This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. You may need more money than you think to retire on dividends. Retire on dividends?

In the competitive financial industry, staying ahead means mastering client engagement and refining marketing strategies. Marketing for financialadvisors in 2025 will require a sharp focus on effective communication, personalized client experiences, and smart use of technology. Clarify your objectives.

Which is surprising to some, given that a decade ago, the emergence of so-called "robo-advisors" was supposed to displace human financialadvisors and compress advisory fees. In reality, though, the robos struggled to gain traction, and the human financial advice business just continues to grow.

When it comes to advising clients on student loan issues, many financialadvisors might first think about recent graduates seeking advice regarding the most effective way to pay down their balances.

What Do FinancialAdvisors Do? Published: March 21st, 2025 Reading Time: 6 minutes Written by: The Zoe Team Managing wealth involves more than just investingit requires careful planning, strategic decision-making, and a long-term vision. What Does a FinancialAdvisor Do? Optimizing tax-efficient retirement income.

Additionally, we have news that FinCEN has announced an extension of the BOI reporting deadline and a temporary halt in enforcement, an analysis on the implications of wealth taxes in Europe, and a refresher on how the new ‘Savers Match’ program aimed at enhancing the retirement savings of millennials and Gen Z functions.

Every year brings changes in tax rules, and 2025 is no exception. Whether you are saving for retirement, running a business, or planning for your family’s future, these updates could affect your financial decisions throughout the year. These 2025 updates provide fresh chances to protect and grow your wealth.

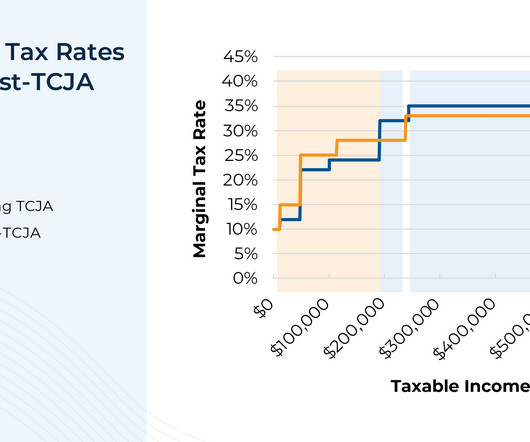

However, most of TCJA's provisions are set to 'sunset' at the end of 2025 – an event that would have at least as much impact as TCJA's initial passage. And yet, the timing of the sunset provision at the end of 2025 means that the actual fate of TCJA will largely hinge on the uncertain outcome of the 2024 U.S.

New Year, New Wealth: A Guide to Financial Resolutions for 2025 Updated December 30th, 2024 Reading Time: 7 minutes Written by: The Zoe Team As the New Year approaches, many of us set personal goals to make the coming year better than the last. Boost Retirement Contributions Maximize contributions to your retirement accounts.

April 15 marks the IRS tax return filing deadline for 2025. These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. Individual Retirement Accounts (IRAs): Contribute up to $7,000 for 2024 ($8,000 if aged 50+). Available to taxpayers aged 70.5

Also in industry news this week: 43% of wealth management firms are frustrated with the effectiveness of their CRM software, spurred on by challenges with integrations and workflows, according to a recent survey The Social Security Administration this week announced a 2.5%

5 Proven Marketing Strategies for FinancialAdvisors to Boost Client Acquisition In her classic hit song Nothing Can Come Between Us, Sade was right when she sang, Its about trust. The number-one objective financialadvisors must have in their online marketing efforts is to build TRUST with their audience.

In contrast, the typical (median) household is far more concentrated in home equity and retirement savings, with limited exposure to stocks or private business ownership. Find Your Wealth Advisor at Harness At Harness , our wealth and financialadvisors can guide you through major life stages and investment decisions.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. GET STARTED 1. For those over 50, the limit is $8,000.

