This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: According to a recent survey, advisors are putting an increasing share of client assets into model portfolios, allowing for customization and time savings that advisors appear to be using to provide more comprehensive planning services RIA M&A deal volume saw an annual record in 2024 as a lower cost of capital, (..)

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. GET STARTED 1. For those over 50, the limit is $8,000.

Every year brings changes in tax rules, and 2025 is no exception. Whether you are saving for retirement, running a business, or planning for your family’s future, these updates could affect your financial decisions throughout the year. Think of it as the tax system’s way of protecting your purchasing power.

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

In the absence of Congressional action, multiple provisions of the Tax Cut and Jobs Act (TCJA) will expire at the end of 2025, and tax rules will revert to what they were before the legislation. The TCJA reduced specific tax brackets and increased the standard deduction.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date. Available to taxpayers aged 70.5

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033.

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

Understanding business meal deductions Business meals continue to serve as a valuable tax deduction in 2025, with most qualifying expenses being 50% deductible when they involve legitimate business discussions with clients, customers, or associates.

While most taxpayers dont need to worry about estate and gift taxes, having significant assets can make them a challenge. Also, like most UHNW individuals, you may have income from several sources like investments, real estate, and business interests that may require special taxplanning. Estate taxes also offer challenges.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. The TCJA has many provisions that are set to expire (sunset) at the end of 2025. In addition, the SALT cap, currently $10,000 per tax return (not per person) will be eliminated.

This article covers a comprehensive list of the most common forms, documents, and information needed to file taxes. If you need a cheat sheet, download our 1-page tax prep checklist. To plan your tax timeline, see our article, 2025Tax Deadline Information for Individual Filers.

Andy Panko started a taxes in retirement Facebook group. They may be focused on the three steps ahead of them, but you are focused on the broader view including 30 years from now when you are going to retire, and that is because I talk to script writers all day and for that reason I can see a broader picture that you can not. “Oh

Here are the top five Roth-related retirement changes following the passing of Secure Act 2.0. 529 plan to Roth IRA rollovers. Starting with the 2017 Tax Cuts and Jobs Act, then the 2019 Secure Act 1.0, it’s clear that investors need to be adaptive in taxplanning. 5 new changes to Roth accounts in Secure Act 2.0.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. The TCJA has many provisions that are set to expire (sunset) at the end of 2025. In addition, the SALT cap, currently $10,000 per tax return (not per person) will be eliminated.

Other pay : Certain employees can be eligible for “pay in lieu of redeployment” (9 weeks) and an “additional separation bonus” (8 weeks) It’s important to note that severance payouts are taxed as ordinary income in the year of payout. Taxplanning for a transition out of Intel is critical.

And as 2024 draws to a close, we wanted to highlight 24 of the most popular and insightful articles that were featured throughout the year (that you might have missed!). Read More.

Market declines also bring opportunities to trigger valuations for income and transfer tax purposes , so that such taxes are applied to current, lower values, thereby lessening the total amount of tax ultimately paid. Deferral of required retirementplan distributions.

Market declines also bring opportunities to trigger valuations for income and transfer tax purposes , so that such taxes are applied to current, lower values, thereby lessening the total amount of tax ultimately paid. Deferral of required retirementplan distributions. GIFT AND ESTATE TAXPLANNING.

Updated for 2024 – 2025. Because many taxpayers earn too much to make pre-tax IRA contributions as they have a 401(k) at work. Many people end up paying taxes twice. There are income limits for contributions to a traditional IRA that qualify for a tax deduction. In the vast majority of cases the answer is no.

However, when exercised, holders must calculate the spread between strike price and fair market value for Alternative Minimum Tax purposes. Documentation significantly impacts ISO taxplanning. Companies provide Tax Form 3921 in January to detail the information needed for accurate calculations.

Like gardening or working out, taxplanning is one of those activities where you get out what you put in. Taxplanning is similar in the sense that you can put work in on the front end that youll reap benefits from later. Many of us just do tax preparation, dropping off a shoebox of documents with a CPA for the weekend.

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Optimize retirementplan contributions The maximum allowable 401(k) contribution for 2023 is $22,500, with a $7,500 additional contribution, if the plan allows, for taxpayers who are 50 and over.

