This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mike McGlothlin , CFP, CLU, ChFC, LUTCF, NSSA, Executive Vice President, Retirement, at Ash Brokerage , is the 2024 recipient of the Kenneth Black Jr. McGlothlin served on the Society of FSP National Executive Committee from 2018 to 2021 and was National President in 2020-2021. Leadership Award.

Recall last week , we were discussing thinking about the impact of retiring Baby Boomers on the equity markets and of rising rates on housing. The demographic question touches on a big issue: $6 trillion dollars in 650,000 (401k) retirementplans held by 10s of millions of Americans.

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. But when they get market timing wrong, they lose subscribers. I sure as hell don’t want to either.

After a significant drop in March of 2020 in the wake of the pandemic, the S&P 500 has staged an amazing recovery. The index finished 2020 with a gain in excess of 18%. As someone saving for retirement , what should you do now? Approaching retirement and want another opinion on where you stand? Review and rebalance

Optimizing your retirement savings takes more than just making sure your IRA isn’t at risk in this market. Know these 3 ages that can help you get the most out of your retirement accounts. At age 50, workers with certain qualified retirementplans can make annual “catch-up” contributions in addition to their normal contributions.

Kansas City won the 2020 game and the market had an up year in spite of the impact of COVID-19. Approaching retirement and want another opinion on where you stand? Financial coaching focuses on providing education and mentoring on the financial transition to retirement. Not sure if your investments are right for your situation?

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. For high earners, converting an IRA to a Roth IRA while you’re still working could be the worst time of all.

After a strong finish in 2020 and very solid returns in 2021, we’ve seen a lot of market volatility so far in 2022. Smart investors factor this into their plans and don’t overreact. Approaching retirement and want another opinion on where you stand? The S&P 500 index was down about 17.6% Be a smart investor.

Northwestern Mutual published a report about the state of retirement and of course all the numbers are grim. million to retire, up about 50% from 2020, while the average retirement account balance is $88,000. I've been pushing back on the idea of have a number, a retirement number, for a very long time.

The risk of selling volatility this way is that the market gets hit either with a fast decline like the 2020 Pandemic Crash or a slower large decline like in 2022 causing the short puts to get assigned. Munnell along with Teresa Ghilarducci are like the aunties of retirement which I am saying in a positive way. People have busy lives.

But to illustrate the relative protection that bonds may be able to provide compared to stocks, heres what happened to the bond market in the 2008 great financial crisis and recession and 2020 market crash. How do bonds perform during a recession? The chart below shows what happened to fixed income (bonds) in 2008.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Either plan is an excellent choice, particularly if you’re not covered by an employer-sponsored retirementplan. Not exactly.

Key Takeaways: The last two years have been marked by the highest inflation rates in decades; your clients saving for retirement can use this to their advantage through short-term investments, tax deferral, and insurance products offering better benefits. For many people, this might mean retirement.

How To Grow Your RetirementPlan Business In The 2020 Economic Crisis. We’ll review: – How has the retirement landscape been affected by COVID-19? – How can advisors grow their retirement business in the current crisis? I’m super excited to welcome the team at Retirement Learning Center.

The post Is COVID-19 affecting your RetirementPlanning? Is COVID-19 affecting your RetirementPlanning? RetirementPlanning Financial Planning Risk. Over their lifetimes, most people have heard warnings and advice from retirement advisors about various aspects of their plans.

Preparing for retirement is a significant life transition that demands a clear understanding of your financial situation. This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. household was $121,700.

The post 5 Financial Advisor Hacks: A Cheat Sheet for People Saving For Retirement! 5 Financial Advisor Hacks: A Cheat Sheet for People Saving For Retirement! The 24-hour news cycle can be a bit insane these days, especially in 2020 when the pandemic dominated the news and murder hornets were on the way. By Michael J.

Hispanic adults who work with financial professionals were less likely to have postponed retirement than those who are not. In 2020, Hispanic Americans comprised nearly 19% of the overall population, a tremendous rise over the last 50 years. Obstacles to retirementplanning. For Hispanic Heritage Month (Sept. population.

Let’s take a deep look at both plans, and particularly at where each stands out. It’s one of the best strategies to supercharge your retirement savings, especially for early retirement. There's no time like the present to begin preparing for your retirement. of providing tax-free income in retirement.

Stressors between health and wealth When examining the connections between financial and personal wellness, the COVID-19 pandemic in 2020 presents a perfect example of the different ways – physically, mentally, and financially – that people were affected by the virus.

