This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When you get it wrong, it crushes your retirement plans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. But when they get market timing wrong, they lose subscribers. I sure as hell don’t want to either.

Morgan Housel Finance types tend to focus on attributes like intelligence, math skills and computer programming. You can know everything about math and data and markets, but if you don’t control your sense of greed and fear and you’re managing uncertainty in your behavior, none of it matters. What happened in March of 2020?

First, is the math right based on my numbers? I didn't want to backtest too far back because Bitcoin had massive gains in 2017 and 2020 that might not be repeatable. If we guess just 2 billion people, and that is just a guess, and divide that into the 15.2 How can it solve anyone's problem?

And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out. Portfolio 1 lagged by quite a bit in 2019 and then even more in 2020. YSPY sells put spreads on a 3x fund.

My Two-for-Tuesday morning train WFH reads: • Stock Pickers Never Had a Chance Against Hard Math of the Market : In years like this one, when just a few big companies outperform, it’s hard to assemble a winning portfolio. If you’re depending on income to fund your retirement, 5% rates are a blessing. 2020 Pandemic Panic ?!? (

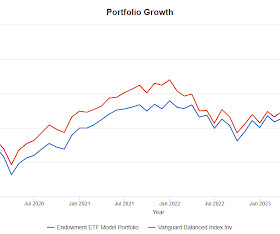

The "endowment" result is very close to red line VBAIX every year except 2020 when it lagged by almost 600 basis point and 2022 when it outperformed by about 500 basis points. It did worse in the 2020 Pandemic Crash by 200 basis points which isn't problematic for how quickly everything snapped back. Is it this?

But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. I did it during the coronavirus collapse in 2020, and I did it again in 2022. I realized I had enough to retire if I wanted to. I did it in 2000, 2002.

The article devoted a good amount of space to bond market math, focusing on the pain of owning the iShares 20+ Year Treasury ETF (TLT) and bond funds in general. There is nothing that says TLT must get back to the $171 dollars it traded at in 2020.

The math behind Universal Life Insurance Interest Rates is a twisted web and most consumers are deceived. Know how the math works so you can see the potential risks that may exist with your policy. This correction was updated in 2020 with AG 49A and again in May 2023 with AG49B. Don’t be fooled! Are you disturbed yet?

Two of the three strategies have traded sideways in the 2020's. Simple math, it looks like the carry index has compounded at less than 3%. I said I was interested enough to start following it, having no idea what to expect. This chart from the paper doesn't paint a rosy picture. The red line for T-bills is price only.

There's other math about outperformance but also the observation that momentum is prone to crashes. You don't see that before the 2020 Pandemic Crash though. The current event, rolling over slowly is more typical of bear market behavior as opposed to the crash in 2020. Here's the last year.

Social Security Retirement Planning . By Michael Garry Yardley Wealth Management October 26, 2020. Around 65 million Americans will receive more than $1 trillion in benefits during 2020, according to the Social Security Administration (SSA). Fleshing out current concerns and common myths.

It doesn't look like an investment grade bond proxy and I would note that on a price basis it essentially fell the same amount as the NASDAQ during the pandemic crash in March 2020. PUTW maybe snapped back half of what the S&P 500 did in March/April 2020. PBP is the Invesco S&P 500 BuyWrite ETF.

A quick excerpt from a post a couple of weeks ago about retirement misconceptions. I would much rather withdraw 10% or more per year from my retirement accounts and do it without taking any principal. Part of the math that determines options premiums is the risk free rate of return from T-bills.

Alicia’s Experience One of my earliest experiences when I first decided to get into financial planning was participating in the Financial Planning Association’s Externship Program in the summer of 2020. women tend to live longer, making it much more important to plan for a longer retirement) or a subjective one (e.g.

In the case of real estate a 2.29% weighting and for "private equity" companies it's about 17 basis points (looked at XLF holdings and then did a little math), that's just not going to move the needle. You may agree with Jack about not needing those things, that's valid, my point is that owning an index fund isn't a proxy for them.

There was a lot of content from various places over the weekend about whether it is time to go back into bonds, what retired investors should do for yield and even whether retirees are better off going 100% into equities. The blue line is equities and the red line is bonds up until the end of 2020.

So I took it upon myself to go off and took a course in bond math, took another course in derivatives and realized the underlying fundamental concepts were barely, I mean, it wasn’t even high school math in most cases. I didn’t know what any of these terms meant. And I thought, great, I just made partner. SALISBURY: Sure.

I’m good at math and science and you know, I always had an idea what go into business, but I felt that electrical engineering would be a good foundation. You know, I, it always, I I see different numbers all the time, so it’s always kinda like, who’s math if you will? 00:02:16 [Speaker Changed] Me too.

But in the Mustachian Era (the years since 2011 when I started writing this blog ), there has only been one: the 2020 Covid Crash which only lasted about a month. It’s fun math – a 20% drop in prices means you get 25% more shares for your dollar, and a 50% drop means twice as many , or 100% more shares per dollar invested.).

Demand is likely to continue as more and more people in the Boomer generation reach retirement. If you’re good with math, then turning to financial planning or accounting or opening up a similar company could be one of the best recession proof businesses to start! They aren’t likely to get rid of the person who knows the numbers.

Commodities can easily go down with equities or in the case of the pandemic crash, the Invesco DB Commodity Tracking Fund (DBC) dropped more than the S&P 500 during the Pandemic Crash of 2020 and took longer to snap back. The math shows the NTSX/ARBIX/BTAL combo would be down 14.7% and that is the number I will assume.

