This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In recent years, the Internal Revenue Code (IRC) has endured some drastic changes resulting from legislative action that have altered the strategies estateplanning professionals have recommended to clients. Contrary to what their name might suggest, flexibility can even be built into irrevocable trusts.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

For individuals, a permanent life insurance plan can play a key role in estateplanning by helping reduce estate taxes. Offset Taxes in EstatePlanningEstate taxes can be a problem for high-net-worth individuals passing on more than the IRS estate tax exclusion, after which the tax rate on transferred money is 40%.

covers some of the top estateplanning trends that tax advisors should be tracking during the second half of 2024. Now that the mid-point of 2024 has passed, we are faced with an environment where little has changed with respect to the wait-and-see posture of estate and wealth transfer planning. citizens and residents.

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. Gifting Other than transferring assets after death, the other primary way to transfer wealth is to gift portions of your estate during your lifetime.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

Frontloading 529 Contributions Contributions to 529 plans can also be frontloaded or “superfunded”, allowing you to make up to five years’ worth of contributions in a single year without incurring gift taxes. For 2024, you can contribute up to $90,000 per beneficiary (or $180,000 if married filing jointly) using this strategy.

High-net-worth individuals who possess a significant number and value of assets and complex financial portfolios may find it hard to manage their finances. However, given the high value of wealth, it becomes all the more critical for high-net-worth individuals to plan their finances optimally. in their work endeavors.

Income from the licensing deal with UMG for the rest of the world will similarly go to Sony when that deal expires in 2026 or 2027, at which point SME will become the worldwide distributor and owner of all content.” And with total control of all the assets comes power. ” – Hits Daily Double I don’t really care.

The potential supplemental estate tax liability for a married couple may be in the $5.6 Attorneys are telling us that 2024 is the time to review and change your estateplan as the lines may be out the door in 2025 for taxpayers wanting to make last minute changes to take advantage of the higher exemption amount.

Like individuals, businesses holding investments and other capital assets should consider other income, gains, and losses when determining when to sell capital assets. In 2026, the current larger exemption will be reduced from $12,920,000 in 2023 to about $6 million per person ($5 million per person adjusted for inflation).

The challenge lies not only in amassing wealth but also in the practical preservation and transfer of assets across generations. But estate tax can eat into this wealth and leave the next generation with a smaller nest egg. Estateplanning for wealthy families during a market dip Estateplanning can be an expensive affair.

On today’s show, Megan Gorman discusses how her firm meets the business challenges of serving high-net-worth families, including personalized services that address both the technical and emotional aspects of wealth, executing on client promises, tax and estateplanning, and building a world-class team.

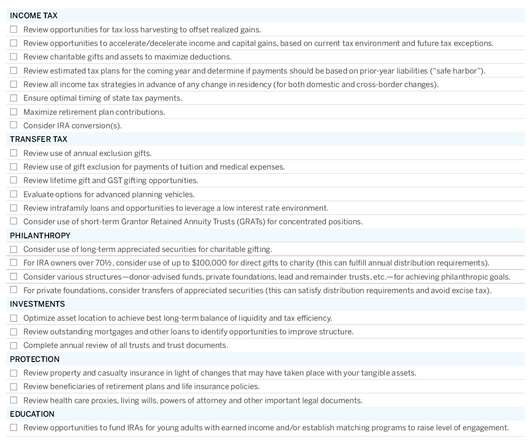

Market conditions may be volatile, but our planning efforts are, as always, focused on stability and consistency. You can find our annual planning checklist at the end of this article. OZ Funds” allow the deferral, and partial avoidance, of capital gains arising out of the sale of appreciated assets.

If its been some time since you established your estateplan, you may want to think about giving it a review. After all, you dont want your loved ones blowing the dust off your original plan years from now only to discover that you havent accounted for all the changes along the way. How will this affect your overall plan?

Dear Mr. Market: Normally we write you letters about the markets or the economy…but what’s all that worth if your assets are not protected or properly positioned for what you intended them to do? The following article is penned by a guest author and Long Beach estate planner, Curtis Kaiser.

For individuals with investments in assets such as stocks, real estate, and other securities, changes in the capital gains taxespecially long-term capital gainswill be particularly relevant. Assets held for over one year, however, are subject to more favorable long-term capital gains tax rates. Starting at $1,500 per year.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content