This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that according to a recent study by DeVoe & Company, only 42% of RIAs surveyed have written succession plans and either have begun to implement them or have already done so.

Which could include measures such as additional time to comply with rules that have been adopted but not yet enforced and perhaps, more broadly, an approach from the SEC that focuses more on whether a firm has robust program controls and a strong fiduciary culture rather than seeking out specific, (sometimes minor) missteps and producing enforcement (..)

Mike McGlothlin , CFP, CLU, ChFC, LUTCF, NSSA, Executive Vice President, Retirement, at Ash Brokerage , is the 2024 recipient of the Kenneth Black Jr. NAIFA and FSP merged in January 2024. Leadership Award. McGlothlin manages a staff of more than 65 employees and has maintained a 90% retention rate.

Open, honest and candid discussion about lawsuits against TIAA and Morningstar, CITs bigger than mutual funds in TDFs, private equity in retirementplans and more.

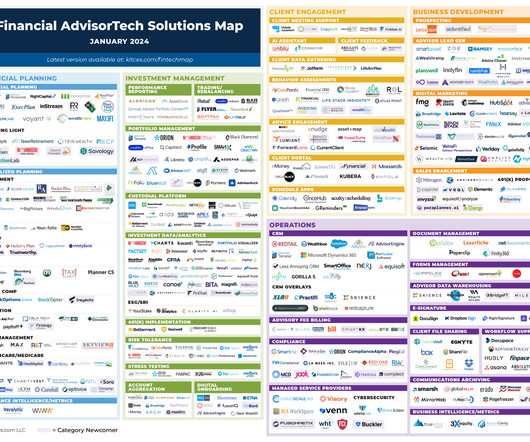

Welcome to the January 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

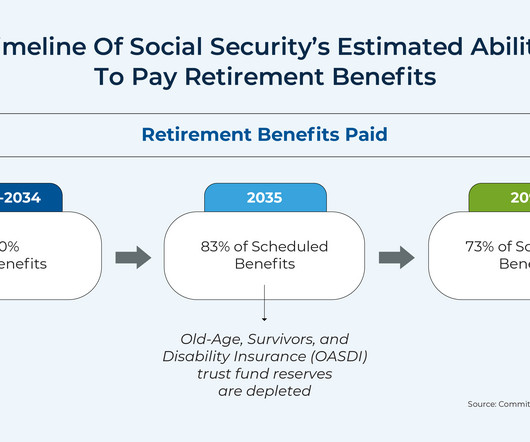

The new law repeals both the WEP and GPO, restoring full Social Security benefits to affected individuals, retroactive to January 2024. But the challenge in making such an estimate is the fact that SSA doesn't clearly show many individuals what their full benefits would be without the reduction for WEP or GPO.

Open, honest and candid discussion about the flexPATH lawsuit verdict, AI in DC plans, employee engagement, convergence and retirementplan advisor due diligence.

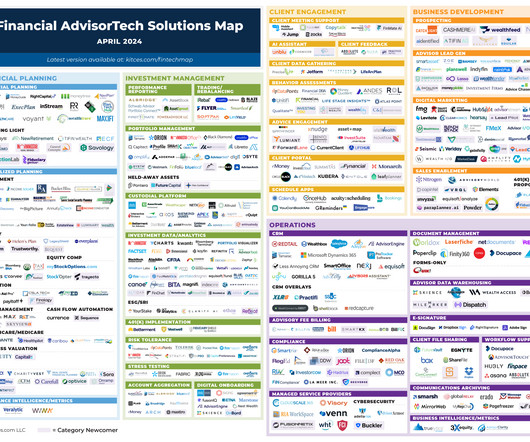

Welcome to the May 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

million Americans turning 65 in 2024, advisors are navigating four core risks that will impact their portfolios in retirement: longevity, inflation, volatility, and emotions. With nearly 4.5 We will discuss new research by Dr. Wade Pfau, professor at The American College of Financial Services.

Welcome to the October 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

Which means that financial advisors can play an important role in adoption planning – helping clients strategically plan for the costs involved in the process, including accessing tax credits that can significantly defray these expenses. At the same time, adoption can be expensive, with costs that can add up to $70,000 or more.

ft.com) Creative Planning has closed on its purchase of Goldman Sachs' ($GS) PFM unit. citywire.com) Creative Planning is expanding its reach in the retirementplan space. papers.ssrn.com) Taxes A 2023 year-end tax planning guide. kitces.com) Advisers How the profession of financial planning has changed over time.

Also in industry news this week: A House committee has advanced a bill that would extend several expired business-related tax measures from the Tax Cuts and Jobs Act and would increase the value of the Child Tax Credit The SEC released its examination priorities for 2024, which include a focus on advisers' adherence to their duty of care and duty of (..)

Updated for 2024. Unlike most types of retirementplans, the SEP IRA is funded by the employer. A SEP IRA (Simplified Employee Pension Individual Retirement Account) is a type of retirementplan specifically designed for self-employed individuals and small business owners. What is a SEP IRA?

Also in industry news this week: While the SEC has had the power to restrict mandatory arbitration clauses in RIA client agreements for more than a decade, an advisory committee meeting this week suggests support for such a measure isn't unanimous CFP Board saw a record number of exam-takers during 2024, reflecting recognition of the professional and (..)