The math is only off by a shade using leverage via UST and a little bit of SSO, remember RPAR is leveraged. I find this to be interesting but anyone needing normal stock market growth in order for their retirement plan to work, probably isn't going to get it from any of these portfolios. The Replication is based on this from RPAR.

ANAT ADMATI, PROFESSOR OF FIANCE AND ECONOMICS, STANFORD GRADUATE SCHOOL OF BUSINESS: So, my journey starts where I took a lot of math. I was good in math and I love the math. So, I was kind of, in my romantic mind when I was in my early 20s, I was going to take but not give back to math, that kind of thing.

One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics. So people really ask you, you take French and can you do math. So I applied to Maryland State retirement.

Turns out the math checks out using Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 equities/fixed income portfolio and the Guggenheim Managed Futures Strategy Fund (RYMFX). A 20% allocation to RYMFX would have helped in the first three months of 2020 albeit with less of an impact. percentage points.

I don’t even know what it’s going to be yet, but I mean, I’m not retiring. 00:21:42 [Speaker Changed] Yeah, I mean, I think, well, what set us up was we, you know, we got the low right in 2020 for the right reasons. So we were very aggressive in 2020 and 2021. And nobody paid him any attention back in 2020.

However, by doing a little math, you can easily determine your hourly wage from your annual salary. For 2020, the federal poverty level for a single person without dependents is $12,760. For example, for a family of four in 2020, the poverty level is $26,200. 55K a Year Is How Much an Hour? However, in general, $26.44

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. People earn wages, whether it’s a retirement account or a tax deferred account or just an investment account.

I — I loved math, but really, I was going to go down that literature route more than anything else and — and study Spanish literature. BITTERLY MICHELL: … difficult situations for those who were retiring, right, and those …. And I remember March 2020, there was no thought in our mind that we were going to work from home.

Over the last five years, it missed out on the stock market rally until late 2020 when it went parabolic, then drifted lower for much 2021. We dove in on the math at my old URL (sad story, no longer exists) and the math checks out. Sometimes it outperforms the S&P 500 and sometimes it doesn't.

It has to be such a different set, the retirement planning is different, the safety net is different. People in Spain when I was growing up in the ‘80s and ‘90s, they expect to just retire and have the government give them like a paycheck every month. 2020 was a huge year. You know, we had a really good 2020.

And when you saw the US Ag down 13% last year, for folks, again, who are investing for retirement and in their 529 plans, they’re not concerned about it. But when you translate that to folks who might have a heavy municipal bond portfolio, and those folks who are in retirement, and they don’t like principal losses.

I think what’s important, though, and what’s key is that we found ourselves at a very interesting point in time, in 2020, in the wake of George Floyd, in the middle of COVID. My dad was a naval officer who retired shortly before I was born. What did your dad retire from doing? Tell us about those experiences.

” After the Dodgers were retired in order in the bottom of the eighth inning, Gibson swung his aching legs down from the training table to hobble toward the clubhouse. 23KGibby @Dodgers @MLB 11:29 PM ∙ Oct 15, 2020 12,090 Likes 2,510 Retweets Gibson raged at the TV screen. “How you doing, big boy?,” The coolest.

So the fact that I had a sociology degree really didn’t impede, I think getting into business Barry Ritholtz : And you end up in like what some would think of as kind of a dry, legalistic part of Fidelity, the ERISA Division, which focuses on retirement accounts. Three subsequent sales in 2020. That’s a whole nother thing.

SEIDES: But market returns across — RITHOLTZ: The past decade, 2010 to 2020, we were what? RITHOLTZ: So hold the duration risk aside with those two, but just for an investor in treasuries, I know you’ve done the math before. Probably the first one I’m ready to retire, which is a post-lockdown question.

.” It’s really helpful to have had five other meetings with people who sit at analogous funds that had losses that were just as big, and in fact, they may have contributed to those losses more and be able to tell him, first off, your fund, just by my math, has a $250 million management fee. LMR in 2020 was 4.6

And so if you compare that to today, if you remember Oaktree raised $15 billion fund in 2020, on its own. So you retire in 2018. For example, you talk about the 2020 distressed cycle, and it’s interesting to me that it was so short, so shallow. If you think of the biggest bankruptcy in 2020 was Hertz. MIELLE: Right?

And I was a math nerd as a kid. You’re 34th, you’re retiring after 34 years and you trounce what’s really the more appropriate benchmark, I would assume the Russell 2000. So, so you set to retire as portfolio manager this year, you mentioned your two successors. You, you beat the s and p by 3.7%

The 75/50 captures 75% of the upside with only 50% of the downside, the math on that works out favorably over the long term. 2020 was a terrible year for XYLD. If it can deliver on being a less volatile proxy for the S&P 500, while tracking closer to the index than XYLD, how should we define success?

And caring about price versus anything, even if it were immune to intangibles, was not a very good thing until late 2020, since the GFC, so about 11 years. I think, you know, kind of near the end of 2020, maybe people were being quiet about that affiliation for a while. My mom was a math teacher so — RITHOLTZ: Okay.

Let Mr. Market do his thing and we’ll find out how we did when we get ready to retire. Since 2020, their performance has been awful. RITHOLTZ: In 2020, no one even came in second. RITHOLTZ: I think she was plus 160% in 2020, when the market from the lows, the market was up 68%. It’s how math works.

And I, and I really like the application of math and statistics and computer science to markets. You learn the math that can help you with, with market making operations. It’s just not smart on a math basis to do that. And are you saying the recession in 2020 is similar to recession in the 1950s?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content