This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

million borrowers since March 2020. Ginnie Mae loans in forbearance increased by 30 basis points to 1.06%, and the forbearance share for portfolio loans and private-label securities (PLS) increased 6 basis points to 0.43%. Mortgage servicers have provided forbearance to approximately 8.4

million borrowers since March 2020. Ginnie Mae loans in forbearance increased by 5 basis points to 1.11%, and the forbearance share for portfolio loans and private-label securities (PLS) decreased 1 basis point to 0.42%. Mortgage servicers have provided forbearance to approximately 8.5

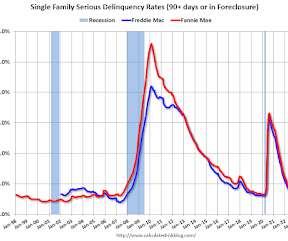

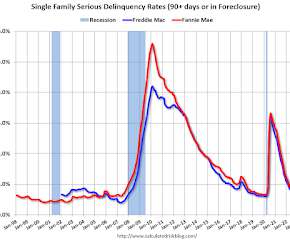

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.41% are seriously delinquent (down from 2.48% in August).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.15% are seriously delinquent (down from 2.34% in October).

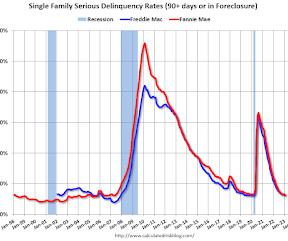

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 1.93% are seriously delinquent (down from 2.04% in February).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.16% are seriously delinquent (down from 2.15% in November).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.34% are seriously delinquent (down from 2.41% in September).

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 0.33% in August The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 6 basis points from 0.39% of servicers’ portfolio volume in the prior month to 0.33% as of August 31, 2023.

From the MBA: Share of Mortgage Loans in Forbearance Decreases Slightly to 0.38% in February The Mortgage Bankers Associations (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 2 basis points from 0.40% of servicers portfolio volume in the prior month to 0.38% as of February 28, 2025.

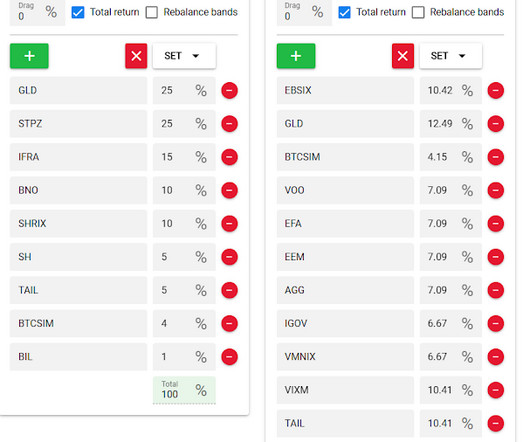

Let's dig in some more on Permanent Portfolio quadrant style. Next is the allocation for the United States Sovereign Wealth Fund ETF that I made up a few days ago and next to that is my most recent attempt from November to recreate the Cockroach Portfolio which is managed by Mutiny Funds. That is a very specialized type of result.

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.60% are seriously delinquent (down from 2.75% in June).

If only the Fed didn’t do X, our portfolio would have been much better” seems to be a terrible approach to managing assets for clients. 2020s : Remained on emergency footing post Covid, despite broad evidence of economic recovery. Following those March 2020 rate cuts, the Fed stayed at Zero until March 2022.

Investors should be considering capturing some of that yield in their portfolios. We’re going to discuss how these changes are likely to affect your portfolios and what you should do about it. My stock portfolio is recovering. 2020 comes. We have a big downturn in 2020. amongst institutional traders.

From the MBA: Share of Mortgage Loans in Forbearance Decreases Slightly to 0.47% in December The Mortgage Bankers Associations (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 3 basis points from 0.50% of servicers portfolio volume in the prior month to 0.47% as of December 31, 2024.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 0.49% in May The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 2 basis points from 0.51% of servicers’ portfolio volume in the prior month to 0.49% as of May 31, 2023.

We can credit three elements for this massive outperformance: -Substantial prices resets: 57% in 2008-09 and 34% in 2020. Fiscal stimulus 2020-22. – Covid Pandemic Crash, March 2020 : Fast and furious, it took a mere 22 trading days from February 19 to March 20 to see a fall of 33.9% The next ~12 years saw gains of 608.5%

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.48% are seriously delinquent (down from 2.60% in July).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.04% are seriously delinquent (down from 2.11% in January).

What’s obvious is that cheaper is better than more expensive; that there are inherent costs in managing an active portfolio that include more than just trading and taxes but research, analysis, PMs, etc. Concentrated portfolio risk. Barry Ritholtz (@ritholtz) August 13, 2020. Lobotomized investing. Dangerous for economy.

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.75% are seriously delinquent (down from 2.86% in May).

Staying long through the 60-day 34% drop during the 2020 pandemic; getting out of the market ahead of the 2022 rate hiking cycle; and getting back in October 2022 for the next bull leg. Consider what you would have had to do over the past 2 decades to be a successful timer.

BAML’s Chief Equity Technician Stephen Suttmeier likens the 2020 crash to the modern version of the 1987 crash: A substantial crash that took place 7 years into the start of a new bull. Secular Bull Market : US stocks are in the 5-6th inning of a bull market. Historical comparisons imply this market may have another 3-7 years to go.

