This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

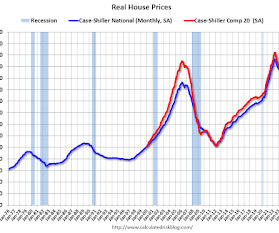

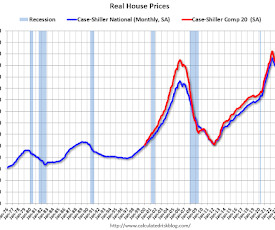

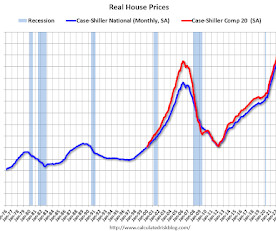

Below 2022 Peak Excerpt: It has been over 18 years since the housing bubble peak. below the recent peak in 2022. Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 1.1% The second graph shows the same two indexes in real terms (adjusted for inflation using CPI).

Below 2022 Peak Excerpt: It has been over 18 years since the housing bubble peak. below the recent peak in 2022. Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 0.8% The second graph shows the same two indexes in real terms (adjusted for inflation using CPI).

Below 2022 Peak Excerpt: It has been over 18 years since the housing bubble peak. below the recent peak in 2022. Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 1.0% The second graph shows the same two indexes in real terms (adjusted for inflation using CPI).

Earliler the Census Bureau released the population estimates for July 2022 by age, and I've updated the table from the previous post. The table below shows the top 10 cohorts by size for 2010, 2022 (released recently), and the most recent Census Bureau projections for 2030. population by age in July 2022 according to the Census Bureau.

It’s never been easier for companies to recruit top-tier talent on a global scale, thanks to remote working apps, platforms, and social media. However, employees are now embracing lifestyle over work – with many migrating to other jobs to find new opportunities that better align with their values and priorities.

Below 2022 Peak Excerpt: It has been 18 years since the bubble peak. below the recent peak in 2022. Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 1.9% The second graph shows the same two indexes in real terms (adjusted for inflation using CPI). In real terms (using CPI), the National index is 1.9%

The FDIC released the Quarterly Banking Profile for Q4 2022: Reports from 4,706 commercial banks and savings institutions insured by the Federal Deposit Insurance Corporation (FDIC) reflect aggregate net income of $68.4 billion in fourth quarter 2022, a decrease of $3.3 billion (4.6 percent) from the third quarter.

Below 2022 Peak Excerpt: It has been over 18 years since the bubble peak. below the recent peak in 2022. Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 1.5% The second graph shows the same two indexes in real terms (adjusted for inflation using CPI). Both indexes increased in July in real terms.

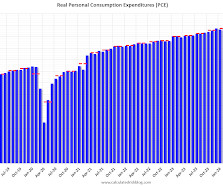

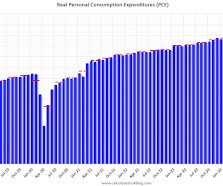

percent in June 2022. percent in February 2022. Real DPI increased 0.4 percent and real PCE increased 0.1 percent; goods increased less than 0.1 percent and services increased 0.2 emphasis added The October PCE price index increased 2.3 percent year-over-year (YoY), up from 2.1 percent YoY, up from 2.7

The fintech industry is growing exponentially — in the first quarter of 2022, the sector saw a 182 percent increase in tech job growth. However, experts are warning that local candidates to fill those roles may become scarce in certain areas.

million in 2022, and 7.3 million in 2021 (2021 and 2022 were the two best years ever), but still a solid year for employment gains. in early 2022. 10) Housing Inventory: Housing inventory decreased sharply during the pandemic to record lows in early 2022. Will there be a recession in 2025? million jobs in 2024.

