This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? You need to start a retirementplan today.

Health insurance plans with an annual deductible of at least $1,4000 for a single person and $2,800 for a family qualify for use with HSAs in 2021, with no change in these limits for 2022. These types of plans are becoming more common with employers and are available privately as well. Health Savings Accounts and retirement .

Podcasts Christine Benz and Jeff Ptak talks with Jamie Hopkins of Carson Wealth about some common retirementplanning questions. peterlazaroff.com) Dan Kemp and Ollie Smith talk with Joe Wiggins author of the new book "The Intelligent Fund Investor." (ft.com) Who really benefits from 529 plans?

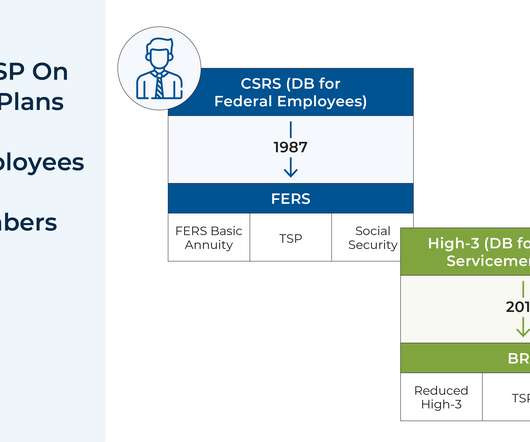

Roth contribution options and employer matches) are common to other workplace-defined contribution plans, the TSP has certain unique attributes, including lower fees than many private-sector plans and a fixed-income investment option exclusive to the plan. While many features of the TSP (e.g.,

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. When you get it wrong, it crushes your retirementplans. Let’s add some color to the discussion on timing itself and add a little nuance.1

It is March…that means you have just about 5 weeks left to get organized and submit your tax return. The tax deadline is April 18, 2023 (some taxpayers in disaster areas in California, Georgia and Alabama have an extended deadline). Gathering all your documents is crucial to complete a tax return free of mistakes.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Social Security is a federal retirementplan originally created under the Social Security Act of 1935.

In this guide, we’re going to present the 10 best long-term investment strategies for 2022. The table below provides a quick summary of each of the 10 best long-term investment strategies for 2022, along with the main features and benefits of each. Below is our list of the 10 best long-term investment strategies for 2022.

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

In November 2022, proponents of the Massachusetts ‘millionaires’ tax (question 1) won their bid to nearly double the income tax rate on individuals with taxable income over $1M a year. As proposed, the new legislation would increase these tax rates to 9% and perhaps even 16% , respectively, starting in 2023.

For 2022 these limits increase to $61,000 and $67,500. For 2022 these contribution limits increase to $20.500 and $27,000, plus the employer-funded profit sharing component in both years. Check with your financial or tax advisor as to how much you will be able to contribute. Investment flexibility . Photo credit: Flickr.

A major decision in retirementplanning is whether to make pre-tax or Roth (after-tax) 401k contributions. Pre-tax contributions go into your retirement account with money that has not been taxed, and then taxes will be paid when the funds are withdrawn in retirement.

There are rules and regulations that can help you avoid higher taxes and penalty fees and help you structure your income to minimize taxes. Know these 3 ages that can help you get the most out of your retirement accounts. Age 59½ is the earliest you can withdraw funds from an IRA account and pay no early withdrawal penalty tax.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. Here are some key points to use with clients as you help them assess their retirementplans.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Either plan is an excellent choice, particularly if you’re not covered by an employer-sponsored retirementplan. Not exactly.

This increases to $19,560 for 2022. During the year in which you reach your full retirement age the annual limit is increased. For 2021 this increased limit is $50,520, for 2022 this limit is $51,960. Any money that may have been withheld from your benefits such as taxes or Medicare premiums. Combined income. %

2022 has been a difficult and trying year for stock and bond indexes in both emerging and developed markets. As we look forward to 2023, the IRS recently announced that the contribution limits for employer-sponsored retirementplans are going up. 529 College Savings Plans. The gift limit for 2022 is $16,000.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. There are many components of the 2022 Act that will impact employers that aren’t outlined below. 529 plan to Roth IRA rollovers. The Secure Act 2.0 The Secure Act 2.0

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement. Is there a better way?

401(k)s and Roth IRAs are some of the most commonly used retirement accounts. Some opt for a 401(k) account simply because it comes with the advantage of getting an employer match, while some go for a Roth IRA account to be able to make tax-free withdrawals in retirement. Thus, you end up paying fewer taxes on your income.

