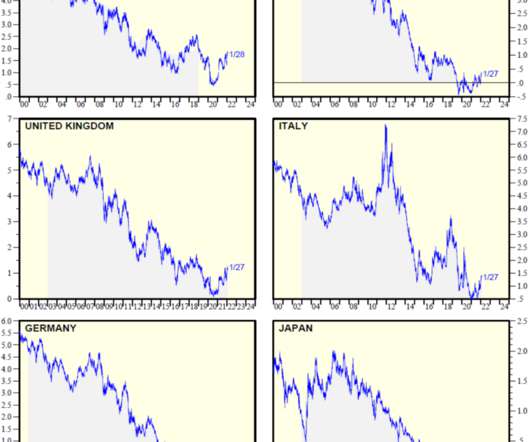

As I wrote about in January 2020, starting yields tell you pretty much all you need to know about what your future returns will look like. Unfortunately, the math isn't on our side anymore. Two, I don't know anybody who holds an entire portfolio of long-term bonds. The increase in income quickly made up for the price decline.

T he stock market has been like a rocket ship over the last three years 2019/2020/2021, advancing +90% as measured by the S&P 500 index, and +136% for the NASDAQ. Math Matters. I did okay in school and was educated on many different topics, including the basic principle that math matters. Source: Calafia Beach Pundit.

Part of the math that determines options premiums is the risk free rate of return from T-bills. We've also looked at countless ways to incorporate a small allocation to covered calls funds to help reduce portfolio volatility, so using them as alts in a matter of speaking. Covered call funds have many favorable attributes.

So I came down, met with our head of the portfolio review department, which oversees our external managers, met with our head of brokerage, and then met with the head of bind indexing, who was Ken Volpert at the time. And she was like, “You should come down and talk to some people at Vanguard.”

A 20% allocation to the average systematic trend fund in a 60/40 portfolio would have resulted in an annual drag of about 1.45 Turns out the math checks out using Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 equities/fixed income portfolio and the Guggenheim Managed Futures Strategy Fund (RYMFX).

I’m good at math and science and you know, I always had an idea what go into business, but I felt that electrical engineering would be a good foundation. You know, I, it always, I I see different numbers all the time, so it’s always kinda like, who’s math if you will? 00:02:16 [Speaker Changed] Me too.

While the data isnt as black and white as other aspects of finance, the impact of behavioral finance is clearjust consider the Covid-induced crash in February 2020 or the meme stock phenomenon of 2021 (to name a few more recent events). Behavior Finance and Your Portfolio So much of the concept of investing is about logic, math, and numbers.

00:21:42 [Speaker Changed] Yeah, I mean, I think, well, what set us up was we, you know, we got the low right in 2020 for the right reasons. So we were very aggressive in 2020 and 2021. And nobody paid him any attention back in 2020. So right, because we agreed with Professor Siegel in April of 2020. And we did.

And I did the math, and I think at that point in time, roughly speaking, assets in ETS were roughly just 10 percent, 12 percent of assets in mutual funds and I was pretty convinced that that number was to increase significantly. BERRUGA: So many of our clients were struggling to find alternative sources of income for their portfolios.

ANAT ADMATI, PROFESSOR OF FIANCE AND ECONOMICS, STANFORD GRADUATE SCHOOL OF BUSINESS: So, my journey starts where I took a lot of math. I was good in math and I love the math. So, I was kind of, in my romantic mind when I was in my early 20s, I was going to take but not give back to math, that kind of thing. ADMATI: Yes.

And when used for ROE, as per the basic rule of math, if the denominator decreases, the fraction as whole increases i.e, The product portfolio includes dominant brands such as Pampers, Gillette, Whisper, Old Spice, Head & Shoulder, Ariel, etc. Company 2018 2019 2020 2021 2022 Average 5 yr. higher ROE. Nestle India Ltd.

The social impact score is especially helpful for analyzing and sourcing MBS outside of the growing, but still limited, labeled bond universe, allowing us to build a more diversified portfolio. According to the National Association of Realtors, low-income homeowners comprised just 27% of all homeowners in 2020, down from 38% in 2010.

One of our colleagues, Ken Stuzin, likens portfolio construction to Darwinian Investing – it is about survival of the fittest. In a concentrated portfolio, it is the losers that kill you. What sort of hit rate should we then expect within their portfolio? 5 As Table 2 below highlights, this team appears to be seriously good!

But you know exactly how they’re going to interplay within a portfolio, hugely powerful. You know, it’s not the equity market, and I run some big equity portfolios, you know, different. But, you know, it’s been in a portfolio for a long time. Last year, it’s in our tactical portfolios.

But in the Mustachian Era (the years since 2011 when I started writing this blog ), there has only been one: the 2020 Covid Crash which only lasted about a month. It’s fun math – a 20% drop in prices means you get 25% more shares for your dollar, and a 50% drop means twice as many , or 100% more shares per dollar invested.).

We discount each year at our 10% minimum weighted average cost of capital (WACC) and some infinite series maths gives us the basis for some rough approximations 2. Today the Global Leaders portfolio cash flow duration in real terms is in the 15 to 17-year range using this calculation. The last time U.S. and appeared to be going higher.

BRYANT: So money, unlike math, money is highly emotional. I mean, there’s 50,000 kids in the Atlanta public school system, so you can do the math there. I believe I love math because it doesn’t have an opinion, that’s a Melody Hobson quote. RITHOLTZ: Right. BRYANT: Number two, money is emotional. RITHOLTZ: Yes.

The current record – set in May 2020 using a tricked out silver Audi S6 disguised as a Ford Taurus Police Interceptor during the height of the recent pandemic, when roads were generally deserted – is 25 hours 39 minutes. More than that, however, we had purchased tickets for Disneyland for everyone for Wednesday. We wanted to go!

SEIDES: But market returns across — RITHOLTZ: The past decade, 2010 to 2020, we were what? That’s a really easy portfolio to create. It allows you to understand, generally speaking, what is a reasonable beta for that whole portfolio. RITHOLTZ: Oh no, it’s much worse. SEIDES: It’s lower. It’s lower.

.” It’s really helpful to have had five other meetings with people who sit at analogous funds that had losses that were just as big, and in fact, they may have contributed to those losses more and be able to tell him, first off, your fund, just by my math, has a $250 million management fee. LMR in 2020 was 4.6

Three subsequent sales in 2020. 00:40:26 [Speaker Changed] They, they know, they know math, they know math. 00:49:16 [Speaker Changed] You know, I have a, a chapter and, and an upcoming book about, you are responsible for your portfolio. Nobody cares about your portfolio. That’s a whole nother thing.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content