This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

bloomberg.com) NEA is becoming a registered investmentadvisor. pionline.com) Economy Q4 2022 GDP was solid, but two leading indicators point toward recession. (wsj.com) Startups Stripe is set to go public in the next twelve months. wsj.com) Startups are pulling out all the stops to avoid down-rounds.

We may not be flying into a storm, but there’s been plenty of turbulence the first part of 2022. How businesses, households, and central banks steer through the rough air will set the tone for markets over the second half of 2022. The sources of turbulence are clear.

Undaunted by another Fed rate hike and news of a contracting economy, the stock market rallied last week on better-than-expected corporate earnings. Powell indicated that it might become appropriate to slow the pace of future hikes, and he didn’t believe the economy had entered into recession. Economy Contracts . Factory Orders.

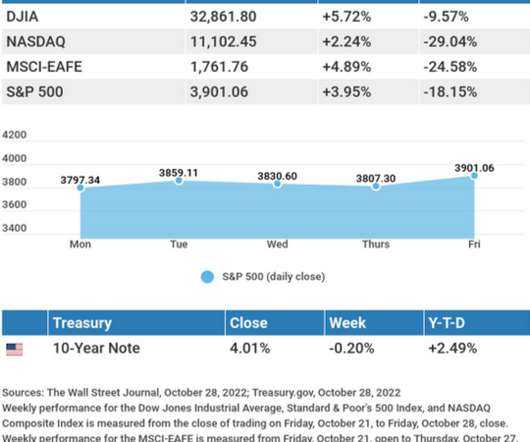

Meanwhile, positive earnings surprises from “old economy” companies powered markets higher. Source: Econoday, October 28, 2022 The Econoday economic calendar lists upcoming U.S. Source: Zacks, October 28, 2022 Companies mentioned are for informational purposes only. The Wall Street Journal, October 28, 2022.

Perhaps the market’s biggest fear has been that the Fed may overdo its tightening to fight inflation and send the economy into a painful recession, break something, or both. He acknowledged that the economy is slowing (which is what the Fed wants) and that the full effect of the rate hikes had not yet been felt. Of course, the U.S.

At this rate, home sales will likely continue to slow and residential investment could turn out to be a drag on Q3 economic growth. Given the lag between Federal Reserve (Fed) policy and the real economy, we have not likely seen the bottom in the housing market. Regional differences are profound. Conclusion.

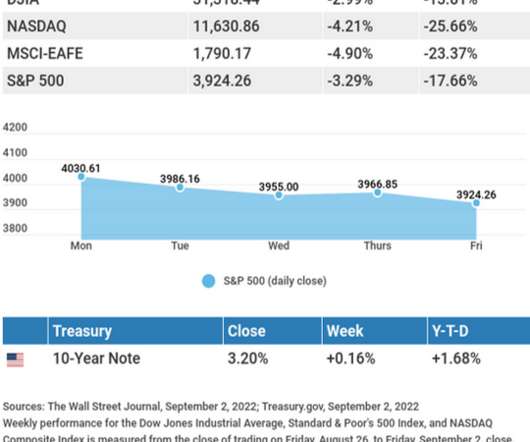

Employers added 315,000 jobs in August, maintaining the labor market’s remarkable resiliency amid a contracting economy. Source: Econoday, September 2, 2022 The Econoday economic calendar lists upcoming U.S. Source: Zacks, September 2, 2022 Companies mentioned are for informational purposes only. CNBC, September 2, 2022.

How businesses, households, and central banks steer through the rough air will set the tone for markets over the second half of 2022. Securities and advisory services offered through LPL Financial (LPL), a registered investmentadvisor and broker-dealer (member FINRA/SIPC). The sources of turbulence are clear.

Whether it’s about the markets and global economy or what’s happening in our local communities, the news we’re hearing on a daily basis has the potential to disrupt the balance of our lives. Even after another dizzying year, as 2022 proved to be. All index data from FactSet.

