This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Not if you spend tax season on a boat! I doubt he’s run the real numbers of being invested in the stock market tax deferred with an additional company match. There is lots more: A slew of bad tax advice likely to get-you-sent-to-jail-for-tax evasion: Live on a boat during tax season! Want to earn more money?

“I need the US Dollar to be a store of value between the time I make it until I spend it, invest it, pay my taxes with it, or give it away. To be more precise, I want to discuss the type of chart that reflects a fundamental misunderstanding of the nature of money, currency, spending, investing, and taxes. and paying taxes.

Sorry, but “fake it till you make it” seems like a poor plan for thinking about the future… Previously : Time to Stop Believing Deficit B t (September 3, 2021) Stimulus, More Stimulus and Taxes (January 25, 2021) Cost of Financing US Deficits Falls (December 18, 2020) Can We Please Have an Honest Debate About Tax Policy?

Your grandchildren will blame the toxic combination of incompetency and ideology for the massively increased carrying costs of unfunded spending and tax cuts. Note that we undertook much of the work anyway (airports, electrical grid, roads, etc.), just decades later at a much greater cost. All simply unnecessary.

The article devoted a good amount of space to bond market math, focusing on the pain of owning the iShares 20+ Year Treasury ETF (TLT) and bond funds in general. It turned out it did matter starting in late 2021. Bond funds have no par value to return to which might make them worse than individual bonds.

We've talked just a couple of times about the market becoming increasingly concentrated which just in terms of math means that a diversified strategy will lag for as long as the big names do well. Outperformed long term but down a sickening 43% and still down about 25% from its late 2021 highwater mark.

Interest rates have skyrocketed since the end of 2021. Again just using simple math, this presumes the par value will roll over each month and reinvest at the same rate to get to the annual yield. If the funds aren’t earmarked for anything in the near term, holding cash could be short-sighted. Hold cash or invest? 467% a month.

That's pretty much what happened starting at the very end of 2021. It is important to understand the math though. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. I think managed futures are pretty good at this as just one example.

What I took from it was that the safe withdrawal rate in 2021 was 3.3%, last year it was 3.8% Part of the math that determines options premiums is the risk free rate of return from T-bills. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. People earn wages, whether it’s a retirement account or a tax deferred account or just an investment account.

So how do you then go from tax and audit practice to finance and investing? So I took it upon myself to go off and took a course in bond math, took another course in derivatives and realized the underlying fundamental concepts were barely, I mean, it wasn’t even high school math in most cases. Very different fields.

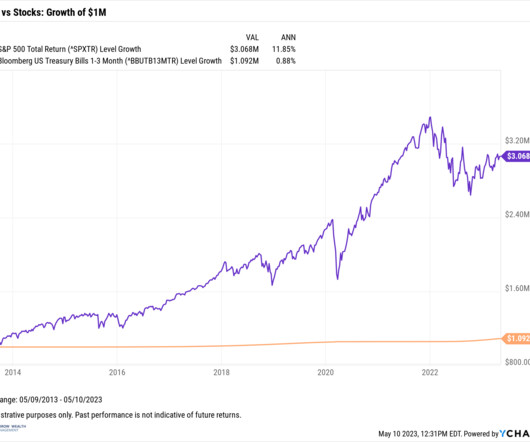

T he stock market has been like a rocket ship over the last three years 2019/2020/2021, advancing +90% as measured by the S&P 500 index, and +136% for the NASDAQ. Math Matters. I did okay in school and was educated on many different topics, including the basic principle that math matters. Source: Calafia Beach Pundit.

If you dig even deeper, you may also think about tax implications, including the alternative minimum tax and qualified holding periods. But the basics of equity compensation and tax aside, theres something else you might want to be mindful of something that is a bit more difficult to define or quantify.

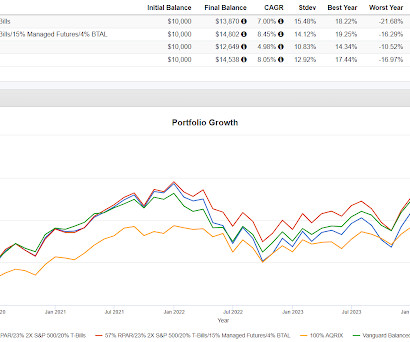

If we stop that backtest at the end of 2021, the two levered portfolios outperformed by five and four basis points respectively, each with noticeably higher standard deviations and lower Sharpe Ratios. A 20% drop in managed futures that is leveraged to a 40% weight would have added another 800 basis points to the decline (simple math).

I — I loved math, but really, I was going to go down that literature route more than anything else and — and study Spanish literature. there’s a big focus on how do we optimize for tax efficiency, too. It’s different wealth regimes, it’s different tax regimes. RITHOLTZ: Applied Mathematics, Quants, those guys, yeah.

One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics. So people really ask you, you take French and can you do math. Two reasons. There was a good equity rebound.

The math is only off by a shade using leverage via UST and a little bit of SSO, remember RPAR is leveraged. In 2020, RPAR did much better than the replication, did a little worse in 2021, 2023 and 2024 YTD and in 2022 RPAR lagged the replication by 11%. The Replication is based on this from RPAR.