Picture retiring in 2010 versus 2020. The S&P 500 was down 22% for the 10 years ending 1/1/2010 while the ten years ending 1/1/2020 it was up 189%. One fascinating point looked at getting great market returns later in your accumulation period versus earlier. This is in the neighborhood of sequence of return.

The Bottom Line on Checking Your 401(k) A 401(k) is a type of retirement savings plan offered by many employers to their employees. It is a tax-advantaged savings plan that allows employees to set aside money from their paycheck on a pre-tax or after-tax (Roth) basis , into an individual account established in their name.

I expanded on it a little bit and noted it's not particularly relaxing but I would reiterate that this is a great time to lean forward and learn about some things in real time versus looking at a backtest from a benchmark event like the 2020 Pandemic Crash or 2022. All of the different factors have their moments in the sun.

The title of the Man article is Why Alpha Matters for Retirement Savers and in it, they make their case for portable alpha. It also fell 37% in the 2020 Pandemic Crash but it took that back in just four months. Portable alpha combines plain vanilla exposure with alternatives in such a way that leverages up.

A major decision in retirementplanning is whether to make pre-tax or Roth (after-tax) 401k contributions. Pre-tax contributions go into your retirement account with money that has not been taxed, and then taxes will be paid when the funds are withdrawn in retirement.

Barron's wrote about the difficulty of spending down accumulated assets in retirement. You can see that the market started to care about price inflation around the time of the 2020 Pandemic Crash. Starting the clock in March 2020 gives a much different picture. Several quick hits today. XME is a client holding.

Both individual investors and financial professionals are now less optimistic about the next 12 months than they were a year ago, according to the results of our eighth annual Advisor Authority survey, powered by the Nationwide Retirement Institute ®. The value of financial planning. View the infographic.

Starting Out clients are likely to be digitally-fluent, so putting this type of responsibility on them isn’t overly burdensome and can create major efficiencies in your planning processes. Holistic planning will be a valuable way for you to address this broad range of needs.

Over the past several years, retirement investors have had plenty to worry about, from the outbreak of COVID-19 in 2020 to the spread of new coronavirus variants and tenuous trade relations with China in 2021 to the Ukrainian conflict in 2022. Volatility, in turn, often contributes to higher fear and anxiety for retirement investors.

It did decline about 5% in the 2020 Pandemic Crash and in 2022 it was up 1.36%. The backtest runs from the start of 2011 to the end of 2020. Um ok, but MSTR started buying Bitcoin in 2020. The USAF backtest and RAAX don't really look too similar to me. RAAX is much more volatile. In the period studied, CPI compounded at 2.5%

For those employees eligible for Intel’s minimum pension benefit (MPP) at retirement, the interest rate used to calculate today’s value of that benefit is changing. This means that your estimated Minimum Pension Plan benefit amount is significantly reduced or erased altogether in many cases. What should I do next?

In 2014, an 87-year-old, retired specialty-glass importer faced more than $2 million in penalties for failing to disclose a $7 million Swiss account which dated back to the 1960s. military banking facilities; certain bank-to-bank settlements; accounts owned by certain retirementplans. In 2022, a professor with dual U.S.

The post Should Pre-Retirees Take a New Look at #Retirement Income? Should Pre-Retirees Take a New Look at #Retirement Income? By Michael Garry Yardley Wealth Management May 21, 2020. I recently was interviewed for an article in a national publication on retirement income, given the current market and job losses.

Invest in the Stock Market Suggested Allocation: 40% to 50% Risk Level: Varies Investing Goal: Long-term growth The stock market is where most of us save for retirement already, mostly through the use of tax-advantaged retirementplans, like a 401(k), SEP IRA, or Solo 401(k).

The S&P 500 doesn't fall 20% in a quarter very often but obviously it can happen, it happened in Q1 of 2020 and the 3rd quarter of 2008 and I imagine there were others. The next day the fund would have a new buffer 20% down from there. If someone is actually going to use this, it is crucial they sell before the 20% threshold is hit.

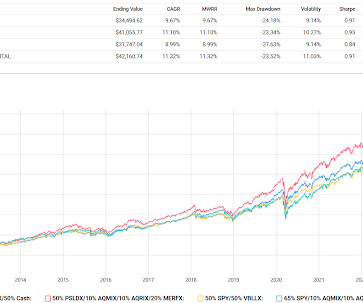

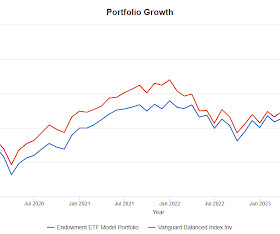

In 2020 and 2023 the fund was unchanged versus up a lot for the other two. To be clear though, the Mystery Fund is not intended to be a single portfolio solution. The year by year tells a slightly different story in case it isn't apparent from the chart.

