This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Keller will step down on April 30, 2026, with the Board planning a search for his successor in the coming year. In a LinkedIn post, Keller wrote that leading well means leaving well.

(kitces.com) Estate planning Four things to consider in anticipation of 2026. investmentnews.com) Retirement It's inevitable we will see more older workers. klementoninvesting.substack.com) The reasons why people un-retire. financial-planning.com) Wealth.com's Ester will help you read estate planning documents.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

We also have a number of articles on retirement planning: New research suggests that while the average senior will amass hundreds of thousands of dollars in health care expenses in retirement, the net cost they have to pay is not nearly as high.

Keller will step down on April 30, 2026, with the Board planning a search for his successor in the coming year. In a LinkedIn post, Keller wrote that leading well means leaving well.

1, 2026 and becomes a big problem for reactive RIAs who fail to help clients take action now." kitces.com) Social Security retirement ages are always a political decision. (thereformedbroker.com) 2025 If nothing changes legislation-wise, there will be a run on estate planning going into 2025. advisorperspectives.com)

I also noted: No cohort is monolithic - some people will age-in-place until they pass away, others will move in with family (or family will move in with their parents), and some will move to retirement communities. The leading edge of the Baby Boom generation is currently 75 (born in 1946), and these people will be turning 80 in 2026.

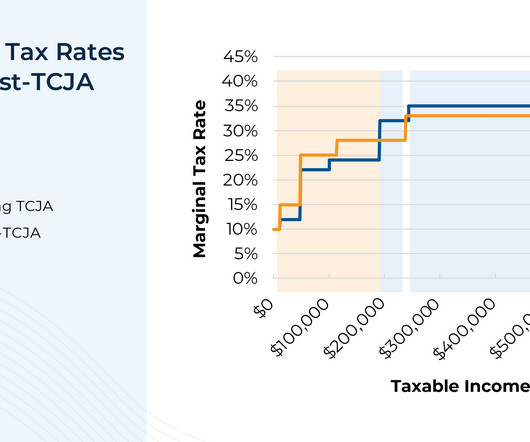

And although TCJA's reputation as a broad tax cut might give the impression that everyone's tax rates would increase after its expiration, comparing the current Federal tax brackets with their estimated post-TCJA equivalents shows that a fair number of households will actually see their tax rates decrease.

Watch Danny Boyd of CinemaStix’s video (above) about the challenges of making a flick about a retired hitman. Chapter 5 is confirmed , and heading to theaters in 2026, which I wouldn’t want to bet against. But it almost wasn’t made at all. John Wick 4, which came out this summer, did $432.2 million at the box office.

Early retirement has become a popular financial goal. Even if you never retire early, just knowing that you can is liberating! Can You Really Retire at 50? Can You Really Retire at 50? Table of Contents Can You Really Retire at 50? FAQs on Retiring Early at 50 It’s a big bold claim – retire at 50?

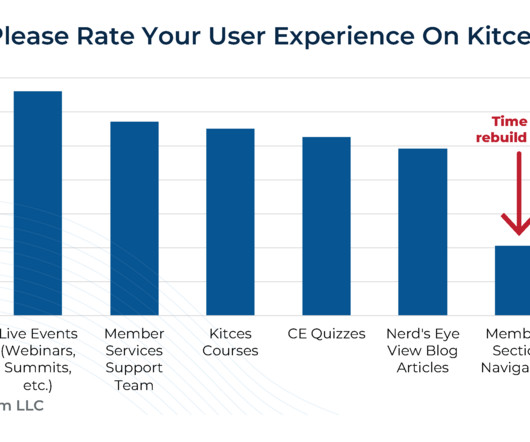

And also make it easier for us to redesign the Nerd's Eye View blog side of the website as well, in 2026!) Which means over the next 12 months, we're going to rebuild it all from scratch, with a modern technology foundation that will allow us to better scale over the next decade.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033.

riabiz.com) Taxes How pre-tax retirement contributions provide flexibility down the road. kitces.com) Tax strategies if the TCJA expires in 2026. (riabiz.com) Charles Schwab ($SCHW) is mothballing the Institutional Intelligent Portfolios platform.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

Many states also exempt retirement income, which may include Social Security. However, retirement income is generally included for income related monthly adjustment amount (IRMAA) computations to determine if supplemental payments are due for Medicare Part B and Medicare Part D premiums.

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. Individual Retirement Accounts (IRAs): Contribute up to $7,000 for 2024 ($8,000 if aged 50+). Capital Gains : If you have appreciated investments, holding onto them until 2026 can help you defer taxable gains.

For example, if you work for a company and leave due retirement, death, disability, or due to a family emergency or a health issue, your employer may be willing to offer you a post-termination grace period (or another alternative, like speeding up the vesting schedule). That being said, there may be some exceptions.

just upended retirement planning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Those born between 1951 – 1959 can delay taking money from retirement accounts in their own name until 73. The Secure Act 2.0

This means if Congress does nothing, we will revert to 2017 tax rules for the 2026 tax year. The importance of the standard deduction for retirees is that it completely offsets a corresponding amount of withdrawals from tax deferred retirement accounts. Tax diversification also remains an important strategy as we save for retirement.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement. One option is to contribute to a Roth IRA.

