This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Podcasts Michael Kitces talks with Meg Bartelt of Flow FinancialPlanning about evolving her practice. kitces.com) Brendan Frazier talks with Bari Tessler, author of "The Art of Money: A Life-Changing Guide to Financial Happiness." 1, 2026 and becomes a big problem for reactive RIAs who fail to help clients take action now."

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

By Matt Lewis, CLTC, Vice President, Insurance Life insurance is designed to provide for your loved ones after your death, giving you peace of mind that their financial needs will be met without your income. But life insurance can benefit your financialplanning in many other ways. As of 2023, that exclusion is $12.92

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

That must mean it’s time to roll up my sleeves and get to work on year-end financialplanning – with an emphasis on 2023 income tax. The potential supplemental estate tax liability for a married couple may be in the $5.6

Frontloading 529 Contributions Contributions to 529 plans can also be frontloaded or “superfunded”, allowing you to make up to five years’ worth of contributions in a single year without incurring gift taxes. Review Your EstatePlanning The end of the year can also be a practical time to take stock of your long-term estateplanning.

High-net-worth individuals who possess a significant number and value of assets and complex financial portfolios may find it hard to manage their finances. However, given the high value of wealth, it becomes all the more critical for high-net-worth individuals to plan their finances optimally. in their work endeavors.

Guest: Megan Gorman, Founder and Managing Partner of Chequers Financial Management , a female-owned, high-net-worth tax and financialplanning firm based in San Francisco. And so right now, like a lot of advisors, we’re dealing with the fact that the unified credit is scheduled to go down in 2026.

Despite having significant resources, wealthy individuals face the threat of estate taxes that can reduce the wealth intended for the next generation. Careful financialplanning during a market dip can play a crucial role in minimizing the impact of estate taxes on intergenerational wealth.

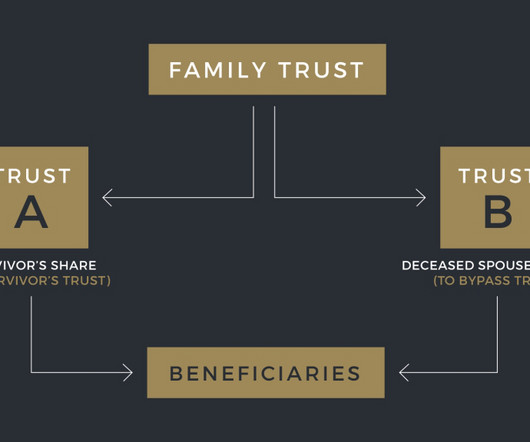

Has it been nearly a decade (or more) since you and your spouse updated your estateplan? If so, there’s a good chance your plan includes the classic “AB Trust” structure, which—prior to 2011—was the primary way for married couples to double the value of their federal estate tax exemptions.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content