This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

2021AssetAllocation Perspectives and Outlook. Fri, 02/26/2021 - 13:22. We are pleased to share Brown Advisory’s 2021 Investment Solutions Group (ISG) Annual Outlook report. Valuations seem stretched, and there may be many signs that animal spirits are soaring. Download the full report >.

So what we find, and then of course we have a multi-asset solutions business where we talk to clients about the entirety of their portfolio, their strategic assetallocation models. So you’re Chief Investment officer of Asset and Wealth Management. So we start with a strategic assetallocation.

The recent rally in the market has made the valuations more expensive compared to historical standards. However, heightened valuations do not provide comfort in replicating higher returns of the past in the medium term. Valuations across all sectors do not offer any margin of safety.

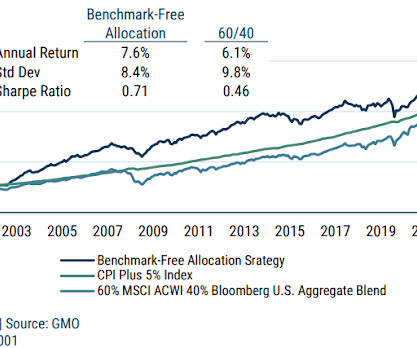

GMO posted a short paper in support of its Benchmark Free AssetAllocation Strategy (BFAAS). For this post we'll focus on BFAAS' assetallocation. The asset mix is 53.6% A more detailed look at the asset mix shows the the following. A more detailed look at the asset mix shows the the following.

Higher valuation of Indian markets compared to Global peers along with negligible earnings growth also didn’t help. One should not be over-allocated to equity (check the 3rd page for assetallocation) at the current levels and any exposure should primarily be towards large cap-oriented value portfolios against growth stocks.

IBM loses to QCOM based on valuation. Sticking back to the balancing theme of quality businesses, great valuations, meshed with the reward of a dividend, you get Ford yielding 4.62% and Conoco only at 2.16% but trading for a bargain P/E of 7. times and return on equity (ROE) of 9%. Why will this massive recovery likely happen?

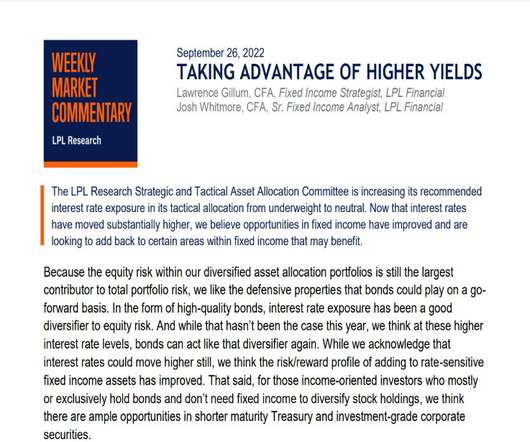

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. In late 2021, markets expected the Fed to largely stay on the sidelines and keep short-term interest rates low.

Some of the fund managers continued discouraging flows in Mid & Small Cap stocks by either sounding cautious, dropping coverage, or stopping the inflows owing to frothy valuations in the space. We maintain our underweight position to equity (check the 3rd page for assetallocation) due to an unfavorable risk-reward ratio.

Sentiment cycles move from one extreme of greed to another extreme of fear which takes valuations also to extremes from their long-term averages. At the extreme of fear sentiment (which coincides with dirt-cheap valuations), the risk-reward is highly favorable i.e., higher potential upside with lower potential downside risk.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. At the same time, the resilience of the U.S.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

Retail sales data from the Census Bureau (we focus on the Retail Sales excluding Food Service, Autos, Building Materials, and Gas Stations statistics) has shown year-over-year growth, slow from the average mid-teens numbers seen in 2021, to a still healthy upper-single digits number in 2022 [Figure 2]. over the last 20 years, pre-2020.

When LPL Research released the Outlook 2022: Passing the Baton in December 2021, the team’s view was that the hit from inflation would be manageable and would therefore limit the number and magnitude of interest rate increases, enable the U.S. economy to avoid recession, and support above-average valuations.