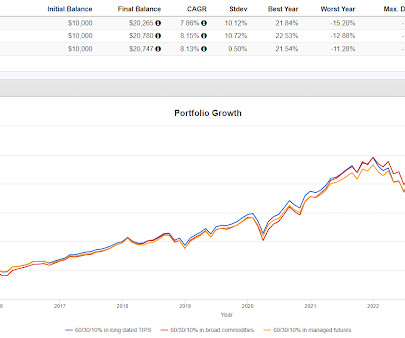

In 2022, it was up 104 basis points (total return). but it was low in 2022 when it mattered. In 2022, when managed futures was having its heyday, there were all of a sudden a lot of calls about putting 20% or more in managed futures. The results were fascinating. We pounded the table here why that was probably a bad idea.

And how does it compare to the 401k and other retirementplans that exist? A Simple IRA, or Savings Incentive Match Plan for Employees, is a type of employer-sponsored retirement savings plan that is designed to be easy to set up and maintain for small business owners. What is a Simple IRA?

The risk of selling volatility this way is that the market gets hit either with a fast decline like the 2020 Pandemic Crash or a slower large decline like in 2022 causing the short puts to get assigned. Munnell along with Teresa Ghilarducci are like the aunties of retirement which I am saying in a positive way. People have busy lives.

The stock market has returned an average of between 9% and 11% over the past 90 years and that’s the kind of growth that you’ll need to tap into if you want to retire at 50. Your retirementplan shouldn’t be. Get in touch with an Independent Financial Professional to see if you're on track to meet your retirement goals.

I expanded on it a little bit and noted it's not particularly relaxing but I would reiterate that this is a great time to lean forward and learn about some things in real time versus looking at a backtest from a benchmark event like the 2020 Pandemic Crash or 2022. All of the different factors have their moments in the sun.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. For high earners, converting an IRA to a Roth IRA while you’re still working could be the worst time of all.

That will give you a combined contribution of $13,000, which will also be fully tax-deductible. There's no time like the present to begin preparing for your retirement. When you turn age 72, you’re required to begin receiving distributions from the plan. Ads by Money. We may be compensated if you click this ad.

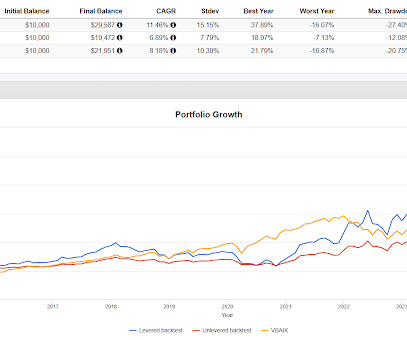

You can see on the backtest, RPAR fairing worse than VBAIX by almost 600 basis points in 2022 and then didn't really come back the way VBAIX did. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Risk parity is a good example of a great story.

Every now and then we talk about expat living as part of a retirementplan, usually the context is an underfunded retirementplan. Portfolio 2 was spared a couple of hundred basis points which is better than nothing and Portfolio 3 did very well in 2022. One popular country in expat living circles is Ecuador.

The max drawdowns of the backtested portfolios bottomed out in late 2022 as follows To the extent quadrant style might intersect with all-weather, you can decide for yourself whether any of them were all weather enough. There's no wrong conclusion to draw, do you think they are all-weather enough?

Because the investment income earned in a Roth IRA is tax-deferred—and eventually tax-free—there are no tax complications to worry about. Unlike taxable brokerage accounts and even bank accounts, there’s no possibility of incurring the so-called “ kiddie tax ” on the investment earnings in a Roth IRA account.

An individual who learns to manage $4,000 a month after taxes will be equipped to manage $14,000 or even $40,000 a month as their earnings increase over time. Take Advantage of RetirementPlans and Matching Contributions. Employers often match a portion of this contribution to a retirementplan as an employer benefit. .

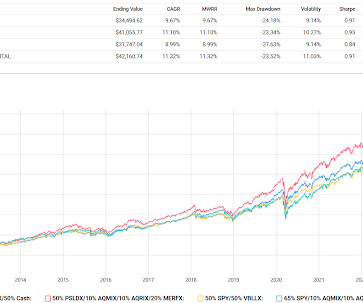

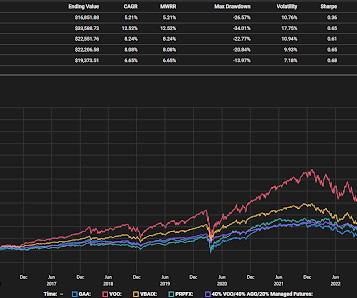

Dave Nadig found a potential tax problem in the fine print. Apparently it is not diversified enough to meet RIC, regulated investment company, standards which as Dave tells it would nullify the tax benefits associated with ETFs. In 2022 Portfolio 1 fell 6.27% versus a decline of 5.29% for PRPFX and 16.87% for VBAIX.

