This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: According to a recent survey, advisors are putting an increasing share of client assets into model portfolios, allowing for customization and time savings that advisors appear to be using to provide more comprehensive planning services RIA M&A deal volume saw an annual record in 2024 as a lower cost of capital, (..)

Advisor Today Guest Column January of 2025 is the 50th anniversary to one of the most important pieces of legislation in the retirementplanning arena ever put into law by Congress. What Im referring to is the enactment of ERISA, the Employee Retirement Income Security Act.

Notably, estimating benefits in this way isn't a simple 'back-of-the-envelope' calculation, given the complexity of the rules determining the calculation of Social Security retirement, spousal, and survivor benefits.

Heres your top 10 financial planning checklist for the new year. Write Down Your 10 Financial Goals for 2025! Maximize Retirement Contributions Contribute as much as possible to your 401(k), IRA, or Roth IRA. For 2025, the IRS has increased contribution limitsdont miss out. Happy Planning and best to you in 2025!

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. You may need more money than you think to retire on dividends. Retire on dividends?

Mike McGlothlin , CFP, CLU, ChFC, LUTCF, NSSA, Executive Vice President, Retirement, at Ash Brokerage , is the 2024 recipient of the Kenneth Black Jr. NAIFA and our FSP community congratulate Mike McGlothlin as the 2025 winner of the Ken Black Leadership Award, said NAIFA CEO Kevin Mayeux , CAE. Leadership Award.

Additionally, we have news that FinCEN has announced an extension of the BOI reporting deadline and a temporary halt in enforcement, an analysis on the implications of wealth taxes in Europe, and a refresher on how the new ‘Savers Match’ program aimed at enhancing the retirement savings of millennials and Gen Z functions.

April 15 marks the IRS tax return filing deadline for 2025. These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older.

Early retirement has become a popular financial goal. Even if you never retire early, just knowing that you can is liberating! Can You Really Retire at 50? Can You Really Retire at 50? Table of Contents Can You Really Retire at 50? FAQs on Retiring Early at 50 It’s a big bold claim – retire at 50?

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033. Stay tuned.

The Five Phases of RetirementPlanning Published January 29, 2025 Reading Time: 2 minutes Written by: The Zoe Team Retirement is a journey with distinct phases, each requiring its own focus and preparation. The Transition Phase Approaching retirement brings the need for a shift in priorities.

Client events are evolving in 2025, offering unparalleled opportunities to connect with clients, strengthen relationships, and drive quality leads. In this guide, well walk you through actionable strategies, creative ideas, and promotion tips to ensure every event you plan is a success. It’s a win-win for you and the experts.

Client events are evolving in 2025, offering unparalleled opportunities to connect with clients, strengthen relationships, and drive quality leads. In this guide, well walk you through actionable strategies, creative ideas, and promotion tips to ensure every event you plan is a success. It’s a win-win for you and the experts.

Many states also exempt retirement income, which may include Social Security. However, retirement income is generally included for income related monthly adjustment amount (IRMAA) computations to determine if supplemental payments are due for Medicare Part B and Medicare Part D premiums.

The growth in US retirement assets offers potential opportunities for retirementplan advisors to likewise expand their business. Our Mike Dullaghan discusses growth opportunities in the retirement market and how to enhance client engagement.

As you would expect from an outstanding organization like Microsoft, it offers a very robust 401(k) to help employees save for retirement. This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! )

which brings several changes to the retirement system, is now law. Whether you’re decades from retirement or quickly approaching it, some of these changes will likely impact you and your financial plan. Before this change, matches on employer plans were pre-tax. The Secure Act 2.0, Secure Act 2.0: Secure Act 2.0:

In 2025, SECURE 2.0 introduces mandatory automatic enrollment in new retirementplans, increased catch-up limits for certain workers, and reduced participation requirements for long-term part-time workers. Our Mike Dullaghan highlights the details of the new provisions.

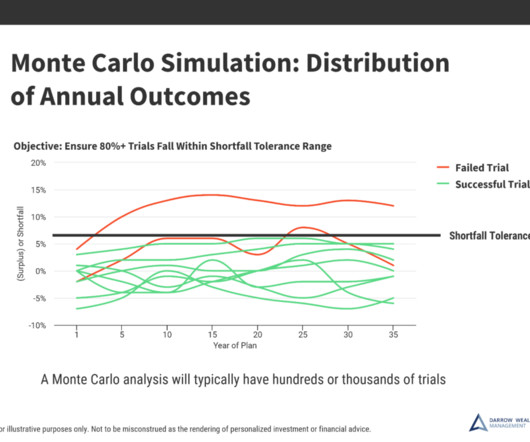

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Stress testing a financial plan or retirement income goals is crucial to help ensure retirees wont run out of money under different conditions in the financial markets.

Published: March 21st, 2025 Reading Time: 6 minutes Written by: The Zoe Team Managing wealth involves more than just investingit requires careful planning, strategic decision-making, and a long-term vision. Estate Planning : Ensuring your wealth is passed on according to your wishes. Optimizing tax-efficient retirement income.