Client events are evolving in 2025, offering unparalleled opportunities to connect with clients, strengthen relationships, and drive quality leads. Why a Client Event is a Must-Have in 2025 The landscape of client engagement is more dynamic than ever, and client events have become an essential part of building long-lasting relationships.

Client events are evolving in 2025, offering unparalleled opportunities to connect with clients, strengthen relationships, and drive quality leads. Why a Client Event is a Must-Have in 2025 The landscape of client engagement is more dynamic than ever, and client events have become an essential part of building long-lasting relationships.

Act, signed into law December 29, 2022, is designed to help strengthen the retirement system and Americans’ preparedness for retirement. The act introduces 92 provisions that will impact your clients and their financial plans, whether they’re in, nearing, or still years away from retirement. The SECURE 2.0

What Do FinancialAdvisors Do? Published: March 21st, 2025 Reading Time: 6 minutes Written by: The Zoe Team Managing wealth involves more than just investingit requires careful planning, strategic decision-making, and a long-term vision. What Does a FinancialAdvisor Do? Optimizing tax-efficient retirement income.

While an investor’s timeline affects their risk tolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be. Retirement planning, like any type of robust financial planning, should include stress testing your investment strategy and financial plan.

When rates are low, corporations often retire high-cost debt in favor of issuing new bonds at a lower rate and a longer duration to lock in favorable rates. However, to reach your long term financial goals, your investment strategy likely needs a mix of both. How Bonds Work How Do Interest Rates Affect Bonds?

I am a CFA® charterholder and financialadvisor marketing consultant. I have a newsletter in which I talk about financialadvisor lead generation topics which is best described as “fun and irreverent.” They’re not going to like me if I go out there and say I’m a financialadvisor for dentists.”

The Five Phases of Retirement Planning Published January 29, 2025 Reading Time: 2 minutes Written by: The Zoe Team Retirement is a journey with distinct phases, each requiring its own focus and preparation. Understanding these phases can help you approach your financial future with clarity and confidence.

Are FinancialAdvisors Lazy To Recommend Active ETFs ? It was a thin article that came down to advisors knowing their limitations which is of course useful for anyone in any of their endeavors. Also noted was what the world looked like 30 years ago when the author worked as an advisor.

million for tax year 2025, but rates for amounts above that threshold range up to 40%. Put aside assets in a tax-advantaged retirement account like a Roth IRA, if eligible, where they can grow tax-free. Your tax or financialadvisor can help you determine the best strategies for your situation.

In a recent FinancialAdvisor article, our Senior Wealth Advisor, Matt Saneholtz , CFA, CFP®, EA, was quoted on the implications of the Medicare industry upheaval during the upcoming open enrollment period. He shared his insights on the matter, discussing why Medigap may be a good option despite their high premiums.

A Roth IRA is a type of investment account that lets you invest after-tax dollars for retirement. From there, your money can grow tax-free, and you can withdraw your funds without having to pay income taxes once you reach retirement age. It is also recommended to consult with a financialadvisor for personalized advice.

Is Your Financial Confidence Holding You Back? Published: March 20th, 2025 Reading Time: 6 minutes Written by: The Zoe Team Have you ever stood in a grocery aisle, staring at a wall of options, unable to pick one? Retirement Planning (22%): Fear of running out of money or not saving enough. Find your financialadvisor matches.

Is Your Financial Confidence Holding You Back? Published: March 20th, 2025 Reading Time: 6 minutes Written by: The Zoe Team Have you ever stood in a grocery aisle, staring at a wall of options, unable to pick one? Retirement Planning (22%): Fear of running out of money or not saving enough. Find your financialadvisor matches.

Financialadvisors like you need more than traditional methods to get seen online. Building effective marketing assets, like videos, guides, and case studies, is essential for advisors looking to attract and convert prospects. Are you aiming to reach established business owners focused on retirement planning?

This is compared to short-term capital gains rates, which mirror your ordinary income tax rate, up to 37% in 2025. For 2025, the threshold is $200,000 for single filers and $250,000 for joint filers. retirement or financial independence) often makes sense.

