This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

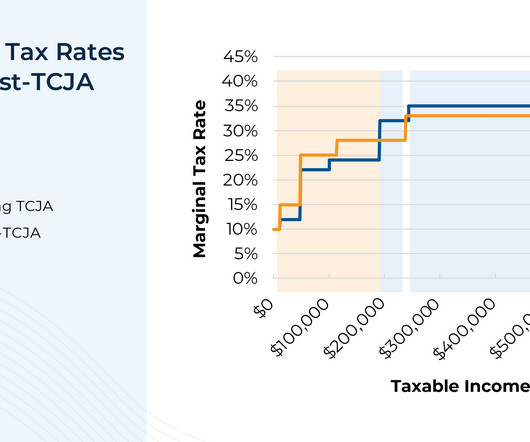

And although TCJA's reputation as a broad tax cut might give the impression that everyone's tax rates would increase after its expiration, comparing the current Federal tax brackets with their estimated post-TCJA equivalents shows that a fair number of households will actually see their tax rates decrease.

Which is surprising to some, given that a decade ago, the emergence of so-called "robo-advisors" was supposed to displace human financialadvisors and compress advisory fees. In reality, though, the robos struggled to gain traction, and the human financial advice business just continues to grow.

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. Individual Retirement Accounts (IRAs): Contribute up to $7,000 for 2024 ($8,000 if aged 50+). For the majority of people, however, April 15th will remain the deadline. Available to taxpayers aged 70.5

For Canada alone, the expected is 50% of accumulated wealth by 2026. Holding such a large portion of the world’s wealth, it would be naive to ignore the significance of women’s role in the financial industry. Related: 7 Productive Cold Calling Tips for FinancialAdvisors. What Women Want. In Conclusion.

Jump-starting (or catching up on) retirement savings by investing the money in a brokerage account. Inherited IRA or retirement account. If you inherit an IRA, 401(k), or other type of retirement account from a parent, you must take the inheritance in 10 years. Discuss your situation with your financialadvisor.

Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Checklist: Year-end Tax Planning Strategies Review the following tax strategies with your tax advisor and/or financialadvisor before the end of the year. GET STARTED 1.

The decision to hire a financialadvisor is a prudent move. Seeking professional advice can provide valuable insights and a roadmap to achieve your financial goals with strategic planning. But the world of financial advice is crowded. Moreover, your financialadvisor’s way of working might not match your style.

in 2026, the eligibility age will be adjusted to 46. The beneficiary may only make this contribution if they are not participating in any employer sponsored retirement plan. The disability can be physical or mental, and it must significantly impair the person’s ability to function in daily life.

Direct indexing assets, currently at $462 billion, are expected to rise up to $825 billion by 2026, according to Cerulli Associates data that is cited in the article, making its growth forecast the biggest out of ETFs, mutual funds, and separately managed accounts. The service costs $4.99

trillion by 2021, it is expected to rise to $23 trillion by 2026. Experienced financialadvisors specializing in alternative investments can provide valuable insights, help you navigate the intricacies of the market and guide you towards suitable investment opportunities. appeared first on Fortune FinancialAdvisors.

trillion by 2021, it is expected to rise to $23 trillion by 2026. Experienced financialadvisors specializing in alternative investments can provide valuable insights, help you navigate the intricacies of the market and guide you towards suitable investment opportunities. appeared first on Fortune FinancialAdvisors.

For example, if you work for a company and leave due retirement, death, disability, or due to a family emergency or a health issue, your employer may be willing to offer you a post-termination grace period (or another alternative, like speeding up the vesting schedule). Talk to your financialadvisor before making any investing decisions.

While this is by no means an exhaustive or comprehensive list of financial planning tools, these three broad areas will get you headed in the right direction. As you’re thinking about these topics, please remember to consult with your financialadvisor to make sure the information you have is accurate and beneficial to your unique situation.

million for couples), but it will revert to its pre-2018 level of $5 million (adjusted for inflation) in 2026. Essentially, the policy would not provide an instant benefit, but would instead provide an income stream for the employee in the long-term, perhaps in retirement. As of 2023, that exclusion is $12.92 million ($25.84

The Roth IRA (Individual Retirement Account) is a tax-advantaged retirement savings account wherein you contribute after-tax dollars, earn tax-free growth, and make tax-free withdrawals (subject to fulfilment of certain conditions). The Roth IRA is a popular retirement savings vehicle along with the 401(k) and the traditional IRA.

If the sunset occurs, this inflation-adjusted amount, which is currently $13,610,000 as of July 2024 , could be reduced by one-half (after inflation adjustments for 2025 and 2026) starting on January 1, 2026. Griffin educates wealth transfer professionals through his newsletter, State of Estates, which can be found at [link].

It is a process that can allow high-net-worth individuals to transfer their wealth to future generations while minimizing tax burdens, maximizing financial security, and protecting their hard-earned money. Need a financialadvisor? Compare vetted advisors matched to your specific requirements. million in 2023.

The IRMAA , or Medicare income-related monthly adjustment amount, is a bit of a missed opportunity for many financialadvisors. I am a CFA® charterholder and financialadvisor marketing consultant. I am an irreverent and fun marketing consultant for financialadvisors. It’s time for a revamp. Are you really?

In this guide, we’ll explore the key tax changes in effect for 2025, how theyll influence your filing status, retirement savings, investment, and estate planningand offer strategic advice to help high-income and high-net-worth individuals prepare more effectively for upcoming coming tax changes. Minimizes taxes if rolled over promptly.

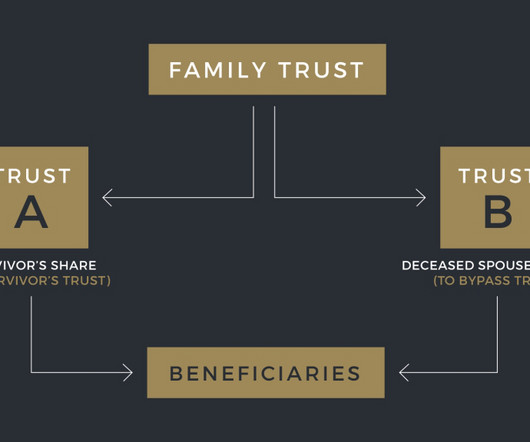

If Bill dies in 2026 without using any of his ~$7.5 Portability is now a permanent feature of federal estate tax law, but if your estate plan still includes AB Trust planning, it might now be doing more harm than good. million estate tax exemption, Alice can file a portability election with the IRS—without needing a separate trust.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content