This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

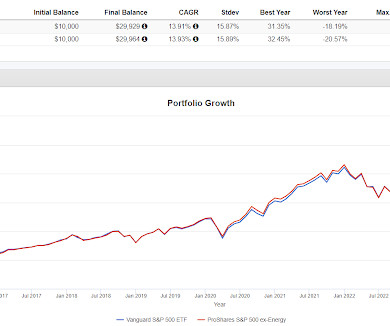

Staying long through the 60-day 34% drop during the 2020 pandemic; getting out of the market ahead of the 2022 rate hiking cycle; and getting back in October 2022 for the next bull leg. I have dozens of examples of traders who made the right call for some of the above for all the wrong reasons. By Jeff Sommer New York Times, Nov.

This piece was inspired by this fantastic Josh Brown rant on CNBC about how the 60/40 stock/bond portfolio isn’t dead. The 60/40 stock/bond portfolio is the gold standard of portfolios. The math on the 40% slice is much cleaner. Give it a watch. I don’t love a standalone bond aggregate as a 40% bond slice.

There were 127 million US households as of 2022. First, is the math right based on my numbers? I think it can be a productive portfolio addition betting on the asymmetry which of course argues for starting very small. The above two portfolios are pretty consistent with a lot of the work we do here.

A portfolio that goes narrower than an S&P 500 500 or total market fund probably has some exposure to low vol, dividends and the others. And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out.

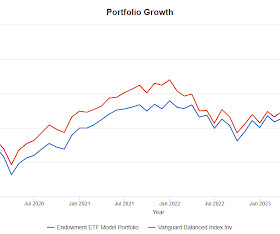

The "endowment" result is very close to red line VBAIX every year except 2020 when it lagged by almost 600 basis point and 2022 when it outperformed by about 500 basis points. If any of us had constructed this portfolio and implemented it for ourselves, it would have been a very acceptable result.

The fund owns a lot of puts and should go up a lot in the face of a crash but not necessarily a slow protracted decline like there was in 2022. According to Portfoliovisualizer, CYA dropped 46.10% in 2022. The fund in question is the Simplify Tail Risk Strategy ETF (CYA). Here's what caught my eye that it might have blown up.

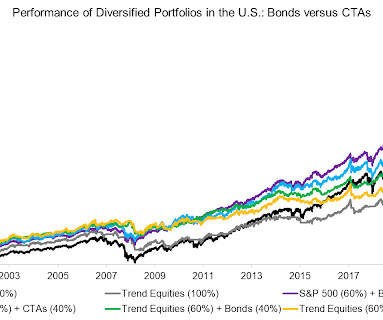

It is of course not dead but bonds became a far less effective diversifier years ago, long before 2022 when interest rates started going up. The risk was there for years, 2022 when when there was a consequence to investors who took that risk. I would say that is a very big bet but the math in their backtest supports it.

So I took it upon myself to go off and took a course in bond math, took another course in derivatives and realized the underlying fundamental concepts were barely, I mean, it wasn’t even high school math in most cases. I didn’t know what any of these terms meant. And there was a problem with 168 of them at the end of 2008.

We've talked just a couple of times about the market becoming increasingly concentrated which just in terms of math means that a diversified strategy will lag for as long as the big names do well. Despite outperforming for 15 years, PSLDX was down 43% in 2022 which speaks to what diversification is about. In 2022 they didn't work.

And then just a little math, the "guarantee" based on the 50/50 allocation would be 2.5% Down less clearly worked in 2022 and YTD HEQT is lagging the S&P 500 by 400 basis points. Portfolio 3 with 65% HEQT and 35% SPHB was down quite a bit less than the S&P 500 last year and the standard deviation is noticeably lower too.

The Wall Street Journal had an article about the standard 60/40 portfolio , that is 60% allocated to stocks and 40% allocated to fixed income. My experience is that the typical retired person/couple expects growth in exchange for some volatility from the equity portion of their portfolio, they don't want it from their fixed income sleeve.

In my ongoing quest to redefine portfolio construction, I've mentioned labeling asset classes based on their attributes versus just their proper names like growth which could include more than just equities or inflation protected which could include more than just TIPS and so on. We talk frequently about portfolios being relatively simple.

She has a really fascinating background, very eclectic, a combination of math and law. You, you get a, a BS in Mathematics and a JD from Boston University Math and Law. It is something, math has always come easy to me since a child. I didn’t get an advanced degree in math. Not the usual combination. What happened?

