This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that the Treasury Department has finalized rules requiring most SEC-registered RIAs to implement risk-based Anti-Money Laundering and Countering the Financing of Terrorism programs, including a requirement to report suspicious (..)

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. In 2024, the lifetime gift tax exemption is $13.61

Deferring income to a future year will allow you to reduce your current tax burden and keep more of your money working for you. Effective ways to achieve this include: For employees : If your employer offers this option, request that your year-end bonus be deferred to January 2026. Starting at $1,500 per year.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. It can also preclude some taxplanning strategies down the road.

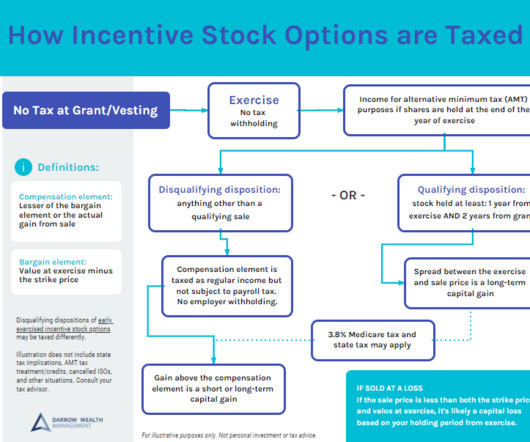

6 tax strategies for incentive stock options and AMT Triggering the alternative minimum tax isn’t the end of the world, but you don’t want to do it by accident. By December, your CPA and financialadvisor can help in developing a tax projection for the year. How Incentive Stock Options are Taxed 3.

The decision to hire a financialadvisor is a prudent move. Seeking professional advice can provide valuable insights and a roadmap to achieve your financial goals with strategic planning. But the world of financial advice is crowded. For this, you must know how to evaluate a financialadvisor’s performance.

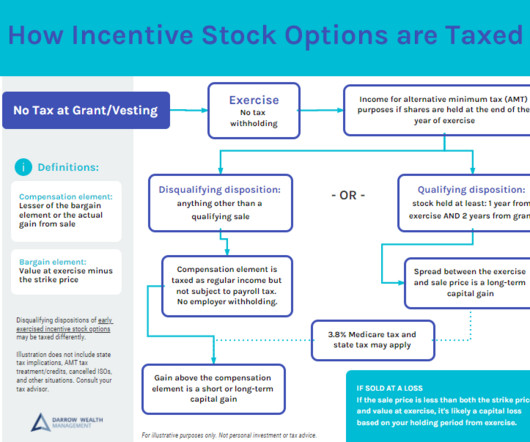

6 tax strategies for incentive stock options and AMT Triggering the alternative minimum tax isn’t the end of the world, but you don’t want to do it by accident. By December, your CPA and financialadvisor can help in developing a tax projection for the year. How Incentive Stock Options are Taxed 3.

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. For reference, the federal estate tax exemption limit is set to revert back to $5 million (or around $7 million when adjusted for inflation).

If the sunset occurs, this inflation-adjusted amount, which is currently $13,610,000 as of July 2024 , could be reduced by one-half (after inflation adjustments for 2025 and 2026) starting on January 1, 2026. Harness will continue to be in your corner with updates and tax practice management tips to help you tackle uncertainty head-on.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. It can also preclude some taxplanning strategies down the road.

If the manager chooses to use the Three-Year Carried Interest Loophole, they would not be required to pay taxes on that $200,000 until 2026. However, if the investment is sold before the three-year mark, the standard tax rate would apply, and the manager would need to pay tax on their carried interest.

The IRMAA , or Medicare income-related monthly adjustment amount, is a bit of a missed opportunity for many financialadvisors. We’ve got special guests Dan McGrath and Paul Morrison of IRMAA Certified Planner with us today to talk about what you may be overlooking about IRMAA planning. An example is how taxplanning is handled.

Given the complexities involved in backdoor strategies, it’s advisable to consult with a tax professional whos well-acquainted with the mechanisms involved in backdoor Roth strategies. Get started Harness makes it easy to find tax and financialadvisors best suited to your needs. Starting at $1,500 per year.

With Republicans appearing to have secured a sweep of the White House and both chambers of Congress, the most immediate question for many financialadvisors and their clients is what impact the election results will have on the scheduled expiration of the Tax Cuts & Jobs Act (TCJA) at the end of 2025. Read More.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content