This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

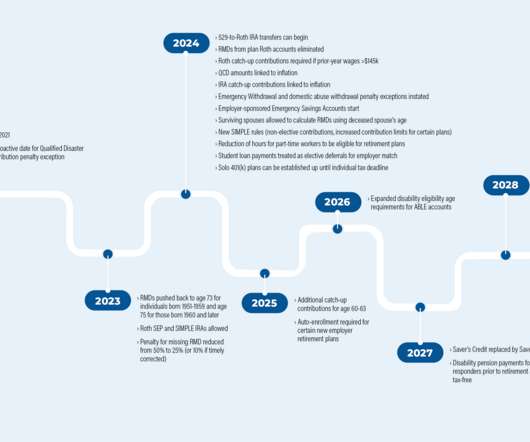

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72.

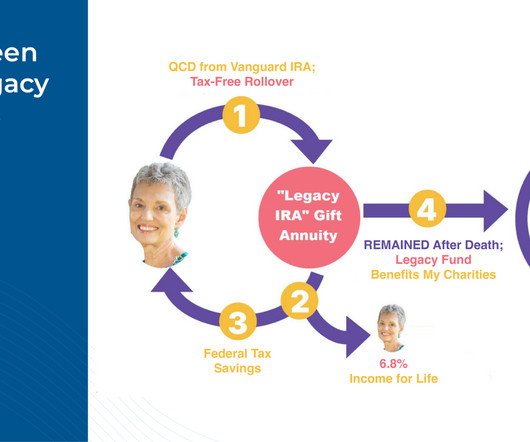

However, the caveat with current CGAs has been that they could only be funded with after-tax dollars before the donor’s death, meaning that if an individual only had tax-deferred funds (e.g., legislation at the end of 2022. But the SECURE 2.0 The potential benefits of the new Legacy IRA rules are threefold.

As dynamic as the secondary market may be, secondaries come with complex tax implications that can significantly impact returns if not properly managed. What are the tax implications of secondary transactions? What are the tax challenges in secondary transactions? What tax strategies optimize secondary investments?

Key Takeaways: Because the 2022 and 2023 standard deductions are relatively high ($27,700 in 2023 and $25,900 in 2022 for married couples filing jointly), it isn’t worthwhile for many taxpayers to itemize deductions. Tax season has begun, and it’s not too early to think about planning for the 2023 tax year.

In November 2022, proponents of the Massachusetts ‘millionaires’ tax (question 1) won their bid to nearly double the income tax rate on individuals with taxable income over $1M a year. As proposed, the new legislation would increase these tax rates to 9% and perhaps even 16% , respectively, starting in 2023.

So much occurred in 2022, and we're excited (and anxious) to see what 2023 has in store! 4 MIN READ. Another year has come and gone in what feels like a blink of an eye.

By Mike Valenti, CPA, CFP ® , Director of TaxPlanning It’s that time of year again! W-2s, 1099s and mortgage statements have been to hit your mailbox: a daily reminder that it is, once again, Tax Season. Overall, it was a relatively quiet year on the tax front. Although Congress isn’t done yet! More on that later.)

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts. Act passed in late 2022. Along with the new Finalized Regulations, the IRS also released a new set of Proposed Regulations dealing with some unanswered questions around the SECURE 2.0

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Employee matters.

Even as tax season winds down, it’s still important that you consider tax strategy as part of your financial picture. Many couples file jointly, and while it can sometimes help save on your taxes, it isn’t always the best option in each case! Determine if you can file jointly. 1] Consider your deductions and credits.

Not only was the stock market fairly volatile, but there were also atypical tax regulation changes. Tax-loss harvesting. Paying taxes on investment gains can be a financial burden, but tax loss harvesting can reduce your bill. Did you have a liquidity event in 2022? Max out your retirement contributions.

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

Podcasts Christine Benz and Jeff Ptak talk with Tim Steffen, director of taxplanning for Baird. riabiz.com) Three positives, and three negatives, from the 2022 Future Proof festival. morningstar.com) Michael Kitces and Carl Richards talk about repurposing lessons from clients for content.

Acts, what that means to you and your TaxPlanning in Retirement. also known as Securing a Strong Retirement Act of 2022 (HR2954), builds on the SECURE Act and its significant changes to retirement. Lastly, Larry will take your questions on TaxPlanning in Retirement so you can avoid unintended tax consequences in retirement.

is significant legislation signed into law on December 20, 2022, and is expected to have several impacts on retirement income planning. It contains several provisions designed to improve Americans' retirement security, including later required minimum distributions (RMDs), 529-to-Roth rollovers, and other taxplanning opportunities.

TaxPlanning: Things to work on before year-end. Though it may seem that we’ve just put last tax season to rest, now is the time to work on adjustments to optimize your 2022taxes! Don’t wait until April 15th, 2023, to think about your taxes…there are things that need to get done by year-end!

While these can be avoided, there is another cash outflow that can considerably lower your savings and returns and is also hard to avoid – tax. Taxplanning is essential. Tax is charged on every penny you earn. Tax evasion is a crime, and missing tax payments can lead to legal hassles that can be hard to get out of.

Income shifting (also known as income splitting) may be defined as dividing income in a way that lowers overall taxes. When using these methods to shift income to a child, it’s always important to bear in mind the kiddie tax. Timing the receipt of your income can also help you lower your taxes.