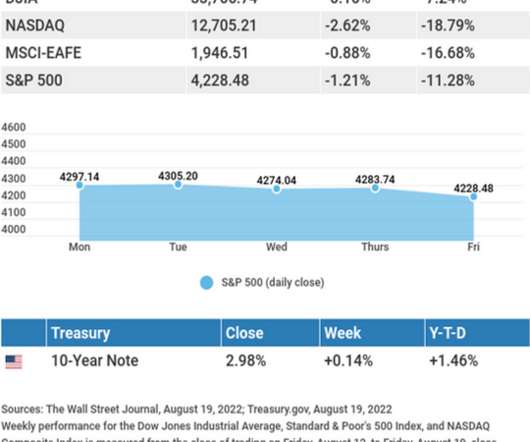

Fed officials did acknowledge that further rate hikes risked unintended economic weakness because of the time it takes for higher rates to work through the economy. Source: Econoday, August 19, 2022 The Econoday economic calendar lists upcoming U.S. Source: Zacks, August 19, 2022 Companies mentioned are for informational purposes only.

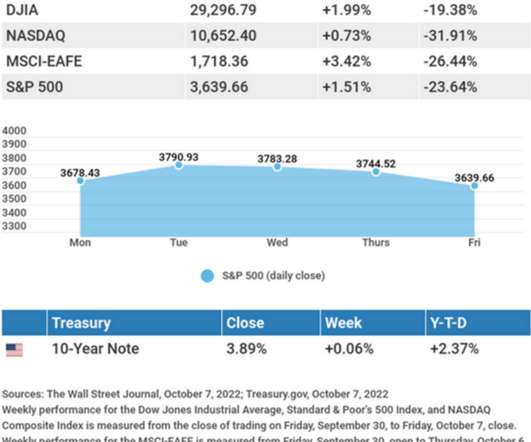

Falling yields further lifted investor enthusiasm, as did new economic data indicating a cooling economy. Source: Econoday, October 7, 2022. Source: Zacks, October 7, 2022. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. Jobless Claims.

He cited several areas of progress in the inflation fight, including a deceleration in interest rate sensitive parts of the economy, such as housing and supply chain improvement. Source: Econoday, December 2, 2022 The Econoday economic calendar lists upcoming U.S. The Wall Street Journal, December 2, 2022. Consumer Sentiment.

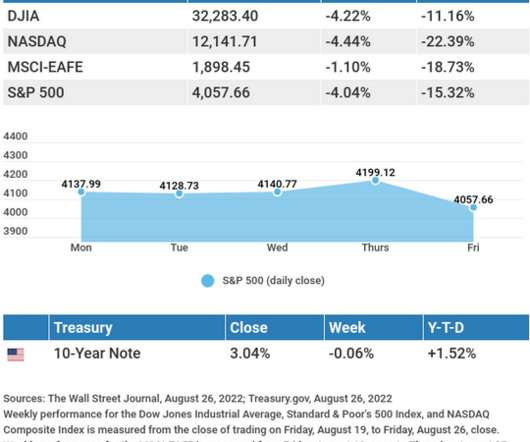

Stocks rallied on Thursday, sparked by a revised Gross Domestic Product estimate showing the economy’s shrinking less than initially estimated. Source: Econoday, August 26, 2022 The Econoday economic calendar lists upcoming U.S. Source: Zacks, August 26, 2022 Companies mentioned are for informational purposes only.