Published: April 9th, 2025 Reading Time: 7 minutes Written by: Keith Corbett, CFP Equity compensation is a type of non-cash benefit that some employers offer employees as part of their total compensation package. Proactive planning with a financialadvisor can help employees make informed decisions and minimize tax liability.

While the market remains strong, how does this news affect the savings of retirees or those about to retire? . So, how do people who are retired or about to retire combat this inflation? But for someone retired or nearing retirement, this strategy could be fatal to their portfolio. .

Also, if you’re a business owner , you’ll also need more in savings.Take a look at your entire financial situation, or work with a fee-only financialadvisor to determine exactly how much savings you should have. That’s often the difference between having enough money to retire, and not.

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financialadvisors including topics covering technical planning, practice management, advisor marketing, career development, and more. Read More.

Alternatively, you may want to exercise and sell ISOs if you have a financial goal you want to fund, such as retirement, a second home, or a college expense. The after-tax proceeds can be used to fund your goals, objectives, retirement, or whatever is most important to you. Incentive Stock Options at Expiration.

Updated for 2024 – 2025. Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Investors often ask: should I be making nondeductible IRA contributions? Why non-deductible?

The updated tax code went into effect in 2018 and will “ sunset ” in 2025. This strategy can be especially impactful during a donor’s highest earning years, often within a few years of retirement. Let us connect you with the most qualified wealth planners Find My Advisor Ready to Grow Your Wealth? Ready to Grow Your Wealth?

While the final submitted text has not been released, some experts suggest that the DoL likely made few changes to its initial proposal, despite significant opposition from broker-dealers that could lead to the judicial system deciding the rule’s ultimate fate.

Qualified Charitable Distributions (QCDs) Your distributions from your retirement plans are reported on your 1099-R form , but the form doesnt specify how much went to a QCD. We can also start putting practices in place for 2025 to plan ahead. Remember: These are only a few of the tips and details to keep in mind.

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts. As a whole, these regulations introduce significantly more complexity to the process of tax planning around retirement accounts, particularly after the death of the account's original owner.

And suddenly every broker, every financialadvisor where they were operating through Merrill Lynch or Schwab could sell those funds and indexing was available to, all prior to that, there were a lot of brokers who would never have sold an index fund because they didn’t have access to Vanguard’s platform.

by Jake Anderson, Paraplanner Retirement accounts like 401(k)s and IRAs allow individuals to save for their future in a tax advantaged manner. This gives you ample time to grow your savings and investments for retirement. IRAs and 401(k)s are primarily designed to help fund retirement not pass wealth onto future generations.

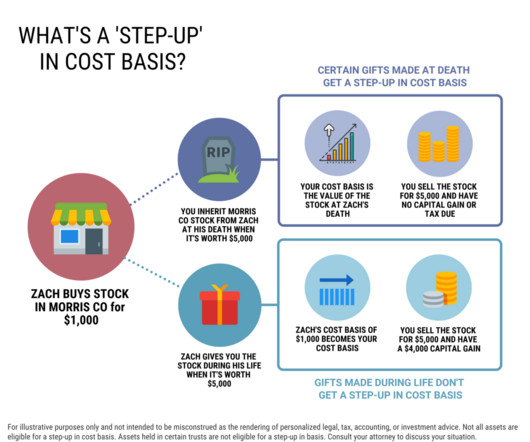

Non-retirement assets like stocks in a brokerage account, inherited home , antiques/art/collectables, or other real estate, are generally eligible for a step-up in cost basis. Retirement accounts and IRAs do not receive a stepped up basis. It’s also worth noting that the step-up in basis doesn’t just happen automatically.

If you’ve just inherited a retirement account like an IRA or 401(k) from a parent, sibling, or relative, you may be unsure about what your options are and what to do next. Most non-spouse beneficiaries inheriting an IRA, 401(k), or retirement account from the original account owner must take the money in 10 years.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content