When rates are low, corporations often retire high-cost debt in favor of issuing new bonds at a lower rate and a longer duration to lock in favorable rates. Retirementplanning, like any type of robust financial planning, should include stress testing your investment strategy and financial plan.

While an investor’s timeline affects their risk tolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be. Retirementplanning, like any type of robust financial planning, should include stress testing your investment strategy and financial plan.

Harnessing Tax-Advantaged Savings Retirement accounts and health savings plans offer the dual benefits of saving tax and building wealth. Resources & People Mentioned The Retirement Podcast Network Goals of Tax Planning Blog Should | Roll My IRA into My 401K to Do a Backdoor Roth?

legislation, all new retirement savings plans will automatically enroll workers beginning in 2025, unless they opt out, and gradually increasing their savings rates as the years roll on. After all, investments are customized to the individual, and retirementplans should be personalized as well, Benartzi posits.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement. One option is to contribute to a Roth IRA.

The tradeoff is that it usually goes down more when the market goes down including so far in 2025. Pivot to an article in Barron's about hybrid target date funds offered in 401k plans where upon retirement (minimum age might be 65), some or all of the balance can be converted into an annuity.

Doug Massey has 40 years of experience in the financial industry, specializing in retirementplanning and life insurance. As NAIFA's President-Elect for 2025, he is committed to advancing the organization's influence and protecting advisors' interests.

Doug Massey has 40 years of experience in the financial industry, specializing in retirementplanning and life insurance. As NAIFA's President-Elect for 2025, he is committed to advancing the organization's influence and protecting advisors' interests.

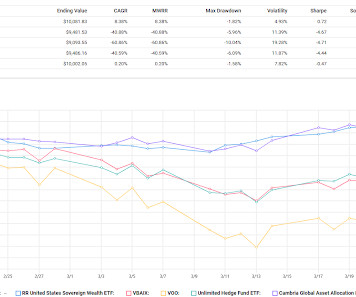

Is 2025 going to be a good year for SCHD as a broad based or core holding relative to other strategies or factors? There's no way to know of course but if 2025 turns out to be a bad year for the S&P 500 then there's a pretty good probability of SCHD doing better than market cap weighting (MCW) and maybe most of the other factors.

To plan your tax timeline, see our article, 2025 Tax Deadline Information for Individual Filers. Retirement Contributions: Proof of contributions to IRAs, 401ks, or other retirementplans, which may be deductible. Need to Find a Tax Professional for 2025? This is a product of Harness Tax LLC.

The TCJA has many provisions that are set to expire (sunset) at the end of 2025. Mortgage interest will once again be tax-deductible on larger loans As a result of the 2017 legislation, between 2018 and 2025, interest on new mortgages is only tax-deductible up to $750,000 of mortgage debt on a primary or second home.

Check out our Top 30 Influencers for Financial Advisors in 2025 here.) Blog posts, social media updates, webinars , and email campaigns that speak to market uncertainties, retirementplanning, or financial goal-setting will resonate more with potential clients.

The Medicare industry is facing major disruptions ahead of the 2025 open enrollment, with insurers cutting benefits, raising premiums, and exiting certain markets. This has led to increased confusion for beneficiaries, particularly in deciding between Medicare Advantage and Medigap plans.

How great have the returns been for the Mag 7 stocks for the last couple of years, but so far in 2025 most of them look like they are down mid-teens to mid-20's percent. Another dynamic that might be weighing the stocks down is the possible ending of the carried interest tax break.

Published: March 20th, 2025 Reading Time: 6 minutes Written by: The Zoe Team Have you ever stood in a grocery aisle, staring at a wall of options, unable to pick one? Budgeting & saving (23%): Uncertainty about creating a plan that works. RetirementPlanning (22%): Fear of running out of money or not saving enough.

While the market remains strong, how does this news affect the savings of retirees or those about to retire? . So, how do people who are retired or about to retire combat this inflation? But for someone retired or nearing retirement, this strategy could be fatal to their portfolio. .

Are you aiming to reach established business owners focused on retirementplanning? Calculators: Interactive tools, like budget or retirement calculators, offer personalized insights that are highly valuable to prospects. Ask yourself: Are you targeting young professionals eager to learn about investing?

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

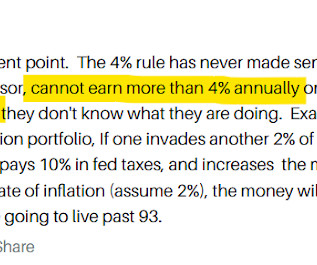

in 2025 instead of the typical 4%. A $38,000 withdrawal implies $950,000 in retirement assets. Now, at the start of 2025 a $31,000 fixit comes long, plus the $40,000+/- withdrawal. How many expensive fixits should we expect over the course of a 30 year retirement (use the number of years more applicable to you)?

The Wall Street Journal has an article up this weekend about investors rotating to dividend centric stocks and funds because they are doing well in 2025 as market cap weighting has struggled, especially since mid-February. The Schwab US Dividend Equity ETF (SCHD) seems to garner the most attention.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content