This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? I generally consider this a plan for the self-employed.

Health savings accounts (HSA) provide another vehicle to save for retirement. Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. High deductible health insurance plans . These limits increase to $3,650 and $7,300 for 2022.

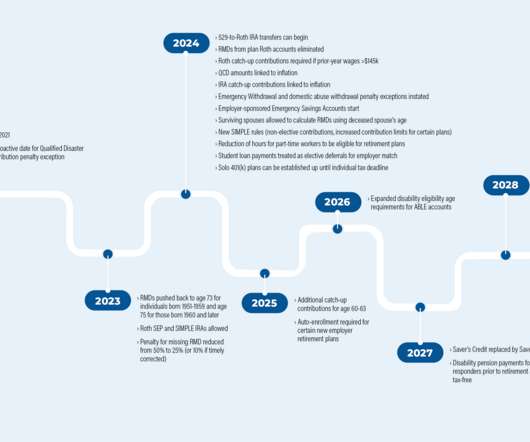

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

Vestwell conducted the fourth-annual “Retirement Trends Report” in fall 2022 and received responses from almost 1,300 savers, 500 financial advisors and 250 small businesses.

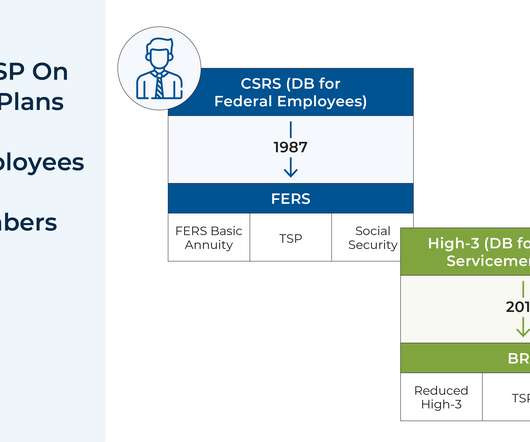

government is the largest employer in the country, it can be especially helpful for advisors to be familiar with the ins and outs of (and recent changes to) the Federal government’s own defined contribution plan: the Thrift Savings Plan (TSP). In 2022, the TSP underwent a series of changes impacting its many account holders.

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns. Read More.

Realistic RetirementPlanning My children have consistently (and kindly) remarked about how grateful they are to have been able to graduate (with honors) from fine universities without any debt. Our retirementplanning took a hit to do so. Much retirementplanning advice focuses on saving more and saving earlier.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that Congress appears poised to pass a series of changes affecting retirementplanning, dubbed “SECURE ACT 2.0”, ”, by the end of the year. Social Security COLA for 2023.

Among other measures, the proposal would amend the current 5-part test that determines fiduciary status for retirement accounts by defining as a fiduciary act a one-time recommendation to roll funds from a company retirementplan to an Individual Retirement Account (IRA), strengthen advice standards for independent insurance professionals, apply to (..)

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns. Read More.

Podcasts Christine Benz and Jeff Ptak talks with Jamie Hopkins of Carson Wealth about some common retirementplanning questions. ft.com) Who really benefits from 529 plans? nytimes.com) Planning Doug Boneparth, "Cash flow lives at the heart of financial organization." morningstar.com) 20 thing to do before year-end.

Among these are your longevity, lifestyle, comfort with market performance, sequence of return risk, current health, housing plan, proportion of fixed to variable expenses, proximity to children and so much more. One or two million dollars may seem like a lot of money to have set aside for retirement. A Retirement Reality Check.

In spite of what was said on PBS Frontline The Retirement Gamble and elsewhere in the press, in my opinion 401(k) plans are one of the best retirement savings vehicles available. Here are 4 steps to make sure that your 401(k) plan is working hard for your retirement. Get started . Are you self-employed ?

From there, we have several articles on investments: How Morningstar plans to simplify its rating system amid continued concerns about its effectiveness. A study suggests that some fund companies are misleading investors by changing their benchmark indices to make their performance look better.