Petersen, CPA, CFP ® , CP, Affluent Wealth Planning The holidays are upon us! That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. Lastly, I allocate the retirementplan contributions between Roth and Traditional 401(k) accounts.

The study also identified attributes of "top performing" firms across a range of metrics, finding that they are more likely than other firms to have a clear ideal client persona, client value proposition, and marketing plan.

Nevertheless, there is potential for many individual RIAs to expand their staffing further, with the addition of specialized planning and operations roles being seen as a potential avenue to boost firm growth. in 2023, the RIA space showed significantly more strength, with 10.4%

Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable. This is why having a smart, well-rounded retirementplan that includes income planning and tax planning is so important!

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more. Read More.

Do you have a plan in place for your retirement? For many people, the extent of their retirementplanning includes signing up for the plan at work – which is often more of a starting point than a comprehensive retirementplan. Some 457 plans can allow for Roth contributions and in-plan rollovers.

Because when it comes to financial planning, you’re ready to write it downand studies show that writing down your goals makes you 42% more likely to achieve them. Heres your top 10 financial planning checklist for the new year. A little planning now avoids big headaches later. Ready to Tackle 2024? Not for you.

Today’s Animal Spirits is brought to you by YCharts and Fabric: See here for 20% off your initial YCharts professional subscription Go to meetfabric.com/spirits for more information on life insurance from Fabric by Gerber Life On today’s show, we discuss: How Individual Retirement Accounts Changed the Stock Market Forever Social Security: (..)

Here are 5 areas to review to determine if you may need to make some adjustments for 2024. Review Tax Withholding: Check your paystubs to assess if adjustments to your W-4 are needed to avoid overpaying or underpaying taxes in 2024. The post Make your 2024 Taxes Less Taxing by giving yourself a Tax Checkup!

In this environment, financial advisors have the opportunity to add value for their clients not only by giving a clear explanation about the current status of Social Security and the potential legislative changes that could improve its solvency, but also by modeling what (realistic) changes would mean for their clients' financial plans.

If you’re planning to boost your retirement savings, the latest announcement from the Internal Revenue Service (IRS) brings good news. In 2024, contribution limits for most retirementplans will be increased by $500, providing individuals with additional opportunities to secure their financial future.

Strategy Contribution Limit (2024) Advantages Disadvantages Backdoor Roth IRA $7,000 ($8,000 if 50+) Circumvents income limits for Roth IRA, providing increased tax-free growth Low annual limit and pro-rata rule complications. It also requires an individuals 401(k) plan to allow after-tax contributions and in-service withdrawals.

Whether you’re decades from retirement or quickly approaching it, some of these changes will likely impact you and your financial plan. Student Loan and Roth Account Matching Employers will be able to match employees’ student loan payments to a workplace retirement account beginning in 2024. Secure Act 2.0:

But typically, it means the same thing: working in some capacity after retiring early. According to the 2024 State of RetirementPlanning Study by Fidelity Investments, the rise of remote and hybrid work has shifted retirement preferences for working Americans under age 42. But that’s short-sighted.

Some of the measures in the bill include increasing the required minimum distribution age, raising catch-up contribution limits, permitting some rollovers from 529 plans to Roth IRAs, and expanded access to employer plans. retirement changes. 529 plan to Roth IRA rollovers. 9 major Secure Act 2.0 The Secure Act 2.0

Stocks vs bonds historical returns by calendar year (1997 – 2024) Top takeaways: Between 1997 and 2024, the S&P 500 returned 9.7% Returns shown are based on calendar year returns from 1950 to 2024. Growth of $100,000 is based on annual average total returns from 1950 to 2024. on an average annualized basis.

Do you know when you want to retire? Are you saving enough for the retirement you want? Myth #2: You should plan to retire in your 60s With more people going back to school or changing careers later, holding off on retiring is becoming more common, too. for more information.

If your child is a sophomore in high school right now, this year is super important for your college funding plan! So…if your child is a sophomore in high school right now…2024 is the tax year that will be used for financial aid eligibility. Do’s Don’ts Increase pre-tax retirementplan contributions if you can.

Seals Financial Planning & Investments What does Seals do right? Engaging Queries for Common Concerns The site poses common questions such as “Will I be okay when I retire?” to engage visitors, especially those nearing retirement and seeking a financial plan. and “Will I outlive my money?”

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Stress testing a financial plan or retirement income goals is crucial to help ensure retirees wont run out of money under different conditions in the financial markets.

We are thrilled to announce that our CEO, Marian ela Collado , CPA/PFS, CFP®, CDS® will serve as one of the speakers at the upcoming CNBC Women & Wealth on March 5 th , 2024. Marianela’s session will focus on retirementplanning and how women can maximize their financial future. appeared first on www.tobiasfinancial.com.

This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. These figures can serve as a valuable reference point for individuals planning their retirement.

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older.

Individuals often use a brokerage account to save for medium to long-term goals such as college (to avoid over-funding a 529 plan), a new or second home, major asset purchase, or just because they have extra cash flow to put to work. Tax-deductible contributions means distributions in retirement are taxable as regular income.

Stocks vs. Bonds: Differences in Risk and Return Make a Case for Both While there wasn’t much that went according to plan in 2020, when we zoom out, this is a picture of a diversified portfolio performing as we might expect. The Callan Periodic Table ranks calendar year returns for various asset classes.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content