This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

Also in industry news this week: According to a recent survey, advisors are putting an increasing share of client assets into model portfolios, allowing for customization and time savings that advisors appear to be using to provide more comprehensive planning services RIA M&A deal volume saw an annual record in 2024 as a lower cost of capital, (..)

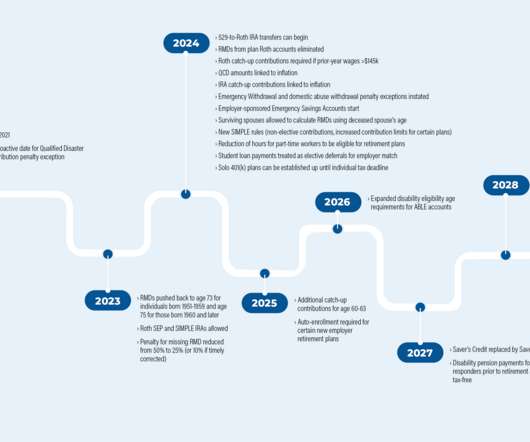

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

(citywire.com) Creative Planning is expanding its reach in the retirementplan space. papers.ssrn.com) Taxes A 2023 year-end taxplanning guide. thinkadvisor.com) The 10 best financial advisor conferences to attend in 2024. citywire.com) Choreo is buying the wealth management business of BDO USA.

Welcome to the October 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

Updated for 2024 – 2025. Because many taxpayers earn too much to make pre-tax IRA contributions as they have a 401(k) at work. Many people end up paying taxes twice. There are income limits for contributions to a traditional IRA that qualify for a tax deduction. In the vast majority of cases the answer is no.

Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy. These pillars provide a comprehensive framework for building a resilient and sustainable plan. For the tax year 2024, individuals can contribute a sum of $4,150 and families can contribute $8,300 to their HSA.

And as 2023 draws to a close, we wanted to highlight 25 of the most popular and insightful articles that were featured throughout the year (that you might have missed!). Read More.

Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable. If their income is over $44,000, up to 85% could be taxed!

As such, one of the most important retirement income resources is Social Security, which provides retirees inflation-adjusted income for life. Making the right decisions around claiming Social Security — based on your spending needs, longevity and taxplanning — could mean the difference between meeting your retirement goals or not.

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older. Timing RMDs : Begin taking RMDs by April 1 of the year after you turn 73.

IRAs: the $1,000 catch-up limit will be indexed by inflation for tax years starting in 2024. would permit employers to make matching contributions to an employee’s 401(k) and 403(b) retirementplan, even if the worker isn’t saving themselves. 529 plan to Roth IRA rollovers. The Secure Act 2.0 Other Roth changes.

Strategy Contribution Limit (2024) Advantages Disadvantages Backdoor Roth IRA $7,000 ($8,000 if 50+) Circumvents income limits for Roth IRA, providing increased tax-free growth Low annual limit and pro-rata rule complications. The key difference lies in the final destination of the after-tax contributions.

This infographic has more on how a brokerage account is taxed. Taxplanning opportunities in retirement If you only have assets in tax-deferred accounts, you may have fewer taxplanning options in retirement. See 2024 limits to determine whether you’re eligible.

Lowering the estate and gift tax limits The current exemption was raised dramatically in 2018. In 2024, a single taxpayer can claim a federal estate and lifetime gift tax exemption of $13.61 This tax benefit is scheduled to sunset at the end of 2026. Last reviewed June 2024 The post Major Tax Changes Are Coming in 2026.

Retirementplanning: Calculate retirement needs and contribute regularly to retirement accounts. TaxPlanning: Optimize tax efficiency through strategies such as retirement contributions, tax-deferred accounts, and deductions and credits. Why most of us retire earlier.”

Roth 401(k)s can only bypass annual distributions if 100% of the retirementplan was in a Roth account. If there’s a mix of pre-tax and Roth funds, RMDs will apply. As a result, taxplanning is critical, particularly if you’ve inherited a large 401(k) or IRA.

Blind spots in retirementplanning are those aspects that are often overlooked, either intentionally or subconsciously. From seemingly harmless low-interest debt to underestimating the emotional impact of transitioning out of the workforce, various factors can disrupt your peace of mind during your retirement years.

Calculate your 2023 after tax income and expected after tax2024 income. Compare this to your 2023 expenses and expected 2024 expenses. Are you saving or contributing 10-20% of your income to a dedicated savings plan? RetirementPlanning Review your retirement goals and objectives.

By working with a tax professional, you can apply tax strategies to reduce your taxable income or defer paying taxes. 20 tax reduction strategies for high-income earners in 2024Tax strategy is complex, and there are numerous ways of reducing taxable income depending on your situation.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. But there are other ways to go about taxplanning.

The ability to do 529 plan to Roth IRA rollovers goes into effect January 2024. No required minimum distributions (RMDs) in Roth 401(k) plans. Starting in 2024, individuals who left assets in a Roth employer plan won’t be subject to mandatory distributions during their life. Prior to the passing of Secure Act 2.0,

Lowering the estate and gift tax limits The current exemption was raised dramatically in 2018. In 2024, a single taxpayer can claim a federal estate and lifetime gift tax exemption of $13.61 This tax benefit is scheduled to sunset at the end of 2026. Last reviewed June 2024 The post Major Tax Changes Are Coming in 2026.

Also in industry news this week: A recent study suggests that while a majority of financial advisory clients surveyed have only had 1 advisor, deteriorating client service is a key risk factor that could sway certain clients to leave for a different advisor RIA M&A activity in 2024 is poised to surpass the total number of deals seen in 2023, according (..)

Calculate your 2024 after tax income and expected after tax 2025 income. Compare this to your 2024 expenses and expected 2025 expenses. Are you saving or contributing 10-20% of your income to a dedicated savings plan? 2024 was a great year for risk assets. Are you on track to retire when you want to?

Whether its taxplanning, practice management, or technology trends, Michael remains a go-to resource for cutting-edge knowledge. Samantha was also a finalist in the 2024 Wealthies. ( His workshops, PBS specials, and books help financial professionals master tax-efficient strategies for their clients.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content