This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Podcasts Michael Kitces talks with Meg Bartelt of Flow FinancialPlanning about evolving her practice. kitces.com) Brendan Frazier talks with Bari Tessler, author of "The Art of Money: A Life-Changing Guide to Financial Happiness." 1, 2026 and becomes a big problem for reactive RIAs who fail to help clients take action now."

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

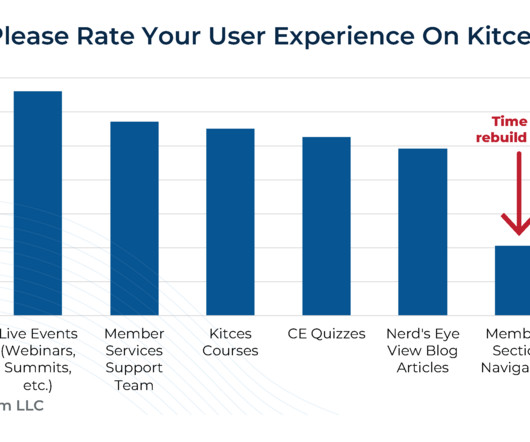

And also make it easier for us to redesign the Nerd's Eye View blog side of the website as well, in 2026!) Which means over the next 12 months, we're going to rebuild it all from scratch, with a modern technology foundation that will allow us to better scale over the next decade.

Harnessing Tax-Advantaged Savings Retirement accounts and health savings plans offer the dual benefits of saving tax and building wealth. They arent just personal milestones but important life events and moments that should prompt you to update your financialplans.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

That must mean it’s time to roll up my sleeves and get to work on year-end financialplanning – with an emphasis on 2023 income tax. Many states also exempt retirement income, which may include Social Security. Lastly, I allocate the retirementplan contributions between Roth and Traditional 401(k) accounts.

Checklist: Year-end Tax Planning Strategies Review the following tax strategies with your tax advisor and/or financial advisor before the end of the year. Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income.

in 2026, the eligibility age will be adjusted to 46. The beneficiary may only make this contribution if they are not participating in any employer sponsored retirementplan. The current tax law also allows for a rollover from a 529 plan to an ABLE account up to the annual limit amount. With the passing of Secure Act 2.0,

This is in addition to the accelerated vesting provided by Intel retirement rules. However, if you are eligible for retirement at Intel ( here’s a helpful post on the subject ), the APB will be prorated according to the number of full calendar months you worked. For APB, December 31 st is the magic day.

It is a strategic initiative to ensure you are making the most of available opportunities and safeguarding your financial future. For example, there is going to be an increase in tax rates in 2026 due to the onset of the Tax Cuts and Jobs Act. Developing a plan to navigate the complexities of Social Security taxes is essential.

trillion by 2021, it is expected to rise to $23 trillion by 2026. Evaluate your financial situation, investment time horizon and potential cash flow requirements. Ensure that the illiquid nature of certain alternative investments aligns with your financialplans. between 2015 and the end of 2021. trillion in 2015 to$13.32

trillion by 2021, it is expected to rise to $23 trillion by 2026. Evaluate your financial situation, investment time horizon and potential cash flow requirements. Ensure that the illiquid nature of certain alternative investments aligns with your financialplans. between 2015 and the end of 2021. trillion in 2015 to$13.32

By Ryan Egolf, EA, Senior Tax Planner As the New Year quickly approaches, it’s time to put a bow on your 2023 financialplan. While this is by no means an exhaustive or comprehensive list of financialplanning tools, these three broad areas will get you headed in the right direction.

By Matt Lewis, CLTC, Vice President, Insurance Life insurance is designed to provide for your loved ones after your death, giving you peace of mind that their financial needs will be met without your income. But life insurance can benefit your financialplanning in many other ways. As of 2023, that exclusion is $12.92

However, given the high value of wealth, it becomes all the more critical for high-net-worth individuals to plan their finances optimally. Estate planning is one of the key components of financialplanning these individuals need to focus on. Need a financial advisor? million in 2023.

Although Gen Xers are getting older, the majority of people using a financial advisor are retired or pre-retirees. Retirement for those people isn’t about capturing the highest rate of return – you’ve already won the race hopefully by that point – it’s about making that money survive because you are no longer working.

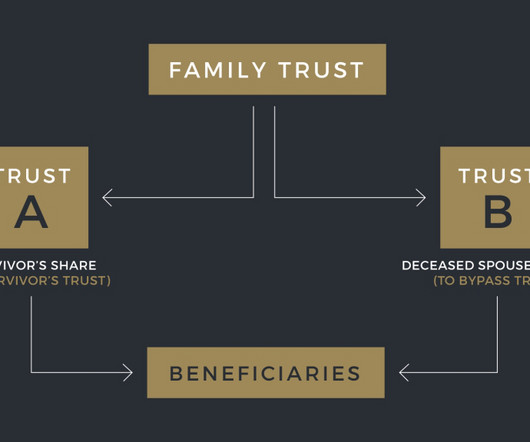

Portability is now a permanent feature of federal estate tax law, but if your estate plan still includes AB Trust planning, it might now be doing more harm than good. To illustrate how portability can simplify and enhance an estate plan, let’s look at Bill and Alice, who have been married for 40 years.

The sooner you start saving and the more you save, the faster and larger your retirement nest egg will grow. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content