This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that the Treasury Department has finalized rules requiring most SEC-registered RIAs to implement risk-based Anti-Money Laundering and Countering the Financing of Terrorism programs, including a requirement to report suspicious (..)

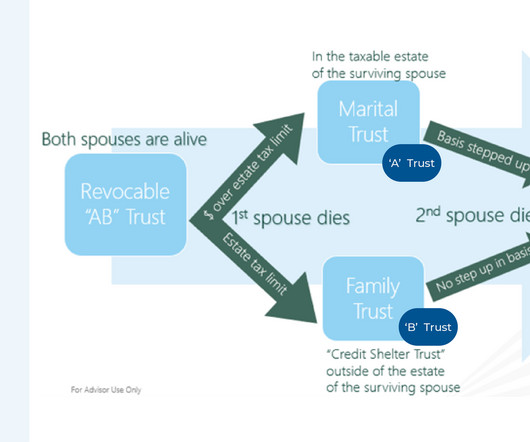

In recent years, the Internal Revenue Code (IRC) has endured some drastic changes resulting from legislative action that have altered the strategies estate planning professionals have recommended to clients. For instance, prior to the 2017 Tax Cuts and Jobs Act (TCJA), "A/B trusts" had become ubiquitous for spousal estate taxplanning.

One strategy is to accumulate deductions that a client would normally take over 2 years into a single year. For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Don’t forget about the net investment income tax (NIIT), which is an additional 3.8%

Effective ways to achieve this include: For employees : If your employer offers this option, request that your year-end bonus be deferred to January 2026. This moves your taxable income to the next tax year, potentially lowering your tax bill for 2025.

Guest: Megan Gorman, Founder and Managing Partner of Chequers Financial Management , a female-owned, high-net-worth tax and financial planning firm based in San Francisco. In a Nutshell: High-net-worth clients have high-net-worth needs. Megan’s vision of the “perfect” client experience.

Now that the mid-point of 2024 has passed, we are faced with an environment where little has changed with respect to the wait-and-see posture of estate and wealth transfer planning. However, awareness is key, both for clients and advisors.

Other pay : Certain employees can be eligible for “pay in lieu of redeployment” (9 weeks) and an “additional separation bonus” (8 weeks) It’s important to note that severance payouts are taxed as ordinary income in the year of payout. Taxplanning for a transition out of Intel is critical.

If your financial advisor is not keeping a close eye on your taxes, they might be missing out on various opportunities that could impact your financial well-being. An effective financial advisor should be proactive in reviewing your taxplan before the year-end. Annual Roth conversions can be one measure to tackle the changes.

If you allow your clients to distribute their income incorrectly, they government is going to take all of it. Given that financial advisors are always encouraging their clients to stash away money in tax deferred vehicles, making those distributions taxable upon withdrawal. #2 An example is how taxplanning is handled.

With Republicans appearing to have secured a sweep of the White House and both chambers of Congress, the most immediate question for many financial advisors and their clients is what impact the election results will have on the scheduled expiration of the Tax Cuts & Jobs Act (TCJA) at the end of 2025. Read More.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content