In fact, as of September 2022, over 70 million Americans were collecting benefits. [1] You might have a generic 60/40 portfolio that you expected to cover the rest of your income needs but that possibly needs updating after recent market activity. 3] So, it’s easy math: the less you work, the less you’ll earn.

Here's a quote I saw attributed to Barry Ritholtz: “The Best Portfolio is probably the one which sacrifices a bit of performance, but helps you sleep at night.” Barry's quote reminded me of another influence on how I try to manage client portfolio volatility and why I use alts (yes, that conversation continues). Cannot be done?

The Math Behind the Growth Let’s take a step back and think about what it would take for a company like Apple to reach a $10 trillion market cap. trillion, and by the end of 2022, it had soared to $40.5 A well-diversified portfolio can help protect against the unpredictable nature of the stock market.

Global Leaders Investment Letter: June 2022 mhannan Thu, 06/16/2022 - 11:30 Just want the PDF? We discount each year at our 10% minimum weighted average cost of capital (WACC) and some infinite series maths gives us the basis for some rough approximations 2.

The way the math works, a 67% allocation to NTSX (Portfolio 2 with 33% in the T-bill ETF) equals 100% in Vanguard Balanced Index Fund (VBAIX) which is a proxy for 60/40 and Portfolio 3. Portfolio 1 is 100% in NTSX which in 2022 was down 25.84% versus down 16.85% for Portfolio 2 and 16.87% for Portfolio 3.

Her job is portfolio and product solutions and that means she could go anywhere in the world and do anything. One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics.

I — I loved math, but really, I was going to go down that literature route more than anything else and — and study Spanish literature. I — I — I think 50 plus 75 plus 75 plus whatever happened September 2022, that’s the end of the soft landing. RITHOLTZ: Applied Mathematics, Quants, those guys, yeah.

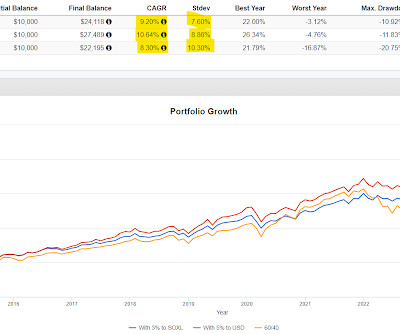

We regularly look at capital efficiency and its potential uses in portfolio construction. Consider the following two portfolios. In terms of risk weighting or volatility weighting, a smaller allocation to semiconductors could deliver the same benefit to a portfolio as a larger weighting to broad tech.

In fact, the Federal Reserve has raised the upper limit federal funds rate by 5% since the beginning of 2022. Again just using simple math, this presumes the par value will roll over each month and reinvest at the same rate to get to the annual yield. Hold cash or invest? Interest rates have skyrocketed since the end of 2021.

A little more specifically the need for diversified portfolios persists with the implication that bonds are the way to get this done. This chart contributes to the logic supporting a 60/40 portfolio. As a matter of math, it cannot repeat the run from 8.5% Portfolio 2 above has 65% in growth. in November.

Here's how QYLD has done for the last 5 years coming into 2022, so before the market was underway, versus the NASDAQ. And here is 2022, the bear market. Similar to PUTW, it didn't offer protection during the pandemic crash of 2020 but only dropping half of what the S&P 500 index has dropped in 2022 is impressive and surprises me.

That is correct, technically but whatever you're looking for from REITs, or private equity or any of the others, you're not going to see it impact the portfolio as part of an index fund. Mistakes during those types of events are what managing portfolios is all about.

You would offer three of their stock picks where they were probably touting stocks they wanted to unload from their portfolio. But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. That’s exactly right.

This year, its performance has it the top 1% of mutual funds but in “2021 and 2022 it was ranked in the bottom 100th percentile.” Here I am talking not just portfolio management but overall lifestyle, habits and choices and yes this does filter into my day job managing investment portfolios. So it is today with bonds.

Risk parity portfolios are particularly vulnerable when their active weighting algorithms fail to predict shifts in asset correlations." The authors noted that risk parity did very well for a long time but that "bond based risk-parity failed miserably in 2022." The leverage is usually obtained by using treasury futures.