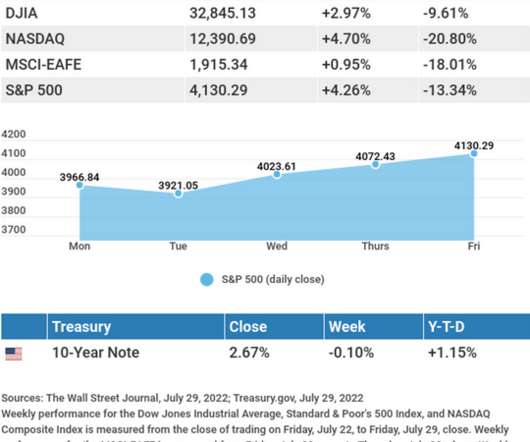

As the week progressed, stocks gained momentum as earnings results poured in from different sectors of the economy, showing that businesses were navigating higher inflation and slowing growth better than investors feared. Source: Econoday, July 22, 2022. Source: Zacks, July 22, 2022. The Wall Street Journal, July 22, 2022.

Dear Valued Investor, As the calendar has turned to July, investors would certainly like to forget the first six months of 2022. economy remain relatively strong. real GDP growth to be around 2% in 2022. This may come to pass, especially if a recession can be averted in 2022 as we expect. Should the U.S.

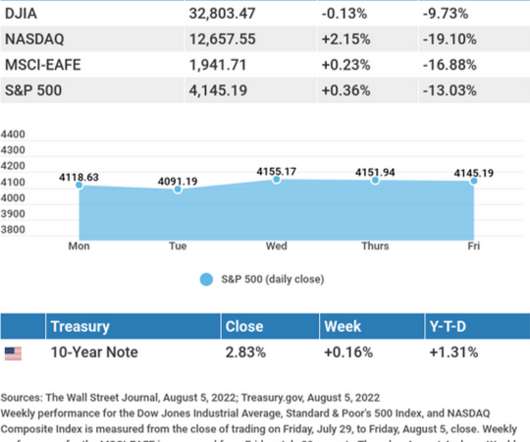

economy added 528,000 jobs in July, doubling the consensus expectation of 258,000. Leisure and hospitality, professional and business services, and healthcare lead the way in reported job gains, as seen in most sectors of the economy. Source: Econoday, August 5, 2022 The Econoday economic calendar lists upcoming U.S.

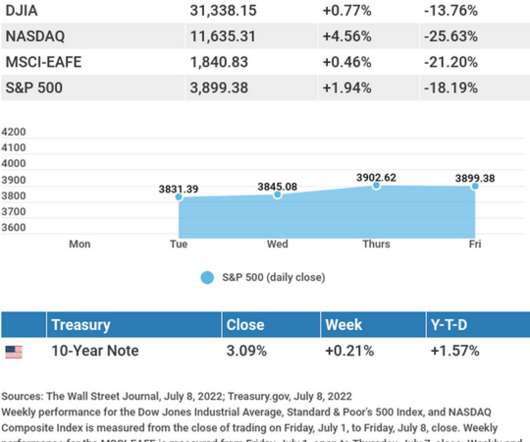

Recession fears were supported by an inversion in the yield curve and updated second-quarter Gross Domestic Product projections indicating the economy is ready to contract. Source: Econoday, July 8, 2022 The Econoday economic calendar lists upcoming U.S. The Wall Street Journal, July 8, 2022. CNBC, July 8, 2022.

Dear Valued Investor, In the last several weeks, we have continued to face elevated uncertainty in financial markets due to high inflation and rising interest rates, and we thought it was an important time to take stock with the final quarter of 2022 just ahead. But this is not your 1970s- style stagflation. in August of this year.

economy contracted for the second straight quarter. With a strong, even if slowing, job market and resilient consumer spending, we believe not enough sectors of the economy are contracting to qualify as an official recession. Given the slowing economy, intense cost pressures, and a strong U.S. All index data from FactSet.

Investors were approaching the new earnings season with a fair amount of trepidation amid an environment of higher interest rates and a slowing economy. Source: Econoday, October 21, 2022. Source: Zacks, October 21, 2022. The due dates as of 2022 are April 30 for Q1, July 31 for Q2, October 31 for Q3, and January 31 for Q4.

