This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

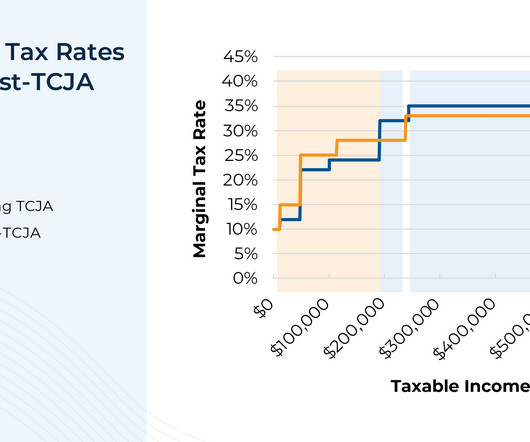

The Tax Cuts and Jobs Act (TCJA), passed in 2017, was one of the most extensive pieces of tax legislation to be passed in the last 30 years, touching many aspects of individual, corporate, and estate tax. elections.

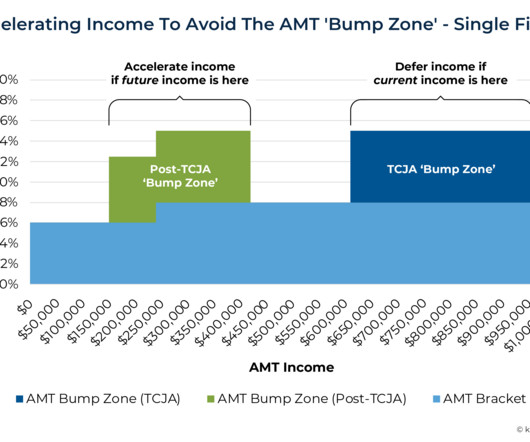

Since the Tax Cuts & Jobs Act (TJCA) was passed in 2017, few households have been subject to the Alternative Minimum Tax (AMT), which TCJA restructured so that it applied mainly to a select number of upper-income households.

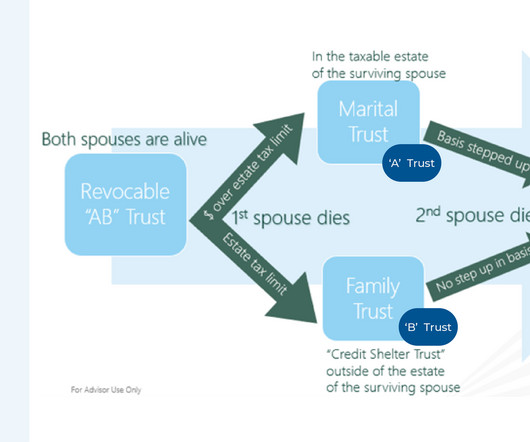

In recent years, the Internal Revenue Code (IRC) has endured some drastic changes resulting from legislative action that have altered the strategies estate planning professionals have recommended to clients. For instance, prior to the 2017 Tax Cuts and Jobs Act (TCJA), "A/B trusts" had become ubiquitous for spousal estate taxplanning.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. For some, this may lead to more taxes paid on capital gains.

thinkadvisor.com) The latest in advisortech news from April including the SEC's scrutiny of tax-loss harvesting systems. kitces.com) Practice management Why succession planning is important to firm owners whether they plan to sell or not. sciencedaily.com) How tax-adjusting a portfolio works in practice.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that the Treasury Department has finalized rules requiring most SEC-registered RIAs to implement risk-based Anti-Money Laundering and Countering the Financing of Terrorism programs, including a requirement to report suspicious (..)

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

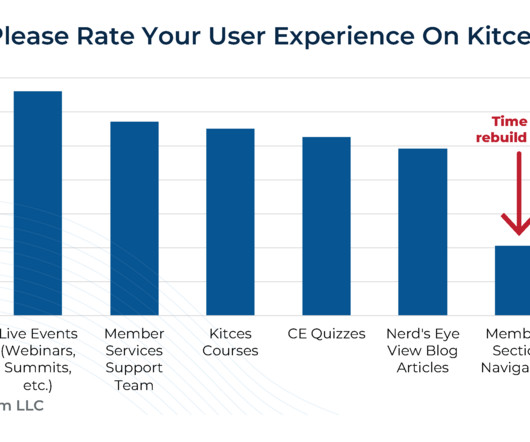

And also make it easier for us to redesign the Nerd's Eye View blog side of the website as well, in 2026!) Which means over the next 12 months, we're going to rebuild it all from scratch, with a modern technology foundation that will allow us to better scale over the next decade.