Firm billings have now decreased for the majority of firms every month except two since October 2022. In November, we saw the first positive score for multi-family since 2022. From the AIA: ABI December 2024: Business conditions end the year on a weak note The AIA/Deltek Architecture Billings Index (ABI) score fell to 44.1

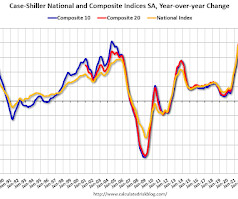

Below 2022 Peak • Freddie Mac House Price Index Increased in September; Up 3.6% . • Case-Shiller: National House Price Index Up 4.2% year-over-year in August • Fannie and Freddie: Single Family and Multi-Family Serious Delinquency Rates Increased in September • Inflation Adjusted House Prices 1.5%

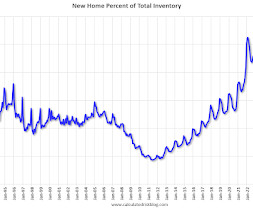

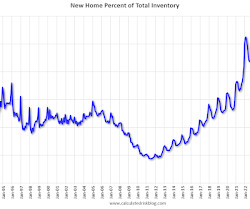

in December 2022. The following graph uses Not Seasonally Adjusted (NSA) existing home inventory from the National Association of Realtors (NAR) and new home inventory from the Census Bureau (only completed and under construction inventory). Then, with the pandemic, existing home inventory collapsed and now the percent of new homes is 22.4%

As we move through 2022, companies are eager to retain a competitive advantage and continue on the path of success and adaptability. Preparing for the unexpected and pivoting at a moment’s notice were valuable lessons many global companies learned in 2020 and 2021.

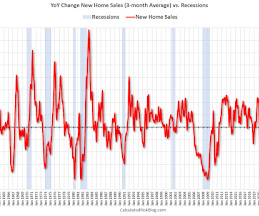

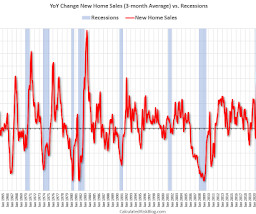

In 2022, both new home sales and single-family starts turned down in response to higher mortgage rates. The YoY change in new home sales in late 2022 and early 2023 suggested a possible recession. New home sales peaked in 2020 as pandemic buying soared.

percent in June 2022. percent in February 2022. Excluding food and energy, the PCE price index increased 2.8 percent from one year ago. emphasis added The February PCE price index increased 2.5 percent year-over-year (YoY) , unchanged from 2.5 percent YoY in January, and down from the recent peak of 7.2 percent YoY , up from 2.7

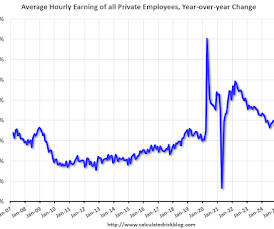

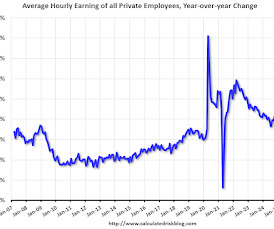

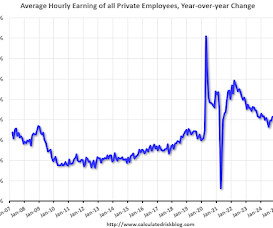

YoY in March 2022 and was at 3.9% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.6%). There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later. Wage growth has trended down after peaking at 5.9%

In 2022, both new home sales and single-family starts turned down in response to higher mortgage rates. The YoY change in new home sales in late 2022 and early 2023 suggested a possible recession. I dismissed it when the yield curve inverted in 2019 and again in 2022. New home sales peaked in 2020 as pandemic buying soared.

Speaker: Marguerita Cheng - Chief Executive Officer at Blue Ocean Global Wealth

November 2nd, 2022 at 9:30 am PT, 12:30 pm ET, 5:30 pm BST Personal finance apps vs. professional money management. How FinTech is changing the industry. The importance of fostering inclusion and belonging in money management.

