This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that according to a recent study by DeVoe & Company, only 42% of RIAs surveyed have written succession plans and either have begun to implement them or have already done so.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. For those over 50, the limit is $30,500.

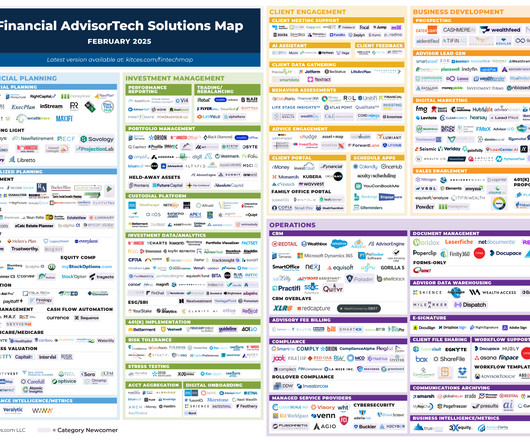

Welcome to the February 2025 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

The IRS released the 2025 401(k), 403(b), and SEP IRA contribution limits, including a new special catch-up contribution for workers age 60 to 63. The IRA and Roth IRA contribution limits are unchanged but income eligibility for tax-deductible IRA contributions and Roth IRA contributions have changed.

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

In the absence of Congressional action, multiple provisions of the Tax Cut and Jobs Act (TCJA) will expire at the end of 2025, and tax rules will revert to what they were before the legislation. The TCJA reduced specific tax brackets and increased the standard deduction.

Advisors who can help their clients with taxplanning strategies to take advantage of PTETs – starting with determining when it’s really worthwhile to do so – can provide significant value given the complexity of the decision.

Every year brings changes in tax rules, and 2025 is no exception. Whether you are saving for retirement, running a business, or planning for your family’s future, these updates could affect your financial decisions throughout the year. Think of it as the tax system’s way of protecting your purchasing power.

As is traditional, the 2025 IRS tax filing deadline is April 15th. In this guide, well explore the 2025tax extension process, the reasons for requesting an extension, and how a tax advisor from Harness can help you. Table of Contents What is a tax extension? Why do I need a tax extension?

Updated for 2024 – 2025. Because many taxpayers earn too much to make pre-tax IRA contributions as they have a 401(k) at work. Many people end up paying taxes twice. There are income limits for contributions to a traditional IRA that qualify for a tax deduction. In the vast majority of cases the answer is no.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

Notably, while the rule will create an additional compliance burden, the due diligence advisers offering comprehensive planning services (as well as their investment custodians) are likely already conducting on their clients to create an effective financial plan could be a 'defense mechanism' for these firms against criminals looking to take advantage (..)

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Tax season has begun, and it’s not too early to think about planning for the 2023 tax year. These contributions are made with pretax money, lowering the client’s overall tax bill for the year.

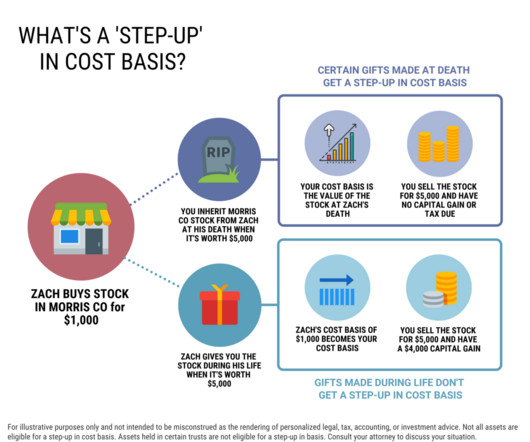

This can get very tricky so it’s important to work with the estate planning attorney settling the estate. In another words, even a survivor without prior ownership in the inherited property could sell without paying a dollar in capital gains tax. Explaining the double step-up Yes, depending on how your estate plan is structured.

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. Let’s take a look at the tax impact and other considerations of each. million before triggering federal estate taxes).

For 2025taxplanning, our Bill Cass shares income taxplanning strategies that can help manage current tax bills and prepare for future changes. Here are the highlights.

As a whole, these regulations introduce significantly more complexity to the process of taxplanning around retirement accounts, particularly after the death of the account's original owner.

Also, like most UHNW individuals, you may have income from several sources like investments, real estate, and business interests that may require special taxplanning. And if your assets span multiple countries, you may need to address international tax issues as well. Estate taxes also offer challenges.

Note, you actually have until Tax Day of 2023 to make these contributions into IRAs but you should act ASAP to avoid forever forgoing the chance to make a 2022 contribution. Contributions can be deducted from taxable income and withdrawals can be made tax-free from these accounts as long as funds are used for qualifying healthcare expenses.

Want to plan better for next years tax return ? Learn about smart taxplanning in our Winning in 2025: Tax Strategies for a Thriving Year webinar , now available for viewing on-demand. The post Winning in 2025: Tax Strategies for a Thriving Year appeared first on Carson Wealth.