Also in industry news this week: As broker-dealers increasingly offer fee-based planning services, RIAs are responding by enhancing their own service offerings, and offering alternative fee structures to differentiate themselves from the competition.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with a research study suggesting that the market volatility experienced in 2022 could increase demand for financial planning services.

Nevertheless, there is potential for many individual RIAs to expand their staffing further, with the addition of specialized planning and operations roles being seen as a potential avenue to boost firm growth.

We also have a number of articles on retirementplanning: How the variability in annuity payouts across annuity providers has exploded in 2022, creating an opportunity for advisors to add value to clients by comparison shopping across insurance companies.

Also in industry news this week: The Office of Management and Budget (OMB) has completed its review of the Department of Labor's new "fiduciary rule ", indicating that it could be released in the coming days or weeks (though, like its predecessors, its ultimate disposition is likely to be determined in the courts) The IRS announced this week that it (..)

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. The less it matters, the easier it is to be bold and outside of the mainstream.4

For 2022 these limits increase to $61,000 and $67,500. For 2022 these contribution limits increase to $20.500 and $27,000, plus the employer-funded profit sharing component in both years. Just like a 401(k) plan with an employer, the Solo Roth 401(k) option allows larger Roth contributions than the Roth IRA limits.

In this guide, we’re going to present the 10 best long-term investment strategies for 2022. The table below provides a quick summary of each of the 10 best long-term investment strategies for 2022, along with the main features and benefits of each. Below is our list of the 10 best long-term investment strategies for 2022.

At their most basic level, executive compensation plans are designed to attract, retain and motivate top talent and leadership. But truly successful plans are designed to be much more than providing a high salary to a key employee – they support the business’s philosophies, values, and mission. . Direct Compensation & Benefits.

At age 50, workers with certain qualified retirementplans can make annual “catch-up” contributions in addition to their normal contributions. In 2022, you can contribute up to $6,000 to an IRA if you are under 50 and an additional $1,000 if you are 50 or older. Some 401(k) plans allow this, and others do not. 3] IRS.gov.

Financial bloggers often portray the traditional IRA vs. the 401(k) plan as a debate, as if one plan is better than the other. In truth, they’re very different plans, and they fill very different needs. If you can, you should plan to have both. This is especially true if your 401(k) plan is fairly restrictive.

After a strong finish in 2020 and very solid returns in 2021, we’ve seen a lot of market volatility so far in 2022. Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. If not perhaps you are taking more risk than you had planned. Do nothing.

The original SECURE Act, signed into law in December 2019, changed many of the long-standing rules governing IRAs and other retirement accounts, and no single measure in the legislation had a more seismic impact on planning than the changes to the post-death distribution rules for retirement accounts.

Qualified retirementplans – such as 401(k)s, 403(b)s and IRAs – offer clear tax advantages. Taxpayers with qualified retirement accounts are required to start taking distributions from the accounts once a certain age is reached. Jamie Hopkins, Managing Partner, Wealth Solutions. Your life expectancy factor is 26.5.

