This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

Also in industry news this week: According to a recent survey, advisors are putting an increasing share of client assets into model portfolios, allowing for customization and time savings that advisors appear to be using to provide more comprehensive planning services RIA M&A deal volume saw an annual record in 2024 as a lower cost of capital, (..)

Which could include measures such as additional time to comply with rules that have been adopted but not yet enforced and perhaps, more broadly, an approach from the SEC that focuses more on whether a firm has robust program controls and a strong fiduciary culture rather than seeking out specific, (sometimes minor) missteps and producing enforcement (..)

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. How much should I be saving?

Mike McGlothlin , CFP, CLU, ChFC, LUTCF, NSSA, Executive Vice President, Retirement, at Ash Brokerage , is the 2024 recipient of the Kenneth Black Jr. NAIFA and FSP merged in January 2024. Leadership Award. McGlothlin manages a staff of more than 65 employees and has maintained a 90% retention rate.

The new law repeals both the WEP and GPO, restoring full Social Security benefits to affected individuals, retroactive to January 2024. To help with this, we've developed a downloadable calculator that simplifies the process of estimating an individual's unreduced Social Security benefits, whether or not a full earnings history is available.

Open, honest and candid discussion about lawsuits against TIAA and Morningstar, CITs bigger than mutual funds in TDFs, private equity in retirementplans and more.

Open, honest and candid discussion about the flexPATH lawsuit verdict, AI in DC plans, employee engagement, convergence and retirementplan advisor due diligence.

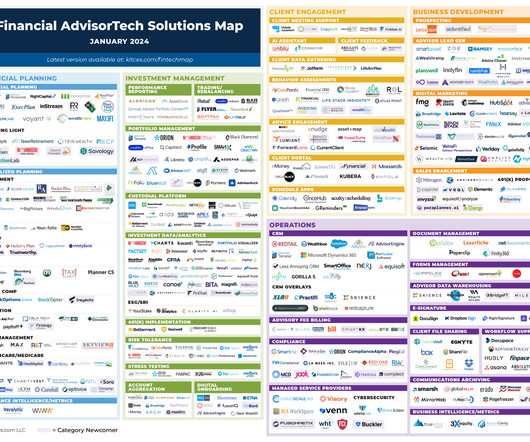

Welcome to the January 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

million Americans turning 65 in 2024, advisors are navigating four core risks that will impact their portfolios in retirement: longevity, inflation, volatility, and emotions. With nearly 4.5 We will discuss new research by Dr. Wade Pfau, professor at The American College of Financial Services.

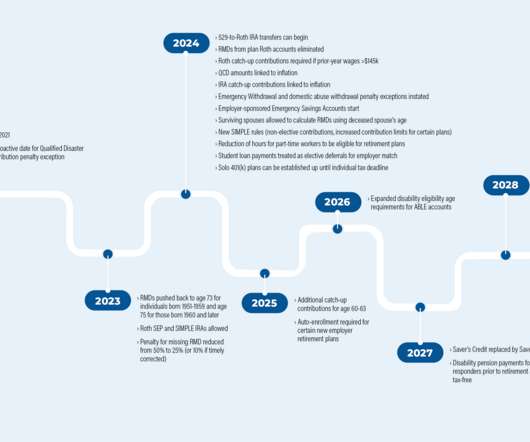

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirementplanning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. In addition, SECURE 2.0

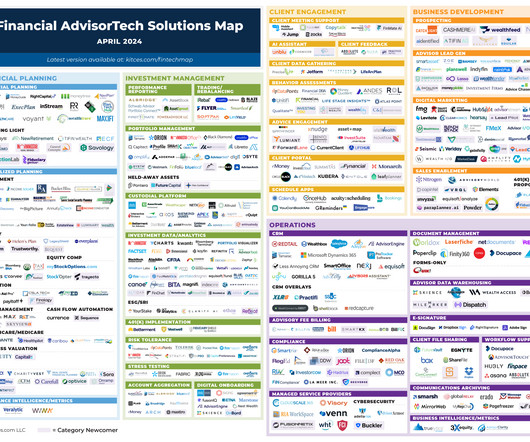

Welcome to the May 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

Also in industry news this week: A House committee has advanced a bill that would extend several expired business-related tax measures from the Tax Cuts and Jobs Act and would increase the value of the Child Tax Credit The SEC released its examination priorities for 2024, which include a focus on advisers' adherence to their duty of care and duty of (..)

Updated for 2024 – 2025. Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Investors often ask: should I be making nondeductible IRA contributions? Why non-deductible?

Achieving financial freedom in retirement requires meticulous planning, dedicated effort, and strategic management. Without a solid plan, you risk drifting without direction. Within this framework, the concept of the five pillars of retirementplanning emerges as a valuable strategy.

The original SECURE Act, signed into law in December 2019, changed many of the long-standing rules governing IRAs and other retirement accounts, and no single measure in the legislation had a more seismic impact on planning than the changes to the post-death distribution rules for retirement accounts.