While the final submitted text has not been released, some experts suggest that the DoL likely made few changes to its initial proposal, despite significant opposition from broker-dealers that could lead to the judicial system deciding the rule’s ultimate fate.

When the original SECURE Act was passed in December 2019, it brought sweeping changes to the post-death tax treatment of qualified retirement accounts.

A financial or tax adviser can help you identify ways to capture that loss so you can offset gains from your liquidity event. Max out your retirement contributions. The current lifetime gift tax exclusion is $12.06M (or $24.12 The exclusion may reduce back to pre-2017 levels of $5M after 2025. at the federal level.

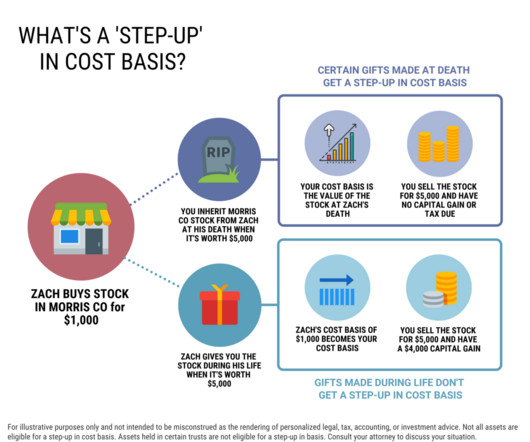

Example of a step-up in tax basis on stocks inherited at death What types of assets are eligible for a step-up? Non-retirement assets like stocks in a brokerage account, inherited home , antiques/art/collectables, or other real estate, are generally eligible for a step-up in cost basis.

If you’ve just inherited a retirement account like an IRA or 401(k) from a parent, sibling, or relative, you may be unsure about what your options are and what to do next. Most non-spouse beneficiaries inheriting an IRA, 401(k), or retirement account from the original account owner must take the money in 10 years.

While the final submitted text has not been released, some experts suggest that the DoL likely made few changes to its initial proposal, despite significant opposition from broker-dealers that could lead to the judicial system deciding the rule’s ultimate fate.

To qualify as an accredited investor in 2025, you must meet one of the following criteria: Income Requirement: Earn at least $200,000 per year ($300,000 with a spouse or domestic partner) for the past two years, with expectations of the same for the current year. Can I hold alternative investments in my retirement accounts?

Any reporting companies created during 2024 have 90 days to file this report, and for reporting companies created in 2025 or after this filing deadline is reduced to 30 days. On the estate planning front, chief among these potential changes is the sunset of the gift and estate tax basic exclusion amount for U.S.

The Long Game: Roth Conversions & Legacy Planning ajackson Thu, 08/01/2019 - 14:51 Legacy planning is all about transferring wealth to descendants as efficiently as possible. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

Legacy planning is all about transferring wealth to descendants as efficiently as possible. So it may be surprising to hear that a Roth IRA—a vehicle ostensibly intended for retirement income—can be a powerful mechanism for next-generation wealth transfer. Background.

The eligibility criteria and rules surrounding home office tax deductions for remote workers are far from straightforward, however. In this article, we examine remote work home office tax deductions in 2025 and provide a clear overview of who qualifies. How Harness can help FAQs Am I eligible for home office tax deductions?

Here are the 30 voices to follow in 2025, along with rising stars you shouldnt miss. Michael Kitces Reason to Follow: Deep insights into financial planning and wealth management Michael Kitces continues to dominate as a thought leader in financial planning. The financial advisory world is evolving faster than ever.

In this guide, we’ll explore the key tax changes in effect for 2025, how theyll influence your filing status, retirement savings, investment, and estate planningand offer strategic advice to help high-income and high-net-worth individuals prepare more effectively for upcoming coming tax changes. That said, U.S.

This ensures you have sufficient funds for your quarterly estimated tax payments. Additionally, you can bolster your long-term financial security by maximizing contributions to retirement accounts like SEP IRAs or Solo 401(k)s, capitalizing on their tax-deferred growth potential.

The end of the year is an ideal time to start planning for the year ahead and make sure youre on target to achieve those goals. Here’s a list of things to consider checking as we head into 2025. Good financial planning is all about asset and liability matching across time. Are you on track to retire when you want to?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content