This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

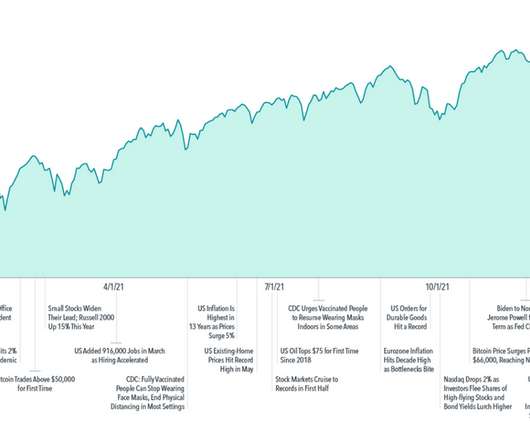

(An investor pondering those questions might take comfort knowing that many assets in the past have outpaced even above-average inflation.). Throughout the year, the market continued a relatively steady rise, with large cap stocks in the US ending 2021 near a record high. The S&P 500 Index1 generated returns of 28.71%.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. In late 2021, markets expected the Fed to largely stay on the sidelines and keep short-term interest rates low.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. Diversification does not protect against market risk.

Retail sales data from the Census Bureau (we focus on the Retail Sales excluding Food Service, Autos, Building Materials, and Gas Stations statistics) has shown year-over-year growth, slow from the average mid-teens numbers seen in 2021, to a still healthy upper-single digits number in 2022 [Figure 2]. over the last 20 years, pre-2020.

For example, the largest S&P 500 ETF had the highest average daily trade volume of US-listed securities in 2021, at $31 billion USD.2 2 It is reasonable to assume a portion of that trading activity represented assetallocation changes motivated by market viewpoints, rather than buy-and-hold position accumulation.

in 2021 and 2.1% The LPL Research Strategic and Tactical AssetAllocation Committee (STAAC) recommends a slight overweight allocation to equities, favors value over growth, small caps over large caps, and the energy, healthcare, and industrials sectors. What Does This Mean for You?

The latest Consumer Price Index (CPI) print decelerated toward the lower end of expectations, with overall headline inflation falling to the lowest level since April 2021. Assetallocation does not ensure a profit or protect against a loss. Insurance products are offered through LPL or its licensed affiliates.

When LPL Research released the Outlook 2022: Passing the Baton in December 2021, the team’s view was that the hit from inflation would be manageable and would therefore limit the number and magnitude of interest rate increases, enable the U.S. Insurance products are offered through LPL or its licensed affiliates.

21, 2021, for a five-year TIPS was -1.685%, a record low. 1 way for retirees to worry less about inflation is to get their assetallocation right. A balanced retirement portfolio should have growth assets and income-producing assets. Insurance-only agents are not licensed to offer investment advice.

We were one of the last to get what’s called a value added license to the compus stat database. And so the institutional space, or most asset selectors, assetallocators are gonna look for managers that are trying to add value. And then in 2021, we actually substantively changed the rules.

The report examined the results of two types of funds7, each holding a mix of stocks and bonds: Balanced: Minimal change in allocation to stocks. Tactical AssetAllocation: Periodic shifts in allocation to stocks. Arnott, “Tactical AssetAllocation: Don’t Try This at Home,” Morningstar, September 20, 2021.

For instance copper, often referred to as Dr. Copper for its ability to forecast economic conditions, just hit its lowest level since February 2021. Insurance products are offered through LPL or its licensed affiliates. Click here to download a PDF of this report. IMPORTANT DISCLOSURES.

MORGENSON: And by 2021, they were extracting 70 billion in dividend recapitalizations. Or should this be kept out of private assetallocators’ hands? Talk to people who try and get licensed to do insurance things, or if there’s a failure to pay out a policy in the litigation that follows. RITHOLTZ: Wow.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content