The "endowment" result is very close to red line VBAIX every year except 2020 when it lagged by almost 600 basis point and 2022 when it outperformed by about 500 basis points. It did worse in the 2020 Pandemic Crash by 200 basis points which isn't problematic for how quickly everything snapped back. Is it this?

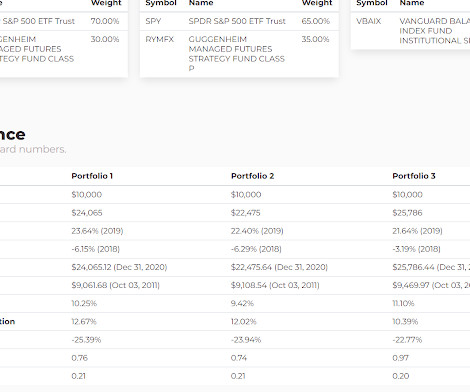

Portfolio 1 lagged by quite a bit in 2019 and then even more in 2020. I took what he was saying to be expressed as follows in a portfolio. And compared to just VBAIX in Portfolio 2 The longer term result is interesting. Then it made it back in 2022 when it was only down 1.1%.

It had a big drawdown in the 2020 Pandemic Crash which, ok, something like that sure but it had a surprisingly big drawdown in 2022 as you can see at 13%. It's growth rate since inception is 3.58% going back to September, 2018 but a lot of that comes from a 15% lift in 2021 (numbers per testfol.io).

Social Security RetirementPlanning . By Michael Garry Yardley Wealth Management October 26, 2020. Around 65 million Americans will receive more than $1 trillion in benefits during 2020, according to the Social Security Administration (SSA). Fleshing out current concerns and common myths.

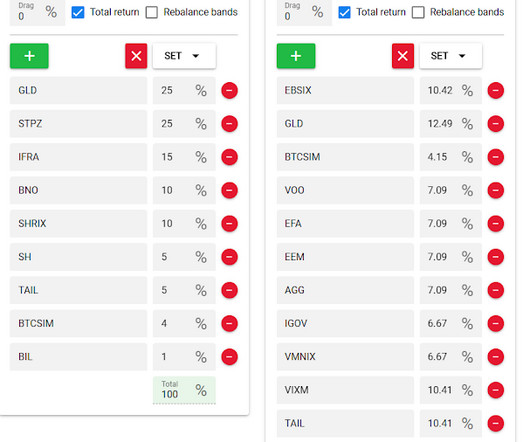

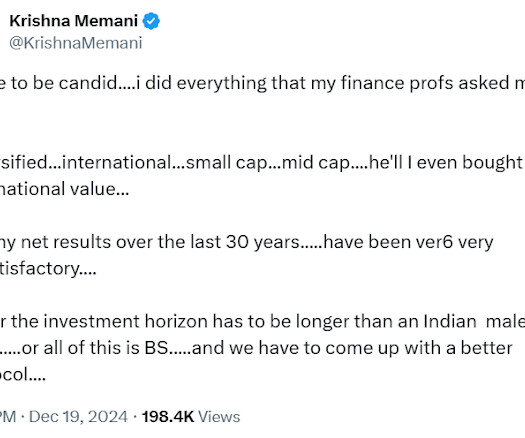

That leads to a Tweet from Krishna Memani who worked at Oppenheimer for a long time and who has been running the Endowment at Lafayette College since 2020. The min vol version is valid longer term but 2020 would have been a challenging time to hold.

Bodie still believes in this, here's a paper he wrote in 2020 , doubling down. He likes TIPS for their volatility profile and because they are real return and he is very concerned about what amounts to sequence of return risk hammering investors as they get close to retirement. Here's a link from me from 2012. years versus 3.13

I saw where this was the worst single day drop since one of the bad days during the 2020 Pandemic Crash. Markets got pasted today of course. Ok, so a quick reminder that bad days have happened before, obvious statement. There have probably been more truly terrible market days than any of us could possible remember.

Forty years ago, the federal government lengthened Social Security’s full retirement age (FRA) from 65 to 67, and increased the delayed retirement credit. Since 1980 through 2014, workers with retirementplans that included a pension fell from 39% to 13%, a 200% decline. Is it the change we want?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content