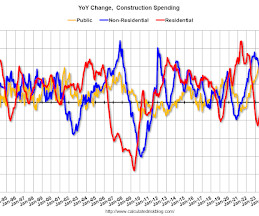

below the peak in 2022. This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted. Private residential (red) spending is 4.2% Private non-residential (blue) spending is at a new peak. Public construction spending is 0.6%

YoY in March 2022 and was at 3.8% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.6%). There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later. Wage growth has trended down after peaking at 5.9%

in June 2023 from June 2022 , their first decline in three months. million) were up 0.6% (32,547( carloads) over the same period in 2022 and were the highest since 2019. decline from June 2022 was their 16th straight. Carloads in 2021, 2022 and 2022: Total originated carloads (which don’t include intermodal) on U.S.

below the peak in 2022. This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted. Private residential (red) spending is 5.3% Private non-residential (blue) spending is at a new peak. Public construction spending (orange) is at a new peak.

Speaker: Nancy Wu, Head of Sales and Customer Success at SkyStem

May 18, 2022 at 1pm EST Prerequisite: None. Advanced Preparation: None Required. Delivery Method: Group Internet-Based. Feedback and Comments: contact marketing@skystem.com or call 646-833-3177.

in December 2022. It took a number of years following the housing bust for new home inventory to return to the pre-bubble percent of total inventory. Then, with the pandemic, existing home inventory collapsed and now the percent of new homes is 25.1% of the total for sale inventory, down from a peak of 27.2%

percent in June 2022. percent in February 2022. Personal saving was $843.2 billion in December and the personal saving ratepersonal saving as a percentage of disposable personal incomewas 3.8 emphasis added The December PCE price index increased 2.6 percent year-over-year (YoY), up from 2.4 percent YoY, unchanged from 2.8

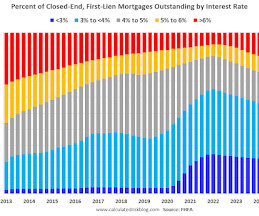

The percent of outstanding loans under 4% peaked in Q1 2022 at 65.1% (now at 54.1%), and the percent under 5% peaked at 85.6% (now at 72.1%). This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic.

I stopped the weekly updates of high frequency indicators at the end of 2022. This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue), 2022 (Orange) and 2023 (Red). Black is 2020, Blue is 2021 and Red is 2022. This data is as of June 25th.

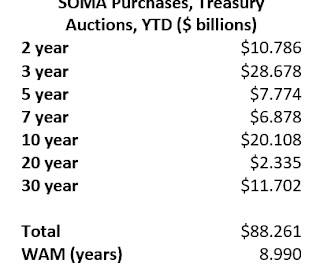

From housing economist Tom Lawler: From the beginning of 2020 to early June of 2022 the Federal Reserves balance sheet more than doubled to an almost inconceivable $8.9 Below is a comparable table for the end of 2022. trillion, with most of the decline reflecting decreases in Treasury and Agency MBS holdings.

billion, and an average loss of $5,400 per borrower since the first quarter of 2022. As in the fourth quarter of 2022, Western states posted the largest annual home equity losses: Washington (-$74,300), California (-$59,600) and Utah (-$37,700). The report shows that U.S. year over year, representing a collective loss of $108.4

in August, unchanged since early 2022. in August 2022. in August 2022. in August 2022 and a high of 4.3% Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, unchanged from August 2022. in August, also a historic low. • foreclosure rate held steady at 0.3%

HELOC balances increased by $7 billion, representing the tenth consecutive quarterly increase since Q1 2022, and stood at $387 billion. Mortgage balances increased by $75 billion from the previous quarter and reached $12.59 trillion at the end of September. Credit card balances increased by $24 billion to $1.17

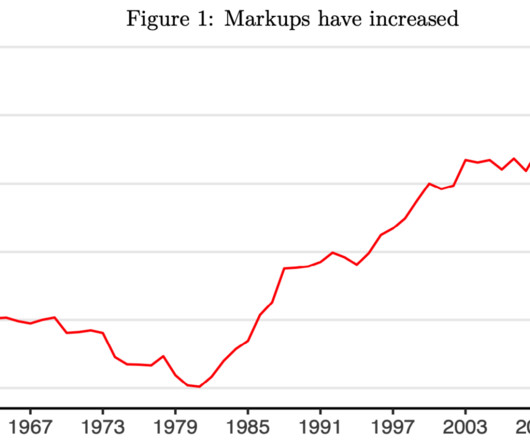

”1 I was pretty skeptical about Greedflation initially; when i ranked the top 15 sources of US inflation in mid-2022 , “ Corporate Profit Seeking ” was at the bottom, ranked 13 out of 15 inflation causes. In August 2022, Vox suggested that if you were mad about inflation you should blame your local officials.