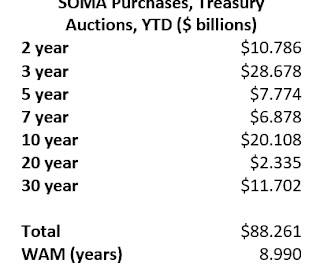

From housing economist Tom Lawler: From the beginning of 2020 to early June of 2022 the Federal Reserves balance sheet more than doubled to an almost inconceivable $8.9 trillion) Agency MBS portfolio with an estimate weighted average life of 8 - 9 years to just slowly roll off adds even more to this private-sector maturity transformation.

downtownjoshbrown.com) A lot of stuff matters beside your portfolio. obliviousinvestor.com) Splitting your portfolio in two. savantwealth.com) The IRS is extending an olive branch to taxpayers who owe money from 2020-2021. (financialsamurai.com) Investing Five ways you lost money in 2023 including overtrading.

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic. The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 0.55% in March The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 5 basis points from 0.60% of servicers’ portfolio volume in the prior month to 0.55% as of March 31, 2023.

Treasuries The MOVE index is at 2020-like levels. twitter.com) 60/40 Portfolio A reason why the 60/40 portfolio isn't working this time around. twitter.com) 60/40 Portfolio A reason why the 60/40 portfolio isn't working this time around. axios.com) Investors are shunning the 20-year Treasury.

The Fed is right about inflation but lacks the appropriate tools to address the 2020 inflation cycle. Regardless, it’s a worthwhile exercise to wargame Fed actions, and consider what they might mean to your portfolio and/or personal finances. The Fed is wrong about inflation, in magnitude and/or its direction. Before inflation falls?

In the stock market, its anyone with a portfolio or 401k/IRA or trading account. Cars are for Driving, Sneakers are for Wearing (November 11, 2020). The Hidden World of Failure (October 23, 2020). September 18, 2020). _. They do not follow the fiduciary rule but instead swap hats on a whim. Previously : Bought or Sold?

This piece was inspired by this fantastic Josh Brown rant on CNBC about how the 60/40 stock/bond portfolio isn’t dead. The 60/40 stock/bond portfolio is the gold standard of portfolios. So yes, as Josh notes in his interview, these criticisms were more valid in 2020 when interest rates were at 0%. Give it a watch.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 0.51% in April The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 4 basis points from 0.55% of servicers’ portfolio volume in the prior month to 0.51% as of April 30, 2023.

Today, the financial plan itself is increasingly becoming not just a ‘value-add’ supporting other services like portfolio management, but rather the whole purpose of (and primary value proposition for) the client relationship to begin with. A lot has changed since 2020, though.

2020 : Pandemic crash of 34%, fastest top fall (but fastest recovery) 2022 : Stocks & bonds both down double digits since 1981 All of these meet the unofficial definition of a bear of a 20% move off of the peak. The GFC and the pandemic were global phenomena; the 2022 market was the worst since 1981 for a 60/40 portfolio.

We work on theoretical portfolios here all the time that blend in strategies that really are negatively correlated or at least very little correlation. Both portfolios have higher standard deviations than the Trinity Replication but much higher returns. Enduring a bear market is about both, behavior and portfolio construction.

Instead, there is a tendency to put too much weight onto the numbers themselves, encouraging a variety of changes and modifications to portfolios due to whatever the latest data suggests. (I have long been a fan of the concept of Strong Opinions, Weakly Held ).

After-tax equity returns from your non-tax-exempt portfolios. To help us unpack all of this and what it means for your portfolio, let’s bring in Ari Rosenbaum of O’Shaughnessy Asset Management, now a division of investing giant Franklin Templeton. So we, for practical purposes, remove those from the portfolio.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 0.26% in November The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 3 basis points from 0.29% of servicers’ portfolio volume in the prior month to 0.26% as of November 30, 2023.

million borrowers since March 2020. Ginnie Mae loans in forbearance dropped 1 basis point to 0.39%, and the forbearance share for portfolio loans and private-label securities (PLS) stayed the same at 0.31%. Mortgage servicers have provided forbearance to approximately 8.1

1 This is significant for two reasons: First, it is a full 5 million more people working today than in January 2020, just before the pandemic struck. It was that 157.087 million people are employed full-time in the United States.1 This is not a popular opinion.

million borrowers since March 2020. Ginnie Mae loans in forbearance increased by 5 basis points to 0.44%, and the forbearance share for portfolio loans and private-label securities (PLS) stayed flat at 0.31%. Furthermore, the performance of both loan workouts and overall servicing portfolios weakened, particularly for government loans.”

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 0.23% in December The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 3 basis points from 0.26% of servicers’ portfolio volume in the prior month to 0.23% as of December 31, 2023.

From the MBA: Share of Mortgage Loans in Forbearance Decreases to 0.31% in September The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 2 basis points from 0.33% of servicers’ portfolio volume in the prior month to 0.31% as of September 30, 2023.

million borrowers since March 2020. Ginnie Mae loans in forbearance increased by 10 basis points to 0.76%, and the forbearance share for portfolio loans and private-label securities (PLS) increased 2 basis points to 0.37%. “The Mortgage servicers have provided forbearance to approximately 8.3

2020: Covid : With the economy closed, people locked down, and local businesses crashing, many were expecting a replay of the previous market crash. If you believed these stories, and acted on them, your portfolio probably did poorly in markets over this era. This was a money-losing set of narratives.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content