This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? You need to start a retirementplan today.

Health insurance plans with an annual deductible of at least $1,4000 for a single person and $2,800 for a family qualify for use with HSAs in 2021, with no change in these limits for 2022. These types of plans are becoming more common with employers and are available privately as well. How the HSA works . Click To Tweet.

Vestwell conducted the fourth-annual “Retirement Trends Report” in fall 2022 and received responses from almost 1,300 savers, 500 financial advisors and 250 small businesses.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that Congress appears poised to pass a series of changes affecting retirementplanning, dubbed “SECURE ACT 2.0”, ”, by the end of the year. Social Security COLA for 2023.

Among other measures, the proposal would amend the current 5-part test that determines fiduciary status for retirement accounts by defining as a fiduciary act a one-time recommendation to roll funds from a company retirementplan to an Individual Retirement Account (IRA), strengthen advice standards for independent insurance professionals, apply to (..)

Podcasts Christine Benz and Jeff Ptak talks with Jamie Hopkins of Carson Wealth about some common retirementplanning questions. ft.com) Who really benefits from 529 plans? nytimes.com) Planning Doug Boneparth, "Cash flow lives at the heart of financial organization." morningstar.com) 20 thing to do before year-end.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Social Security is a federal retirementplan originally created under the Social Security Act of 1935.

Also in industry news this week: As broker-dealers increasingly offer fee-based planning services, RIAs are responding by enhancing their own service offerings, and offering alternative fee structures to differentiate themselves from the competition.

You may be able to do everything online, otherwise contact the plan administrator at your company. There are a number of retirementplan options to consider. If you don’t have a retirementplan in place for yourself, do this today. You work way too hard not to be putting something away for retirement.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with a research study suggesting that the market volatility experienced in 2022 could increase demand for financial planning services.

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

But despite recognizing the impact of investment variability and sequence of return risk on a financial plan, advisors have generally ignored the same historical trends for inflation in their clients' financial plans.

We also have a number of articles on retirementplanning: New research suggests that while the average senior will amass hundreds of thousands of dollars in health care expenses in retirement, the net cost they have to pay is not nearly as high.

We also have a number of articles on retirementplanning: How the variability in annuity payouts across annuity providers has exploded in 2022, creating an opportunity for advisors to add value to clients by comparison shopping across insurance companies.

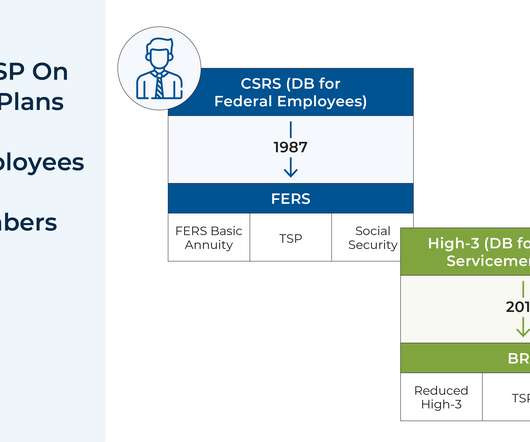

Roth contribution options and employer matches) are common to other workplace-defined contribution plans, the TSP has certain unique attributes, including lower fees than many private-sector plans and a fixed-income investment option exclusive to the plan. While many features of the TSP (e.g.,

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. The less it matters, the easier it is to be bold and outside of the mainstream.4

Nevertheless, there is potential for many individual RIAs to expand their staffing further, with the addition of specialized planning and operations roles being seen as a potential avenue to boost firm growth.

In this guide, we’re going to present the 10 best long-term investment strategies for 2022. The table below provides a quick summary of each of the 10 best long-term investment strategies for 2022, along with the main features and benefits of each. Below is our list of the 10 best long-term investment strategies for 2022.

For 2022 these limits increase to $61,000 and $67,500. For 2022 these contribution limits increase to $20.500 and $27,000, plus the employer-funded profit sharing component in both years. The Solo 401(k) can be a great self-employed retirementplan. If you are self-employed you need to start saving for your retirement.

Know these 3 ages that can help you get the most out of your retirement accounts. At age 50, workers with certain qualified retirementplans can make annual “catch-up” contributions in addition to their normal contributions. 3 Now, many retirees have more time to let their retirement savings grow tax-free. 3] IRS.gov.

The 2022 economic climate has been bumpy for most and, in some cases, even bumpier for retirees. 1] However, in 2022, this number spiked to 9.1% 2] With higher prices in consumer goods, retirees may have had to reevaluate their withdrawals and spending on retirement accounts as their income became strained. 1] [link]. [2]

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Here are some key points to use with clients as you help them assess their retirementplans.

With market volatility and inflation affecting people’s finances, talk about investment strategies and portfolio longevity seems to dominate retirementplanning conversations. But one of the most important aspects of retirement is often overlooked in these conversations: healthcare costs. 1] [link]. [2] 2] [link]. [3]

As multiple recessionary signs flash red including bank failures, persistent inflation, and ongoing volatility, investors of all ages are increasingly nervous about the state of the markets and economy and what it means for their retirementplans and their ability to save for retirement.

2022 has been a difficult and trying year for stock and bond indexes in both emerging and developed markets. As we look forward to 2023, the IRS recently announced that the contribution limits for employer-sponsored retirementplans are going up. 529 College Savings Plans. The gift limit for 2022 is $16,000.

The risk of selling volatility this way is that the market gets hit either with a fast decline like the 2020 Pandemic Crash or a slower large decline like in 2022 causing the short puts to get assigned. Munnell along with Teresa Ghilarducci are like the aunties of retirement which I am saying in a positive way. People have busy lives.