The rise of remote work and digital nomadism has made FEIE a common tax minimization strategy for Americans living abroad. What is the Foreign Tax Credit (FTC)? Financial and lifestyle considerations of living abroad The importance of professional tax advice for expats FAQs about the FEIE What is the Foreign Earned Income Exclusion?

Suppose they made emotional investment decisions during the market volatility of 2022. On the other hand, not having a plan can lead to emotional investment decisions during periods of high volatility – something every investor should avoid. The chart below illustrates the potential consequences of not rebalancing.

By Mike Beirne, MDRT Round the Table editor Try these ideas from the 2022 MDRT Annual Meeting speakers about referrals, communications and marketing. Both sessions aim to educate about the value and benefits of financial and taxplanning, but no selling occurs. 1) Give the referral process a push.

Tobias Financial Advisors is proud to announce that our Wealth Advisor Franklin “Franko” Gay serves on the National FPA NexGen Task Force and is one of the planners responsible for this year’s content at the 2022 FPA NexGen Gathering in Las Vegas from August 23 rd to 25 th. To learn more details, visit: [link].

For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs. Here are some of the most common RMD questions and planning opportunities for investors. How to take RMDs and avoid any taxes (legally of course). There are a couple ways to do it.

The federal income tax is levied by the U.S. It is a mandatory tax that you pay to the government every year. Evading tax is a serious legal offense punishable by law. Therefore, it is important to stay up to date with the changing tax laws, rates, and dates for filing your income tax return. Single filers.

Donating appreciated stock to charity can be a great way to give back and reduce your tax bill. Taxpayers who itemize get a tax deduction for the market value of the stock. If you want to make a gift for the 2022tax year – act now. These two steps don’t need to happen in the same tax year. Give wisely.

Considering Roth conversions in retirement When you convert pre-tax money from an IRA to an after-tax Roth IRA, the amount converted is included in your taxable income. But in retirement, without a paycheck, it can be a great opportunity to control your tax situation for the year and fill up the lower tax brackets.

[i] Private Foundation – A private foundation is created when someone sets up a tax-exempt organization but does not file to be recognized as a public charity. The tax deduction is lower at 20 percent of the taxpayer’s AGI if the gifts are appreciated assets or securities. [ii] A CRT may be partially tax-deductible right away.

In early 2022, the IRS proposed new changes, and if enacted, some inherited IRA beneficiaries will need to take RMDs again and could face big penalties. It’s probable that the IRS would waive penalties as the announcement only came in February 2022 and still isn’t law. What the IRS proposal wouldn’t change.

Implementing these strategies can help reduce tax bills, save more, and achieve financial goals sooner. The deadline for tax filing is around the corner. Besides meeting all the requirements for this date, have you considered the impact of implementing long-term tax strategies on your wealth?

If eligible, you may be able to exclude up to 100% of the gain from federal taxes when you sell your shares through the capital gains tax exclusion. The potential tax savings simply cannot be understated. Using IRS Section 1202, taxpayers can sell stock potentially free of federal capital gains taxes if the requirements are met.

Stay tuned for next week. – Andres Disclosure: This page is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accounting, tax, legal or financial advisors. The observations of industry trends should not be read as recommendations for stocks or sectors.

Stay tuned for next week. – Andres Disclosure: This page is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accounting, tax, legal or financial advisors. The observations of industry trends should not be read as recommendations for stocks or sectors.

was signed into law December 29th, 2022, bringing more major changes to tax law. 529 plan to Roth IRA rollovers. The individual must be the designated beneficiary of the 529 plan and move funds to a Roth IRA in their name. Amount rolled over is tax-free (not included in beneficiary’s income) and penalty-free.

An HSA is a tax-advantaged account that’s paired with an HDHP. An HSA offers several valuable tax benefits: You may be able to make pre-tax contributions via payroll deduction through your employer, reducing your current income tax. Contributions to your HSA, and any interest or earnings, grow tax.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. There are many components of the 2022 Act that will impact employers that aren’t outlined below. IRAs: the $1,000 catch-up limit will be indexed by inflation for tax years starting in 2024.

Last week the IRS issued IRS Notice 2022-53 related to Inherited IRA RMDs which I summarize below. Last Friday (October 7, 2022), the IRS issued IRS Notice 2022-53 which I summarize below: The IRS will not impose the 50% penalty for missed inherited IRA RMDs in 2021 and 2022 that are subject to the SECURE Act 10-year payout period.

The choice to defer is only permitted for tax year you turn 72 in, the year of your first RMD. For example, if you choose to defer your 2022 RMD until April 1, 2023, you will still need to withdraw your 2023 annual RMD by December 31, 2023). Please contact your plan administrator for more details.

Additionally, our estate planning specialist helps clients prepare for possible life scenarios and manage their money according to their wishes. Income TaxPlanning. As HNWIs have higher incomes, they also have increased taxes. However, some financial planners offer strategies to help HNWIs reduce their taxes legally.

Retirement planning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estate planning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

Yet many still have complex needs requiring more sophisticated and personalized investment, estate, and taxplanning services. million households in three key groups who want customized, actionable advice on budgeting, saving, investing, insurance, and planning to help provide peace of mind regarding their finances.

Who doesn’t love a great tax break? Why not make best use of your tax-planning powers when you do? At a glance, it would seem qualified dispositions are the way to go: Qualified dispositions: Proceeds are taxed at (usually lower) long-term capital gains rates. Fewer taxes are better, right? True enough.

Will you end up paying too much in ordinary income taxes for company stock in your 401(k) plan? With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirement planning. In contrast, the average liability is 3 percent for the top quintile, 16.4

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content