The key to getting the market back into balance is a bigger labor force, and the economy is starting to experience a larger labor force as individuals come off the sidelines and rejoin the job market. The global economy is complex, and a simplification of reality always introduces distortions, so perhaps we should zoom out a bit.

economy is in or about to enter recession, so we thought a piece on what a recession might mean for the stock market would be of interest. economy is not currently in recession, odds are still perhaps a coin flip or better that one may come in the next year. While Friday’s strong jobs report provides more evidence that the U.S.

economy following disappointing August inflation data was the top cause of the market’s struggles. in September, temporarily breaking below the June 2022 closing low. Securities and advisory services offered through LPL Financial (LPL), a registered investmentadvisor and broker/dealer (member FINRA/SIPC).

Given the country’s weak economy, due in large part to stringent zero-COVID-19 measures that have led to strict and prolonged lockdowns, coupled with a debt-laden property market, authorities in Beijing and throughout the Chinese provinces will need to focus on reviving the country’s economic underpinning. At the same time, U.S.

economy enters a recession, the causes and potential outcome will be hotly debated. Diffusion describes an economy that has experienced a contraction in a wide range of sectors, such as trade, business activity, and consumer spending. Pockets of Vulnerability Magnified by Monetary Policy – October 10, 2022. If the U.S.

If an economy needs to see inflation easing, it makes little sense to stimulate the economy through tax cuts while tightening monetary policy by raising interest rates. Powell has repeated, in what has become his mantra, that without price stability we cannot have a strong economy or a strong labor market. IMPORTANT DISCLOSURES.

With a series of important economic indicators suggesting the economy is declining and inflation is finally decelerating, albeit very slowly, markets are beginning to factor in that the Fed may soon transition to a less aggressive stance in early 2023. The Economy Slows But Inflation Follows Too Slowly. economy grew at a 2.6%

Here are some of our lessons learned from 2022. One of the lessons learned in 2022 was to never underestimate our central bank’s resolve to squelch inflation. At the start of 2022, markets expected the upper bound of the fed funds rate to stay below 1%. economy to avoid recession, and support above-average valuations.

The growth vs. value debate has been pretty one-sided in 2022, with value outperforming growth for a sustained period for the first time in almost 15 years. Value vs. Growth – Value Takes 2022. You may also be interested in: How Midterm Elections May Move Markets – November 7, 2022. IMPORTANT DISCLOSURES.

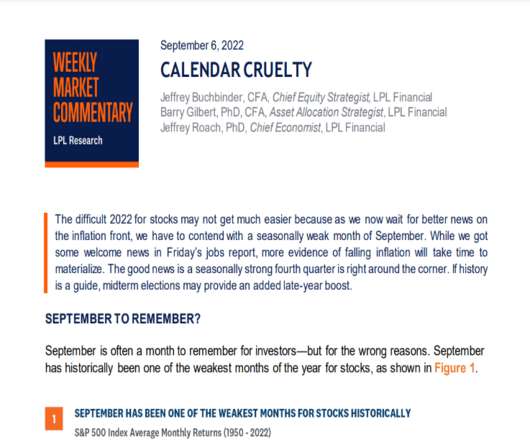

The difficult 2022 for stocks may not get much easier because as we now wait for better news on the inflation front, we have to contend with a seasonally weak month of September. The economy is now employing more workers in temporary help services than ever before, and this could be a cause for concern. What’s Next? – August 22, 2022.

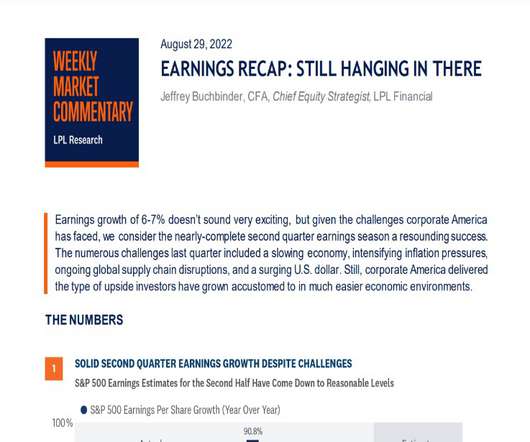

The numerous challenges last quarter included a slowing economy, intensifying inflation pressures, ongoing global supply chain disruptions, and a surging U.S. Estimated profit margins for the second half of 2022 did indeed come down as companies reported, but not dramatically so. annualized according to the Atlanta Federal Reserve.