So I, I did a math degree at Oxford, which is more pure math. You know, pure math can be very theoretical and detached from the real world, and it’s getting worse. You don’t have to pay any tax and just let the rest ride. It’s just math stick to it over long periods of time. You give out 5%.

You have the liquidity, the tax efficiency, the transparency. And I did the math, and I think at that point in time, roughly speaking, assets in ETS were roughly just 10 percent, 12 percent of assets in mutual funds and I was pretty convinced that that number was to increase significantly. We had really good 2021 in terms of inflows.

Also being cognizant of the tax implications of trading activity. They like tax-free income, but they also don’t like principal losses. But if you go back to the period before 2022, from 2019 to 2021, a 60/40 portfolio actually produced 14% returns over that time horizon, which is above the long-term average.

So for a taxable investor, hedge funds generally aren’t tax efficient. And when you look at the assets that are invested, the three trillion in hedge funds, I would guess that north of 90% of that are in institutions that don’t pay taxes. It’s part of their own tax planning. I like Buffett’s idea.

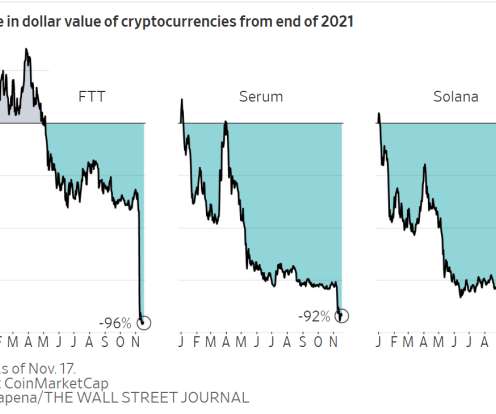

After a stint in Hong Kong, Mr. Bankman-Fried and FTX made their home in the Bahamas, moving in 2021 to take advantage of the island country’s crypto-friendly regulatory regime. The owner got to know Mr. Bankman-Fried’s father, Stanford tax-law scholar Joseph Bankman, during his visits to Nassau to spend time with his son.

Institute for New Economic Thinking ) Insurance and Taxes Now Cost More Than Mortgages for Many Homeowners : Ballooning expenses rewrite the math of homeownership. This December, Ohanian retracted his claim; Hoover retracted 8 additional Ohanian claims.

My mom was a math teacher so — RITHOLTZ: Okay. You can argue they’re — RITHOLTZ: A more tax efficient than that? ASNESS: More tax efficient dividend. And by the way, I don’t take a great stance on how they should be taxed. He’s the genius in math. That’s a separate issue.

That includes all of its changes in its property taxes, it’s, it’s depreciable life for the improvements of the assets. Well, I think that same thing’s been happening in commercial now for the last, you know, since 2021 is that physical occupancy is the leading indicator to economic occupancy. Sometimes five years.

Michael Lewis ] 00:01:42 So this friend reaches out in September of 2021, and I’d never heard of Sam Bankman Fried or F T X , I hadn’t been paying much attention to crypto. Because he was all sure he was a totally isolated math. So, so he’s brilliant at math. He goes to m i t to study, study physics and math.

The way Portfolios 1 and 2 are weighted, the math works for being a 60/40 portfolio and then from there we add portable alpha/capital efficiency/return stacking. In late 2021, when things were going well in markets, they brought up whether they should start to give out a higher percentage every year. I'm a research volunteer.

I’m kind of in intrigued by the idea of philosophy and math. So I found myself getting kind of bored with my math problem sets, and then I could shift to philosophy and then go back and forth. It’s all tax free. In not paying your taxes. So ba in mathematics and philosophy from Berkeley, an MBA from Columbia.

Burger King Tim Hortons, I remember very clearly because it was in the middle of those waves of kind of tax dodgy, those inversion deals. I mean, you’re talking about, I don’t, I could do the math, it’s like a 10,000% return in like three weeks. And that’s sort of the math. RITHOLTZ: Right.

So here’s the math, Barry. If you start with a thousand and you only have an addition of $750 a year, okay, families can contribute to that, your 00:44:48 [Speaker Changed] Corporate tax free. You take it out tax free as well. You cannot anchor yourself to some delusional price you got in 2020 or 2021. Completely.

MORGENSON: And by 2021, they were extracting 70 billion in dividend recapitalizations. And it really became very evident in a 2021 study by academics, I think University of Chicago, UPenn, NYU, that studied long-term mortality at nursing homes that were owned by private equity and compared that with nursing homes. RITHOLTZ: Wow.

Literally the first check-in to Robinhood, which went public in 2021 at about a $34 billion valuation. I wrote a, a column in 2021 for Bloomberg, “What My Worst Trades Taught Me About Investing.: So this is the math that I applied. So think about this, do the math. LINDZON: They have their own tax problems.

So, I did the math, 20 million times a hundred. So, let me just repeat the math. And so, again, I went through this simple math. And they said as a result of them earning zero, the $230 million of taxes that was paid in the previous year is paid in error and we’d like that money back. It is $2 billion on the ship.

You sit in a room all day doing tax returns or something, it’s just not, you know, that it seemed antisocial. Wasn’t the Excel spreadsheet error, which changed their math. A massive buildup in military, you know, couple of huge tax cuts deficits were increasing, the debt was increasing very rapidly. I mean Yep.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content