After a strong finish in 2020 and very solid returns in 2021, we’ve seen a lot of market volatility so far in 2022. The S&P 500 index was down about 17.6% on a year-to-date basis as of Friday’s close. The combination of higher inflation, higher interest rates and the situation in Ukraine are all fueling this market volatility.

There are many components of the 2022 Act that will impact employers that aren’t outlined below. would permit employers to make matching contributions to an employee’s 401(k) and 403(b) retirementplan, even if the worker isn’t saving themselves. Here are some of the biggest changes in the Secure Act 2.0, The Secure Act 2.0

Every now and then we talk about expat living as part of a retirementplan, usually the context is an underfunded retirementplan. Portfolio 2 was spared a couple of hundred basis points which is better than nothing and Portfolio 3 did very well in 2022. One popular country in expat living circles is Ecuador.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Either plan is an excellent choice, particularly if you’re not covered by an employer-sponsored retirementplan. Not exactly.

Form 1099-R reports distributions from pensions, annuities, retirementplans etc. Records for any stocks or other investments you sold in 2022, including crypto transactions or other digital assets. There are a couple of tax moves you still have time to make to impact your 2022 return. Did you have AMT?

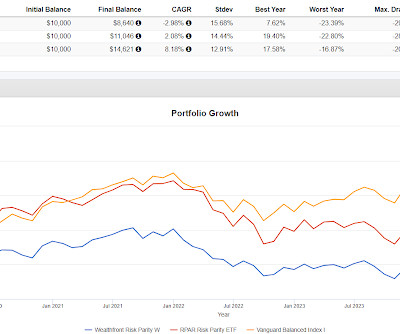

In 2022, it was up 104 basis points (total return). but it was low in 2022 when it mattered. In 2022, when managed futures was having its heyday, there were all of a sudden a lot of calls about putting 20% or more in managed futures. The results were fascinating. We pounded the table here why that was probably a bad idea.

And how does it compare to the 401k and other retirementplans that exist? Being a self-employed retirementplan , the SIMPLE IRA gives you the discretion of what exactly you want your money invested into. . You are allowed to contribute up to $15,500 in 2023 , up from $14,000 in 2022, per year in a SIMPLE IRA.

I expanded on it a little bit and noted it's not particularly relaxing but I would reiterate that this is a great time to lean forward and learn about some things in real time versus looking at a backtest from a benchmark event like the 2020 Pandemic Crash or 2022. All of the different factors have their moments in the sun.

For 2022, the IRS allows taxpayers to contribute up to $20,500 to their 401(k) accounts. You contribute after-tax dollars to be able to make tax-free withdrawals in retirement subject to certain conditions i.e. you must be 59.5 For 2022, the Roth IRA contribution limit is set at $6,000 by the IRS.

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

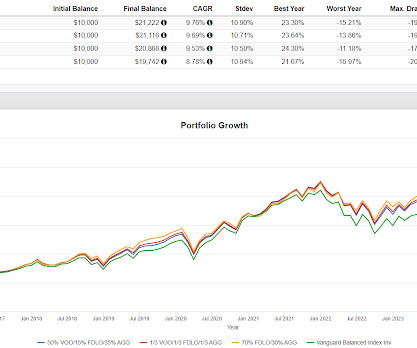

The max drawdowns of the backtested portfolios bottomed out in late 2022 as follows To the extent quadrant style might intersect with all-weather, you can decide for yourself whether any of them were all weather enough. There's no wrong conclusion to draw, do you think they are all-weather enough?

All three were better than VBAIX in 2022 by 150-550 basis points. Somehow, it did worse than the S&P 500 by several hundred basis points in 2022. Based on the chart, I'm guessing that SPD was positioned in such a way as to miss the bounce that started in late 2022. The results are not skewed by one year.

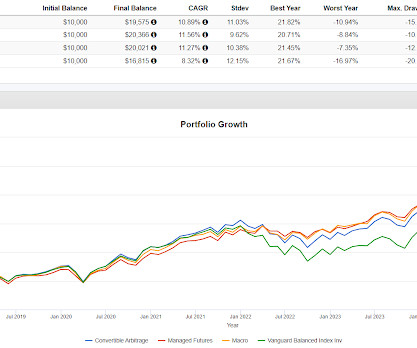

Weaving in the historical part of the essay he points out that in addition to 2022, there have been several events before 1981 where the traditional 60/40 did very poorly, he seemed to be blaming the 40 allocated to bonds. In terms of crisis alpha in rough times, convertible arb didn't really help in 2022 but managed futures and macro did.

Because of low current tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. The high inflation of 2022 means that in 2023, the standard deduction will be higher, and federal income tax brackets will be expanded. They’re good, but not great.

You can see on the backtest, RPAR fairing worse than VBAIX by almost 600 basis points in 2022 and then didn't really come back the way VBAIX did. Even RPAR, compounding at 2% in an 8% world for VBAIX has struggled. RPAR has 70% in treasuries although not all of them are long term. Risk parity is a good example of a great story.

The stock market has returned an average of between 9% and 11% over the past 90 years and that’s the kind of growth that you’ll need to tap into if you want to retire at 50. Your retirementplan shouldn’t be. Get in touch with an Independent Financial Professional to see if you're on track to meet your retirement goals.

More than half of non-retired women believe inflation presents the most pressing and urgent threat to their retirement portfolios, followed closely by economic recession and market volatility. More than half of women are working with a financial professional in 2023, compared to 45% in 2022.

This increases to $19,560 for 2022. During the year in which you reach your full retirement age the annual limit is increased. For 2021 this increased limit is $50,520, for 2022 this limit is $51,960. Earned income is defined as income from employment or self-employment.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content