Those of us called upon professionally to write about market performance in 2022 as the year ends are necessarily struggling for the right verbiage. That’s because, in language as plain as I can make it, pretty much every market and sector has had a very bad 2022. The Bloomberg U.S. Things are no better overseas.

If at the start of the year, someone put 100% into the Vanguard Balanced Index Fund (VBAIX) as a proxy for a 60/40 portfolio, then to employ a portable alpha strategy, they could use leverage to add something to hopefully make it additive to returns. Imagine the Intel scenario of down 59% on top of VBAIX dropping 16% in 2022.

If you’re at all interested in focused portfolios, the concept of quality as a sub-sector under value and just how you build a portfolio and a track record, that’s tough to beat. Dick Mayo was a traditional, I’d say portfolio, strong portfolio manager focused on US stocks. So I was at Harvard.

Charles Schwab just released their 2022 RIA Benchmarking Study and I decided to crunch the numbers and see what the data shows. With a traditional 60/40 allocation, this portfolio would have grown about 75.5% For comparison, a passive 60/40 bond portfolio, as mentioned above, grew at a CAGR of 11.9%. AUM Growth.

After this meteoric multi-year rise, stock values started to come back to earth in 2022, and the rocket ship turned into a roller coaster during January. Math Matters. I did okay in school and was educated on many different topics, including the basic principle that math matters. Source: Calafia Beach Pundit. www.Sidoxia.com.

So I came down, met with our head of the portfolio review department, which oversees our external managers, met with our head of brokerage, and then met with the head of bind indexing, who was Ken Volpert at the time. And she was like, “You should come down and talk to some people at Vanguard.”

And when used for ROE, as per the basic rule of math, if the denominator decreases, the fraction as whole increases i.e, On a yearly basis, from 2018 to 2022, the company has a return on equity of 36.56%, 45.3%, 70.39%, 105.76%, and 104.53% respectively. The ROE numbers from 2018 to 2022 are 57.17%, 49.79%, 42.74%, 71.64%, and 83.3%

From the company’s website, as of May 16th, 2022: Single people. From the company’s ADV Part 2 brochure, as of May 16th, 2022: Fees are set as a fixed annual fee, paid quarterly, and based approximately on the total time required to service an account yearly. But, let’s say you had a much smaller portfolio.

I was little concern during 2022 with high inflation with the market downturn. If the 4% treasury portfolio pays out $50,000 today, it will pay the same $50,000 in 2038 with no growth in account value. Part of the math that determines options premiums is the risk free rate of return from T-bills.

Part of the math that determines options premiums is the risk free rate of return from T-bills. We've also looked at countless ways to incorporate a small allocation to covered calls funds to help reduce portfolio volatility, so using them as alts in a matter of speaking. In 2022 it dropped 13% versus about 19% for the S&P 500.

All of their portfolio managers not only are substantial investors in each of their funds, but they do a disclosure year that shows each manager by name and how much money they have invested in their own fund. So we really think that it creates alignment to have our portfolio managers meaningfully owning shares of the funds that they manage.

Here are some other numbers compared to the S&P 500 and VBAIX which is a proxy for a 60/40 portfolio. The way the math works, a 67% allocation to NTSX replicates 100% into a 60/40 portfolio which leaves 33% left over to do something. In 2022, VBAIX was down 16.87% while Portfolio 2 was only down 10.77%.

But you know exactly how they’re going to interplay within a portfolio, hugely powerful. You know, it’s not the equity market, and I run some big equity portfolios, you know, different. But, you know, it’s been in a portfolio for a long time. Last year, it’s in our tactical portfolios.

Both 2021 and 2022 each had 14 upsets; there were 10 upsets in 2023 and nine in 2024, if only three in 2007. Duke math professor Jonathan Mattingly claimed the average college basketball fan has a far better chance of achieving bracket perfection than one in 9.2 It applies to your personal portfolio, too. quintillion.

One of our colleagues, Ken Stuzin, likens portfolio construction to Darwinian Investing – it is about survival of the fittest. In a concentrated portfolio, it is the losers that kill you. What sort of hit rate should we then expect within their portfolio? 5 As Table 2 below highlights, this team appears to be seriously good!

I was always good at math, but I really, I just didn’t relate to things that were more esoteric bonds options. I worked in sort of a quasi portfolio management role for like a single client account type business. And then I worked on it throughout the GFC and then became the senior portfolio manager during the recovery period.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content