It’s a simple, human act – one that seems like it shouldn’t take too much planning to do it correctly. But when does gifting become a tax issue? What do you need to consider about gifting as it relates to your overall estate plan? Taxes on Giving??? Why do you have to pay taxes on money you’re giving away?

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. The TCJA has many provisions that are set to expire (sunset) at the end of 2025. In addition, the SALT cap, currently $10,000 per tax return (not per person) will be eliminated.

In this guest post, Harness Tax Advisory Council member, Griffin Bridgers, J.D., covers some of the top estate planning trends that tax advisors should be tracking during the second half of 2024. contained a number of changes relevant to estate planning. However, awareness is key, both for clients and advisors.

Schedule a strategy session with us today, and lets discuss how we can tailor a marketing plan that fits your goals and maximizes your results. Lets make your 2025 marketing strategy one that delivers big results with small, intentional actions. Ready to take the next step? Blogging can make you 13x more likely to achieve positive ROI.

Key Takeaways: T ax Season Start: The IRS will likely begin accepting 2024 tax returns between January 15 and 31, 2025. Key Deadlines: The federal tax filing deadline (Tax Day) is April 15, 2025, with an extension deadline of October 15, 2025. Document Deadlines: Most key tax forms (W-2, 1099, etc.)

Some of the measures in the bill include increasing the required minimum distribution age, raising catch-up contribution limits, permitting some rollovers from 529 plans to Roth IRAs, and expanded access to employer plans. 529 plan to Roth IRA rollovers. 9 major Secure Act 2.0 retirement changes. The Secure Act 2.0

Financial and lifestyle considerations of living abroad The importance of professional tax advice for expats FAQs about the FEIE What is the Foreign Earned Income Exclusion? federal income tax (2025). taxes as foreign-earned income could be subject to double taxation. expatriates to reduce their tax liabilities.

2021 Year-End Planning Letter. Without downplaying the importance of appropriate action around year-end taxplanning, our purpose in this letter is to encourage clients to step back, take a breath and consider using this time to focus on the long term. Fri, 11/05/2021 - 13:01. The end of 2021 is notable for a host of reasons.

Significant changes are on the horizon with the upcoming sunset of the Tax Cuts and Jobs Act (TCJA) at the end of 2025. Income Tax Changes Understand the specific changes in income tax rates and deductions. Estate and Gift Tax Changes Learn about the implications for estate and gift taxplanning.

That said, for tax purposes, taking a large lump sum in year 10 should generally be avoided. More planning strategies and tax implications below. Roth 401(k)s can only bypass annual distributions if 100% of the retirement plan was in a Roth account. If there’s a mix of pre-tax and Roth funds, RMDs will apply.

This article covers a comprehensive list of the most common forms, documents, and information needed to file taxes. If you need a cheat sheet, download our 1-page tax prep checklist. To plan your tax timeline, see our article, 2025Tax Deadline Information for Individual Filers.

Estate planning is a critical component of a comprehensive financial plan. Furthermore, estate planning includes aspects such as tax minimization strategies, asset protection, and charitable giving. There are many different types of trusts, each designed to address specific estate planning needs.

Net Investment Income Tax (NIIT): Investors earning passive income from hedge funds may be subject to an additional 3.8% What Are the Tax Strategies for Alternative Investments? Tax-efficient investing in alternative assets requires proactive planning to minimize tax liabilities and maximize after-tax returns.

Most recently, Intel announced layoffs impacting 15% of the workforce with a plan to cut $10 billion in total costs. So, if you separate from the company near the end of the year, earning a full year of salary plus severance payouts, you could be pushed into a higher tax bracket. Taxplanning for a transition out of Intel is critical.

529 plan to Roth IRA rollovers. To help alleviate parents’ fears about over-funding 529 college savings accounts , the Act enables penalty-free rollovers from 529 college savings plans to Roth IRAs, with limitations: The lifetime rollover limit is $35,000. So it’s clear there may be some new planning opportunities on the horizon.

The Long Game: Roth Conversions & Legacy Planning ajackson Thu, 08/01/2019 - 14:51 Legacy planning is all about transferring wealth to descendants as efficiently as possible. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

The Long Game: Roth Conversions & Legacy Planning. Legacy planning is all about transferring wealth to descendants as efficiently as possible. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways. Thu, 08/01/2019 - 14:51. Background.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. The TCJA has many provisions that are set to expire (sunset) at the end of 2025. In addition, the SALT cap, currently $10,000 per tax return (not per person) will be eliminated.

Just say, “ I was researching this company and I know that taxes have just onge up in the local area. I just wanted to come in and do a seminar about how to do taxplanning in XYZ County. Treat everyone associated with the prospect as a valuable source of information.

Federal income tax withholding is generally required at the time of exercise. If the spread is under $1M, the federal statutory withholding rate is 22%, if above, its 37% through 2025. State income tax withholding may be required and payroll taxes (Social Security and Medicare) can apply.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content