All three were better than VBAIX in 2022 by 150-550 basis points. Somehow, it did worse than the S&P 500 by several hundred basis points in 2022. Based on the chart, I'm guessing that SPD was positioned in such a way as to miss the bounce that started in late 2022. The results are not skewed by one year.

Generically, dividends are not tax efficient. They are taxed at ordinary income. SCHD has historically paid "qualified" dividends which are taxed more favorably as capital gains but this is something to continuously track. Derivative income funds that track indexes might be taxed 60/40, you have to check.

One complicating factor is that tax is owed annually on the amount of the par value adjustment so qualified accounts might be better for individual TIPS. That sounds good of course but in reality, being immunized isn't exactly how it played out in 2022. The worst year for all three was of course 2022.

Tax season is here! For many of us, that means a tax refund. Some general, popular advice you may have heard before, is that if you receive a tax refund, a bonus, or an unexpected financial windfall, you should invest or save it for the long-term, rather than spending it now. Immediate gratification can be hard to resist.

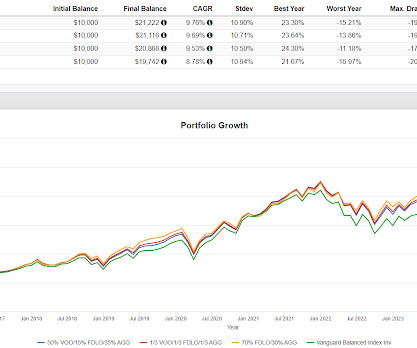

Portfolio 4 has middling stats compared to the others but in 2022 it was only down 8.23% versus 20% for Portfolio 1, 17% for Portfolio 2 and Portfolio 3 was down 22%. Also PSLDX is capable of some huge drawdowns, dropping 43% in 2022 and 33% in 2008. It also fell 37% in the 2020 Pandemic Crash but it took that back in just four months.

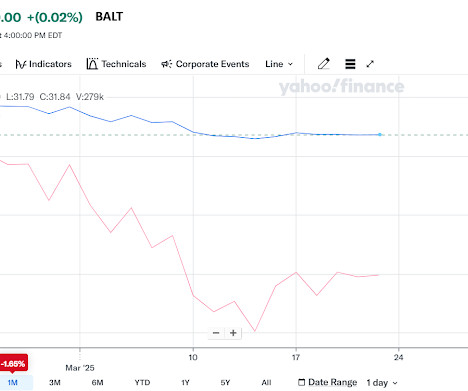

While the one traditional bond ETF was down 25% in 2022, the other four ranged from a decline of 2.51% to a gain of 2.54%. BALT has never paid out a distribution so it is tax efficient. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

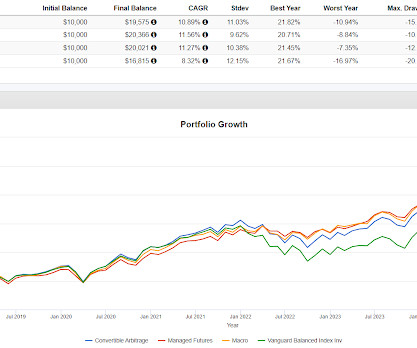

Weaving in the historical part of the essay he points out that in addition to 2022, there have been several events before 1981 where the traditional 60/40 did very poorly, he seemed to be blaming the 40 allocated to bonds. In terms of crisis alpha in rough times, convertible arb didn't really help in 2022 but managed futures and macro did.

MBXIX added the best long term result but QSPIX had the best performance in 2022. The 50/50 version did far and away the best in 2022. The leveraged version outperformed going into the 2022 bear market (that started late in 2021) but has had a tough time digging out of that hole since then. QSPIX is sort of a cherry pick.

It did go down almost 9% in the 2020 Pandemic Crash but that was just a fraction of what the S&P 500 dropped and in 2022, OCRP was up 9.15%. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Portfoliovisualizer says OCRP has a -0.09

For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs. Here are some of the most common RMD questions and planning opportunities for investors. How to take RMDs and avoid any taxes (legally of course). There are a couple ways to do it.

If we swap out AGG and replace it with TFLO which is a floating rate ETF, the CAGR goes up by 14 basis points and volatility drops by 27 basis points which are not dramatic numbers but helped meaningfully in 2022, leading to a performance improvement of 601 basis points.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content