The market rebound and overall bullish sentiment began in earnest when Federal Reserve (Fed) Chairman Jerome Powell suggested at the late July Fed meeting that the trajectory of interest rate hikes could ease later in 2022. Stocks climbed dramatically, and the S&P 500 Index recorded its largest post meeting rally ever recorded.

Retail sales data from the Census Bureau (we focus on the Retail Sales excluding Food Service, Autos, Building Materials, and Gas Stations statistics) has shown year-over-year growth, slow from the average mid-teens numbers seen in 2021, to a still healthy upper-single digits number in 2022 [Figure 2]. over the last 20 years, pre-2020.

We think the move lower in yields may be a bit premature as we expect the economy to stay out of a recession this year. Securities and advisory services offered through LPL Financial (LPL), a registered investmentadvisor and broker/dealer (member FINRA/SIPC). due to expectations of slowing economic growth.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. All index data from FactSet.

Market participants remained on edge due to high inflation and the risk that the Federal Reserve over-tightens monetary policy to combat it, potentially sending the economy into recession. Securities and advisory services offered through LPL Financial (LPL), a registered investmentadvisor and broker/dealer (member FINRA/SIPC).

economy in mid-March, 62% of S&P 500 companies beat estimates, and aggregate earnings were within one percentage point of expectations. economy, as measured by gross domestic product, so the ISM index tends to have some predictive power when it comes to earnings. The S&P 500 is more manufacturing-heavy than the U.S. Conclusion.

However, as Fed rate hikes flow into the real economy, the risk of a recession increases, which should help bring down yields. Over the past six months, the Fed has been aggressively raising short-term interest rates in an effort to arrest these continued consumer price increases and deliberately slow the economy.

I’m a portfolio manager here at Bell InvestmentAdvisors. The first is 2022investment performance. Then, I’m going to be discussing inflation and interest rates and how those affect the value of your investments. Slide 4: 2022: U.S. Slide 5: 2022 in Review: Bonds 08:47 Onto bonds. stock market.

The news on the economy and corporate profits hasn’t been great lately, but thanks to low expectations, it’s been good enough to push stocks nicely higher. The index rallied 11% in March 2022 before turning lower again. economy into recession, causing unemployment to rise and slashing corporate profits. Encouraging Signs.

Marc Zabicki , CFA , Chief Investment Officer, LPL Financial . You may also be interested in: Inflation and Rising Rates Supports Value – November 14, 2022. How Midterm Elections May Move Markets – November 7, 2022. Federal Reserve Preview: TRICK or Treat? – October 31, 2022. IMPORTANT DISCLOSURES.

The intermediate core bond and core plus bond categories represent the two most popular categories by assets under management (AUM) and represent 45% of all asset across the taxable bond open-ended mutual fund space (as of August 2022). In simplest terms, “plus” indicates a more flexible investment mandate across fixed income markets.

We proposed last month that investors have started to look beyond the Fed and shift their attention to corporate earnings and the economy. Clients may recall a political debate surrounding a “technical recession” after two negative GDP reports during the first half of 2022. The economy grew at an inflation-adjusted rate of 2.1%

And third, import prices have moderated since the beginning of 2022 and as import prices slow, we expect consumer prices to eventually reflect the slowdown in import prices. The year 2022 started out with import prices rising very quickly on a monthly basis. Second, strength in the U.S. What was keeping inflation elevated?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content