As I pointed out last month, we are coming off a heroic advance over the last three years (2019/2020/2021) with the S&P 500 soaring +90%. Not only are corporate profits at record levels, they are also expected to grow at a healthy rate (+10% in 2022, +10% in 2023) after mind-boggling growth of +50% in 2021 ( see chart below ).

in 2021 and 2.1% Higher interest rates are challenging stock valuations and perhaps pushing the gains further out in 2023, but we still see solid potential for double-digit returns for stocks this year. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. It pushes valuations higher over time. 00:04:02 That’s what value add software was originally.

The latest Consumer Price Index (CPI) print decelerated toward the lower end of expectations, with overall headline inflation falling to the lowest level since April 2021. Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. All index data from FactSet.

ajackson Mon, 10/11/2021 - 11:55 Endowment and Foundation (E&F) Investment Committees often consider the value of alternatives for their nonprofit. We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. Source: BLOOMBERG.

Mon, 10/11/2021 - 11:55. We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming.

EOG is poised to breakout and trades at bargain valuation of about nine times earnings (relative to the S&P at 23 times earnings and a touch under the overall energy sector of 12 times earnings). That said, it loses early in round one simply due to us believing it’s close to full valuation and due for a breather.

T he stock market has been like a rocket ship over the last three years 2019/2020/2021, advancing +90% as measured by the S&P 500 index, and +136% for the NASDAQ. After this meteoric multi-year rise, stock values started to come back to earth in 2022, and the rocket ship turned into a roller coaster during January.

So there’s been a big push for folks to get the appropriate level of assetallocation in a highly diversified, low cost way. But if you go back to the period before 2022, from 2019 to 2021, a 60/40 portfolio actually produced 14% returns over that time horizon, which is above the long-term average. RITHOLTZ: Right.

After a tough decade for simple systematic value strategies from 2011-2021 this model bounced back very well in 2022. Throughout 2022 the most expensive stocks were the ones hit hardest as valuations started to normalize in a new world of higher interest rates. Mohanram called this the “G-Score”. and -6.1%, respectively.

The DJIA did reach 35,000 in June 2021, but Dent had long been a permabear by then. In March 2021, Dent called for a nearly 50 percent drop in the S&P 500 by June. In July 2021, he followed up with a prediction that equities would drop by 80 percent in the fall, which didn’t happen, either. percent in 2021.

The positive global perception and growing domestic inflows ensure that the premium valuations of the Indian market are maintained. Some of the institutions dropped coverage or discouraged investing in Mid & Small Cap stocks owing to very expensive valuations boosted primarily by retail participation lured by past returns.

He launched his own firm right into the teeth of the collapse in ’09, which turned out to be quite a fortuitous time to launch an asset management shop. Everybody wants to sell a company when they get a good valuation. But I think, you know, for us, 2021, in general, towards the end of the year got very hard, right?

They’re assetallocation model driven folks. And we’ve automated the, the appraisal process for valuation, both intrinsic value, meaning like, where would we pay it, where would we buy it, and where is the fair market price that asset from that level, from price and from consumer behavior now.

And one of the worst performing factors has been valuation. So we’re now in an environment where all the 45-year-old portfolio managers out there have been, have worked their entire careers in these momentum fueled markets, and they’ve been trained to believe that valuation doesn’t matter. I think that’s right.

Barry Ritholtz : So we’re talking about corporate culture November, 2020, you’re elevated from president to CEOI recall lots and lots of CEOs talking about in 2020 and 2021, right in the midst of the Covid pandemic, Hey, how are we gonna maintain a form of corporate culture? How do we keep everybody on the same page?

While we acknowledge that a V-shaped recovery is probably not in the cards and prior valuation targets no longer appear achievable, we remain constructive on equities for the second half, but not complacent. Remember stock valuations are inversely correlated to inflation and interest rates. So a P/E over 20 is probably too rich.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content