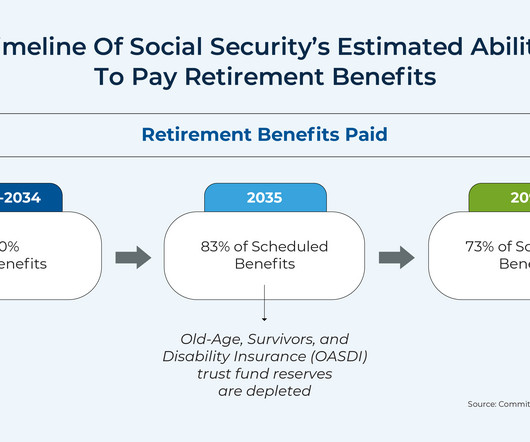

on up to $168,600 of income in 2024 for the Social Security portion of FICA). raising the payroll tax wage cap or increasing the Full Retirement Age) that would close the funding gap. Such options include single-policy solutions that would wipe out the entire 75-year shortfall (e.g., the board of trustees report estimates that a 3.33

Also in industry news this week: While the SEC has had the power to restrict mandatory arbitration clauses in RIA client agreements for more than a decade, an advisory committee meeting this week suggests support for such a measure isn't unanimous CFP Board saw a record number of exam-takers during 2024, reflecting recognition of the professional and (..)

Updated for 2024. Unlike most types of retirementplans, the SEP IRA is funded by the employer. A SEP IRA (Simplified Employee Pension Individual Retirement Account) is a type of retirementplan specifically designed for self-employed individuals and small business owners. What is a SEP IRA?

Welcome to the October 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

Eligible IRA owners age 70 ½ and older can make up to $105k in tax-free charitable donations during 2024 through qualified charitable donations (QCDs). The annual exclusion for gifts increases to $19,000 for the calendar year 2025, up from $18,000 from 2024. The standard mileage rates for 2024 is $0.67

ft.com) Creative Planning has closed on its purchase of Goldman Sachs' ($GS) PFM unit. citywire.com) Creative Planning is expanding its reach in the retirementplan space. thinkadvisor.com) The 10 best financial advisor conferences to attend in 2024. riaintel.com) How to prep an RIA for sale. kitces.com)

The study also identified attributes of "top performing" firms across a range of metrics, finding that they are more likely than other firms to have a clear ideal client persona, client value proposition, and marketing plan.

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. You may need more money than you think to retire on dividends. Retire on dividends?

Also in industry news this week: While the total number of RIA M&A deals in 2023 fell short of a record-setting 2022 amidst an elevated interest rate environment, continued interest from private equity firms and creative deal structures could boost deal flow in 2024 While the SEC authorized 11 "Spot" Bitcoin ETFs last week, comments from chair (..)

Also in industry news this week: The Office of Management and Budget (OMB) has completed its review of the Department of Labor's new "fiduciary rule ", indicating that it could be released in the coming days or weeks (though, like its predecessors, its ultimate disposition is likely to be determined in the courts) The IRS announced this week that it (..)

It goes by many different names: semi-retirement, partial or phased retirement, second career, and so on. But typically, it means the same thing: working in some capacity after retiring early. As more workers consider the growing appeal of semi-retirement, some ask — is working part-time in retirement a good idea?

Do you have a plan in place for your retirement? For many people, the extent of their retirementplanning includes signing up for the plan at work – which is often more of a starting point than a comprehensive retirementplan. Some 457 plans can allow for Roth contributions and in-plan rollovers.

Today’s Animal Spirits is brought to you by YCharts and Fabric: See here for 20% off your initial YCharts professional subscription Go to meetfabric.com/spirits for more information on life insurance from Fabric by Gerber Life On today’s show, we discuss: How Individual Retirement Accounts Changed the Stock Market Forever Social Security: (..)

Early retirement has become a popular financial goal. Even if you never retire early, just knowing that you can is liberating! Can You Really Retire at 50? Can You Really Retire at 50? Table of Contents Can You Really Retire at 50? FAQs on Retiring Early at 50 It’s a big bold claim – retire at 50?

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033.

Planning has changed a lot since the Tax Cuts and Jobs Act nearly doubled the minimum standard deduction to $14,600 for single filers and $29,200 for married-filing-jointly (for 2024). There Are Still Ways to Help Optimize Your Taxes Its important to remember that were still in the tax planning season.

For instance, the Federal Adoption Credit provides a nonrefundable credit of up to $15,950 per child for adoptions in 2023 (claimed on 2024 tax returns), with no limit on the number of adopted children to whom this credit can apply.

by Jake Anderson, Paraplanner Retirement accounts like 401(k)s and IRAs allow individuals to save for their future in a tax advantaged manner. So, let’s say you contribute money to a traditional 401(k) plan in your 20s. This gives you ample time to grow your savings and investments for retirement.

Many states also exempt retirement income, which may include Social Security. However, retirement income is generally included for income related monthly adjustment amount (IRMAA) computations to determine if supplemental payments are due for Medicare Part B and Medicare Part D premiums.

1 With ever-increasing life expectancies, it’s no wonder 63% of American adults say they’re more afraid of running out of money in retirement than they are of death. 2 That’s why it’s vitally important to consider longevity risk when you’re planning for your financial needs in retirement. What Is Longevity Risk?

And as 2023 draws to a close, we wanted to highlight 25 of the most popular and insightful articles that were featured throughout the year (that you might have missed!). Read More.

Act has passed, making it the largest retirement legislation since the original Secure Act hit in the late 2019. As 55% of Americans say they don’t have enough saved for retirement, this bipartisan legislation primarily seeks to make it easier to contribute to retirementplans and use those funds appropriately for their needs in retirement.

Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable. This is why having a smart, well-rounded retirementplan that includes income planning and tax planning is so important!

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content