Petersen, CPA, CFP ® , CP, Affluent Wealth Planning The holidays are upon us! That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA).

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. Let’s take a look at the tax impact and other considerations of each. million before triggering federal estate taxes).

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. For some, this may lead to more taxes paid on capital gains.

Podcasts Michael Kitces talks with Ann Garcia, partner of Independent Progressive Advisors, about planning for mid-work professionals. riabiz.com) Taxes How pre-tax retirement contributions provide flexibility down the road. kitces.com) Tax strategies if the TCJA expires in 2026.

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. Even if a client believes they would not be subject to estate or gift tax under current law, you may want to re-examine the value of their assets to determine whether they exceed a lower exemption amount.

That being said, you will still need to be cognizant of when they vest, how they can impact your tax bill, and when may be the best time to sell or hold shares. Taxes and Portfolio Concentration: The Importance of Managing Your RSUs RSUs are relatively simple to manage when compared to employees stock options.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. In tax lingo, this is known as substantial risk of forfeiture.

But life insurance can benefit your financial planning in many other ways. For individuals, a permanent life insurance plan can play a key role in estate planning by helping reduce estate taxes. million for couples), but it will revert to its pre-2018 level of $5 million (adjusted for inflation) in 2026.

In this guest post, Harness Tax Advisory Council member, Griffin Bridgers, J.D., covers some of the top estate planning trends that tax advisors should be tracking during the second half of 2024. However, awareness is key, both for clients and advisors. citizens and residents. The SECURE Act 1.0

By Ryan Egolf, EA, Senior Tax Planner As the New Year quickly approaches, it’s time to put a bow on your 2023 financial plan. While this is by no means an exhaustive or comprehensive list of financial planning tools, these three broad areas will get you headed in the right direction. In some cases, those payments are tax-free.

A highlight of the future plans of both the companies and a summary conclude the article at the end. billion in value by 2026. However, the figures of Gujarat Fluorochemicals are not comparable historically because of exception tax treatment in base year FY19. Next, we’ll learn about the two businesses.

just upended retirement planning…again. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. Here are some taxplanning strategies to consider when you should start drawing from your IRA. The Secure Act 2.0 But just because you can doesn’t mean you should.

The industry is expected to grow at a CAGR of approximately 16% from 2022 to 2026. 36% YoY Growth (%) 48% 25% KPIT reported a Profit after tax of Rs. However, we should take Tata Tech’s Net Profit growth in FY23 with a pinch of salt as it involves a Deferred Tax Income of Rs. Additionally, digital engineering spending.

A highlight of the future plans and a summary conclude the article at the end. FY 2021-22 Annual Report The structural shift is expected to benefit the nation immensely and increase its share in the global specialty chemicals industry to 6% by 2026 from 4%. Next, we’ll look at the market size and opportunities.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033. Starting in 2026, the catch-up will be indexed by inflation.

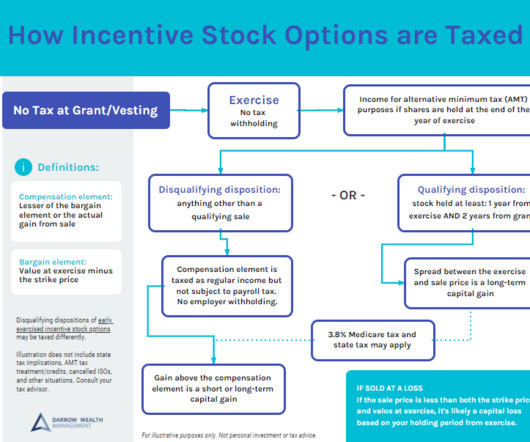

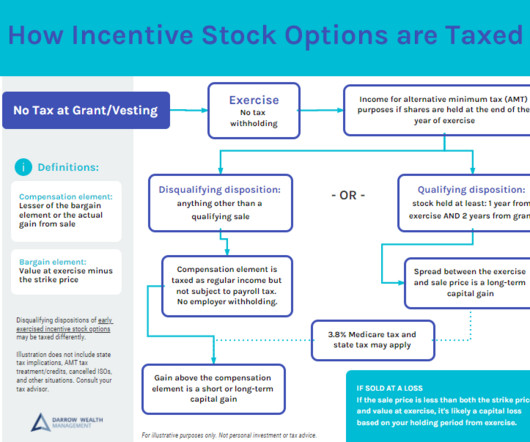

6 tax strategies for incentive stock options and AMT Triggering the alternative minimum tax isn’t the end of the world, but you don’t want to do it by accident. Exercise ISOs early in the year to manage or avoid AMT To get long-term capital gains tax treatment, you need to hold ISOs through the end of the year of exercise.

in 2026, the eligibility age will be adjusted to 46. Tax-Advantaged Savings : Contributions to ABLE accounts are made with after-tax dollars, but the earnings on the account grow tax-free. Withdrawals are also tax-free if they are used for qualified disability expenses. With the passing of Secure Act 2.0,

If you have incentive stock options, you’ve probably heard of the alternative minimum tax (AMT). Essentially, the alternative minimum tax is a prepayment of taxes. The credit reduces your tax liability to reflect prepaid tax. Early sales of ISOs are taxed in the regular tax system.