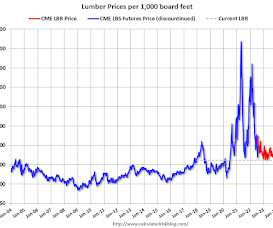

I switched to a physically-delivered Lumber Futures contract that was started in August 2022. This graph shows CME random length framing futures through last August (blue), and the new physically-delivered Lumber Futures (LBR) contract starting in August 2022 (Red). LBR is currently at $446.00 Click on graph for larger image.

I stopped the weekly updates of high frequency indicators at the end of 2022. This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue), 2022 (Orange) and 2023 (Red). Black is 2020, Blue is 2021 and Red is 2022. compared to the same week in 2022.

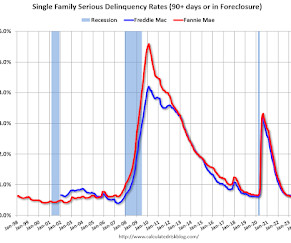

Freddie's rate is down year-over-year from 0.99% in February 2022. Note that multi-family delinquencies have been increasing and were at 0.13% in February, up from 0.08% in February 2022. Freddie Mac reported that the Single-Family serious delinquency rate in February was 0.65%, down from 0.66% January. Fannie Mae reported earlier.

million units, 18% above like-2022, and stronger than Q1’s 8% gain. million units, up 13% from January-June 2022’s 6.78 Light-Vehicle Sales Pegged for 21% Gain; Q2 to Roll in at 2-Year-High 15.7 Million SAAR (pay content). Brief excerpt: Deliveries in the second quarter will total 4.1 First-half 2023 volume will total 7.67

I've now switched to a new physically-delivered Lumber Futures contract that was started in August 2022. This graph shows CME random length framing futures through May 16th (blue), and the new physically-delivered Lumber Futures (LBR) contract starting in August 2022 (Red). Unfortunately, this impacts long term price comparisons.

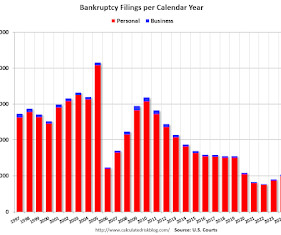

million in September 2010 to a low of 380,634 in June 2022. Bankruptcy totals for the previous 12 months are reported four times annually. For more than a decade, total filings fell steadily, from a high of nearly 1.6 Total filings have increased each quarter since then, but they remain far lower than historical highs.

Freddie's rate is down year-over-year from 0.92% in March 2022. Note that multi-family delinquencies have been increasing and were at 0.13% in March, up from 0.08% in March 2022. Freddie Mac reported that the Single-Family serious delinquency rate in March was 0.62%, down from 0.65% February.

YoY in March 2022 and was at 4.1% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.6%). There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later. Wage growth has trended down after peaking at 5.9%

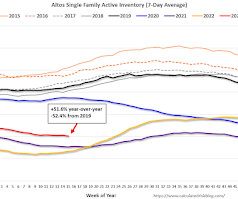

Note that inventory is up from the previous two years (the record low was in 2022), but still well below normal levels. compared to the same week in 2022 (last week it was up 59.1%), and down 52.4% The red line is for 2023. The black line is for 2019. Inventory was up 51.6% compared to the same week in 2019 (last week down 50.9%).

Note that inventory is up from the previous two years (the record low was in 2022), but still well below normal levels. compared to the same week in 2022 (last week it was up 18.4%), and down 52.4% The red line is for 2023. The black line is for 2019. Inventory was up 12.8% compared to the same week in 2019 (last week down 53.7%).

363

363

Input your email to sign up, or if you already have an account, log in here!

Enter your email address to reset your password. A temporary password will be e‑mailed to you.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content