This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. For some, this may lead to more taxes paid on capital gains.

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. What if, instead of seeing it as a mere logistic hurdle, we embraced it as a moment to refine our financial strategy? Analyze whether your tax rate will rise or fall in the coming years.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that the Treasury Department has finalized rules requiring most SEC-registered RIAs to implement risk-based Anti-Money Laundering and Countering the Financing of Terrorism programs, including a requirement to report suspicious (..)

And also make it easier for us to redesign the Nerd's Eye View blog side of the website as well, in 2026!) Which means over the next 12 months, we're going to rebuild it all from scratch, with a modern technology foundation that will allow us to better scale over the next decade.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. For some, this may lead to more taxes paid on capital gains.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. In tax lingo, this is known as substantial risk of forfeiture.

That must mean it’s time to roll up my sleeves and get to work on year-end financialplanning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). AGI impacts multiple other tax considerations.

Guest: Megan Gorman, Founder and Managing Partner of Chequers Financial Management , a female-owned, high-net-worth tax and financialplanning firm based in San Francisco. Common financial issues that high-net-worth individuals face and how Megan created a “one-stop shop” to meet her client’s needs.

in 2026, the eligibility age will be adjusted to 46. Tax-Advantaged Savings : Contributions to ABLE accounts are made with after-tax dollars, but the earnings on the account grow tax-free. Withdrawals are also tax-free if they are used for qualified disability expenses. With the passing of Secure Act 2.0,

If you have incentive stock options, you’ve probably heard of the alternative minimum tax (AMT). Essentially, the alternative minimum tax is a prepayment of taxes. The credit reduces your tax liability to reflect prepaid tax. Early sales of ISOs are taxed in the regular tax system.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. In tax lingo, this is known as substantial risk of forfeiture.

Whether you’re in venture capital, private equity, or angel investing, it’s important to understand the tax implications of your investment income. One of the unique characteristics of carried interest is that it is taxed as a capital gain rather than ordinary income. K-1 forms are reported on an individual’s tax return.

If you have incentive stock options, you’ve probably heard of the alternative minimum tax (AMT). Essentially, the alternative minimum tax is a prepayment of taxes. The credit reduces your tax liability to reflect prepaid tax. Early sales of ISOs are taxed in the regular tax system.

Other pay : Certain employees can be eligible for “pay in lieu of redeployment” (9 weeks) and an “additional separation bonus” (8 weeks) It’s important to note that severance payouts are taxed as ordinary income in the year of payout. Taxplanning for a transition out of Intel is critical.

Step 2: See if the financial advisor conducts an annual tax review Ensuring that your financial advisor reviews your tax return annually is a crucial step in maximizing your financial benefits. An effective financial advisor should be proactive in reviewing your taxplan before the year-end.

trillion by 2021, it is expected to rise to $23 trillion by 2026. Evaluate your financial situation, investment time horizon and potential cash flow requirements. Ensure that the illiquid nature of certain alternative investments aligns with your financialplans. between 2015 and the end of 2021. trillion in 2015 to$13.32

trillion by 2021, it is expected to rise to $23 trillion by 2026. Evaluate your financial situation, investment time horizon and potential cash flow requirements. Ensure that the illiquid nature of certain alternative investments aligns with your financialplans. between 2015 and the end of 2021. trillion in 2015 to$13.32

By Ryan Egolf, EA, Senior Tax Planner As the New Year quickly approaches, it’s time to put a bow on your 2023 financialplan. In some cases, those payments are tax-free. Check into your employer’s short- and long-term disability plans, as they are usually the most affordable options.

By Matt Lewis, CLTC, Vice President, Insurance Life insurance is designed to provide for your loved ones after your death, giving you peace of mind that their financial needs will be met without your income. But life insurance can benefit your financialplanning in many other ways. Estate Taxes.” million ($25.84

But estate tax can eat into this wealth and leave the next generation with a smaller nest egg. Despite having significant resources, wealthy individuals face the threat of estate taxes that can reduce the wealth intended for the next generation. It can trigger tax for the estate owner as well as the inheritor.

However, given the high value of wealth, it becomes all the more critical for high-net-worth individuals to plan their finances optimally. Estate planning is one of the key components of financialplanning these individuals need to focus on. and estate planning can help you discover these.

Given that financial advisors are always encouraging their clients to stash away money in tax deferred vehicles, making those distributions taxable upon withdrawal. #2 Tax questions we should ponder more deeply Advisors are working on a way that is outdated when it comes to IRMAA planning. 4 What is income for IRMAA?

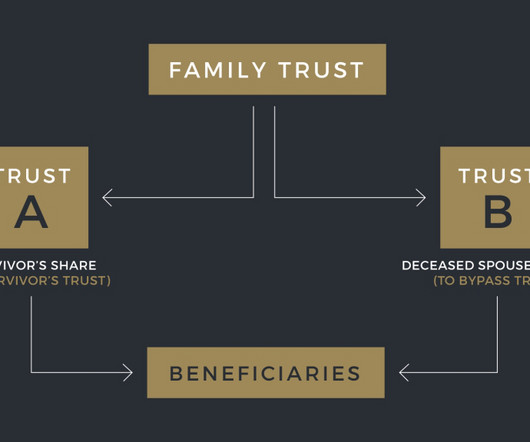

If so, there’s a good chance your plan includes the classic “AB Trust” structure, which—prior to 2011—was the primary way for married couples to double the value of their federal estate tax exemptions. But in 2011, the concept of “portability” changed the estate planning landscape. This election allows her to add Bill’s ~$7.5

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in individual stocks , certain exchange traded funds (ETFs), and notes including AMC 2026, but at the time of publishing had no direct position in DJT, GME, AMC or any other security referenced in this article.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content