But while it’s possible to retire at 50 and have plenty of time left in life to have new experiences, it takes careful planning and a will of steel. That means understanding the stock market, planning for debt and savings, and investing in yourself through education or entrepreneurial ventures. Your retirement plan shouldn’t be.

This is a major advantage as assets can be sold/diversified right away without tax implications. Developing an asset allocation and investment plan that suits you , which may be different than who left you the inheritance. Concentrated holdings with an emotional attachment (often blue-chip stocks) can derail an investment plan.

For founders, employees, and executives with stock-based compensation, an 83(b) election can be a powerful taxplanning tool. When you make an 83(b) election, you’re opting to pay tax on unvested shares now, instead of when the stock vests. In tax lingo, this is known as substantial risk of forfeiture.

Guest: Megan Gorman, Founder and Managing Partner of Chequers Financial Management , a female-owned, high-net-worth tax and financial planning firm based in San Francisco. ” Megan Gorman and I discuss: How Megan draws on her background as an attorney and her passion for tax strategy when advising high-net-worth clients.

At first glance, you wouldn’t think this news matters that much as most small businesses don’t pay Interest/Dividends tax. In 2022 the rate is 5%, and then 4% in 2023, 3% in 2024, 2% in 2025, 1% in 2026, and then completely repealed after 2026. So, what’s changing?

6 tax strategies for incentive stock options and AMT Triggering the alternative minimum tax isn’t the end of the world, but you don’t want to do it by accident. Exercise ISOs early in the year to manage or avoid AMT To get long-term capital gains tax treatment, you need to hold ISOs through the end of the year of exercise.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. The lower the tax rate, the more attractive the Roth contribution becomes relative to a pre-tax contribution.

2019 Year-End Planning Letter. Each year, we send a letter to clients to help guide year-end planning discussions and to offer ideas for them to consider with their other advisors. Market conditions may be volatile, but our planning efforts are, as always, focused on stability and consistency. Fri, 11/01/2019 - 13:44.

Whether you’re in venture capital, private equity, or angel investing, it’s important to understand the tax implications of your investment income. One of the unique characteristics of carried interest is that it is taxed as a capital gain rather than ordinary income. K-1 forms are reported on an individual’s tax return.

The company’s recent financial performance and looming tax increases have raised concerns among investors and industry analysts. New Tax Policies Add Financial Pressure As if the sales slump wasn’t enough, LVMH now faces an additional financial burden. to about 10%.

TaxPlanning – Have necessary steps been taken toward filing required business and individual tax returns, so they get filed on time? The type of business will determine the tax consequence. There are five general types of business taxes and tax changes that can be applied. Income Tax. Estimated Tax.

Most recently, Intel announced layoffs impacting 15% of the workforce with a plan to cut $10 billion in total costs. So, if you separate from the company near the end of the year, earning a full year of salary plus severance payouts, you could be pushed into a higher tax bracket. Taxplanning for a transition out of Intel is critical.

However, given the high value of wealth, it becomes all the more critical for high-net-worth individuals to plan their finances optimally. Estate planning is one of the key components of financial planning these individuals need to focus on. Business succession: Many high-net-worth individuals are business owners.

By 2026, this figure is expected to more than double to 5-7 percent. This falls in line with the company’s target dividend payout ratio of 30-50 percent of the annual standalone PAT (Profit After Tax). Coming to the CAPEX plans of the company, they are seeking to invest ₹1,500 crores in the next three years. ROCE (%) 24.79

The article concludes with a highlight of future plans and a summary. Future Plans of Polycab India The management has given a large target of 20,000 crores of sales by 2026. The post Fundamental Analysis Of Polycab India – Financials, Future Plans & More appeared first on Trade Brains.

A highlight of the future plans and a summary conclude the article at the end. Overall, the Automobile Component Manufacturers Association (ACMA) projects the Indian auto-ancillary sector to touch $ 200 billion in revenues by 2026. The profit-after-tax margin has remained relatively low. Future Plans of Minda Corporation.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content