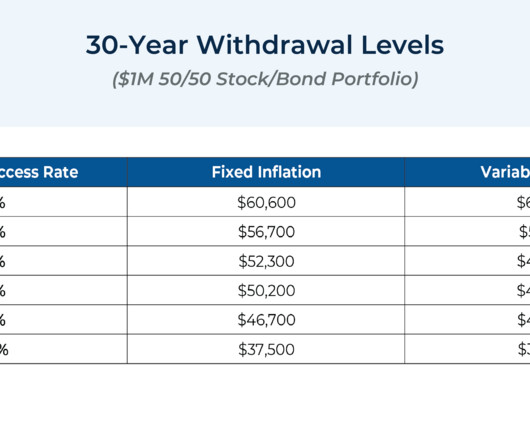

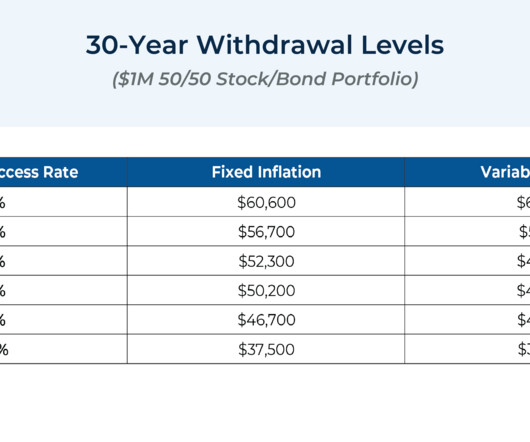

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Here are some key points to use with clients as you help them assess their retirementplans.

The 2022 economic climate has been bumpy for most and, in some cases, even bumpier for retirees. 1] However, in 2022, this number spiked to 9.1% 2] With higher prices in consumer goods, retirees may have had to reevaluate their withdrawals and spending on retirement accounts as their income became strained. 1] [link]. [2]

With market volatility and inflation affecting people’s finances, talk about investment strategies and portfolio longevity seems to dominate retirementplanning conversations. But one of the most important aspects of retirement is often overlooked in these conversations: healthcare costs. 1] [link]. [2] 2] [link]. [3]

As multiple recessionary signs flash red including bank failures, persistent inflation, and ongoing volatility, investors of all ages are increasingly nervous about the state of the markets and economy and what it means for their retirementplans and their ability to save for retirement.

2022 has been a difficult and trying year for stock and bond indexes in both emerging and developed markets. As we look forward to 2023, the IRS recently announced that the contribution limits for employer-sponsored retirementplans are going up. 529 College Savings Plans. The gift limit for 2022 is $16,000.

The Roth IRA vs traditional IRA – they’re basically the same plan, right? While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Not exactly. The most basic requirement is that you have earned income.

Estates of decedents who die during 2023 have a basic exclusion amount of $12,920,000, up from a total of $12,060,000 for estates of decedents who died in 2022. The annual exclusion for gifts increases to $17,000 for the calendar year 2023, up from $16,000 for the calendar year 2022. SmartAsset’s Federal Income Tax Calculator for 2022.

Form 1099-R reports distributions from pensions, annuities, retirementplans etc. Records for any stocks or other investments you sold in 2022, including crypto transactions or other digital assets. Make the last step in your tax filing process setting aside time to review your return and plan for 2023. Did you have AMT?

Some of the measures in the bill include increasing the required minimum distribution age, raising catch-up contribution limits, permitting some rollovers from 529 plans to Roth IRAs, and expanded access to employer plans. retirement changes. 529 plan to Roth IRA rollovers. 9 major Secure Act 2.0 The Secure Act 2.0

The risk of selling volatility this way is that the market gets hit either with a fast decline like the 2020 Pandemic Crash or a slower large decline like in 2022 causing the short puts to get assigned. Munnell along with Teresa Ghilarducci are like the aunties of retirement which I am saying in a positive way. People have busy lives.

As 55% of Americans say they don’t have enough saved for retirement, this bipartisan legislation primarily seeks to make it easier to contribute to retirementplans and use those funds appropriately for their needs in retirement. Expanded Savings Opportunities. The SECURE 2.0 The SECURE 2.0 The SECURE 2.0

And how does it compare to the 401k and other retirementplans that exist? A Simple IRA, or Savings Incentive Match Plan for Employees, is a type of employer-sponsored retirement savings plan that is designed to be easy to set up and maintain for small business owners. What is a Simple IRA?

If you are looking for opportunities to grow your business, expanding your services to clients at all stages of the financial planning lifecycle creates new opportunities for you to reach those households in search of professional advice. People in this stage may have just graduated from college and recently joined the working world.

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

So, let’s say you contribute money to a traditional 401(k) plan in your 20s. This gives you ample time to grow your savings and investments for retirement. IRAs and 401(k)s are primarily designed to help fund retirement not pass wealth onto future generations. 31, 2022 and you turned 75 in 2023. 31 each year.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content