Jump-starting (or catching up on) retirement savings by investing the money in a brokerage account. Inherited IRA or retirement account. If you inherit an IRA, 401(k), or other type of retirement account from a parent, you must take the inheritance in 10 years. Shoring up college funds. Topping off an emergency fund.

Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income. Contribute to Tax-Advantaged Retirement Accounts Do your best to fully contribute to one or multiple tax-advantaged retirement accounts, such as 401(k), 403(b), or IRAs.

Do not be blindsided when premiums are due. · Disability insurance – According to the Social Security Administration, more than a quarter of today’s 20-year-olds will become disabled before they reach retirement age. Taxes & Retirement Plans Tax law seems to get more complicated every year. Your long-term goals start now.

million for couples), but it will revert to its pre-2018 level of $5 million (adjusted for inflation) in 2026. Essentially, the policy would not provide an instant benefit, but would instead provide an income stream for the employee in the long-term, perhaps in retirement. As of 2023, that exclusion is $12.92 million ($25.84

in 2026, the eligibility age will be adjusted to 46. The beneficiary may only make this contribution if they are not participating in any employer sponsored retirement plan. The disability can be physical or mental, and it must significantly impair the person’s ability to function in daily life.

MLB Commissioner Rob Manfred has said he would be interested in using the automated system in 2026, perhaps with a review system or perhaps to make every call. ” According to long-time umpire Joe West (now retired), “[t]hree ways you can miss a call: lack of concentration, lack of positioning, lack of timing.”

In 2026, the current larger exemption will be reduced from $12,920,000 in 2023 to about $6 million per person ($5 million per person adjusted for inflation). They could also consider contributions to an individual retirement account (IRA) and a health savings account (HSA) , too.

Direct indexing assets, currently at $462 billion, are expected to rise up to $825 billion by 2026, according to Cerulli Associates data that is cited in the article, making its growth forecast the biggest out of ETFs, mutual funds, and separately managed accounts. The service costs $4.99

How much money do your clients need to retire? Fifty years from Fuller’s talk puts us in 2026. With this transformational mindset, clients would no longer need to ask, “Do I have enough money to retire.” How much money do you need? Can you ever have “enough” money? How’s that?

in 2025, 8% in 2026, 7.8% There was mention of the potential pain for people who retire before they can start Medicare for having to find health insurance either through Healthcare.gov or some other way. Healthview projects that the premium will rise 6.3% in 2024 and 6.2% in 2027, and around 6% annually through 2031."

This is in addition to the accelerated vesting provided by Intel retirement rules. However, if you are eligible for retirement at Intel ( here’s a helpful post on the subject ), the APB will be prorated according to the number of full calendar months you worked. For APB, December 31 st is the magic day.

If the sunset occurs, this inflation-adjusted amount, which is currently $13,610,000 as of July 2024 , could be reduced by one-half (after inflation adjustments for 2025 and 2026) starting on January 1, 2026.

Pend-up demand, reopening, healthy corporate and consumer balance sheets, and relatively low tax rates , have economists forecasting real GDP slightly under the long-term average of 2% through 2026. Remember, the Federal Reserve is actively trying to slow the economy by raising rates. US real GDP and forecast.

The Roth IRA (Individual Retirement Account) is a tax-advantaged retirement savings account wherein you contribute after-tax dollars, earn tax-free growth, and make tax-free withdrawals (subject to fulfilment of certain conditions). The Roth IRA is a popular retirement savings vehicle along with the 401(k) and the traditional IRA.

For Canada alone, the expected is 50% of accumulated wealth by 2026. For female clients, the meaning of wealth acquisition, investment, and retirement differ from men’s. Women tend to take breaks in their careers for caregiving, have higher medical expenses, and live longer yet are expected to retire early.

For example, there is going to be an increase in tax rates in 2026 due to the onset of the Tax Cuts and Jobs Act. If you are retired, you must make sure that your financial advisor possesses a strong understanding of Social Security taxes. Annual Roth conversions can be one measure to tackle the changes. Need a financial advisor?

trillion by 2021, it is expected to rise to $23 trillion by 2026. If you have long-term investment goals, such as funding retirement or building wealth over several years, alternative investments can offer unique growth and income potential and diversification benefits over time. between 2015 and the end of 2021.

trillion by 2021, it is expected to rise to $23 trillion by 2026. If you have long-term investment goals, such as funding retirement or building wealth over several years, alternative investments can offer unique growth and income potential and diversification benefits over time. between 2015 and the end of 2021.

In the event the primary trustee passes away, is incapacitated, retires, or is no longer able to fulfill their duties, the secondary trustee can step in. An important thing to remember is that the lifetime gift tax exemption will drop to $6 million by 2026. It is also essential to choose a trustee who is likely to outlive you.

Although Gen Xers are getting older, the majority of people using a financial advisor are retired or pre-retirees. Retirement for those people isn’t about capturing the highest rate of return – you’ve already won the race hopefully by that point – it’s about making that money survive because you are no longer working. Are you really?

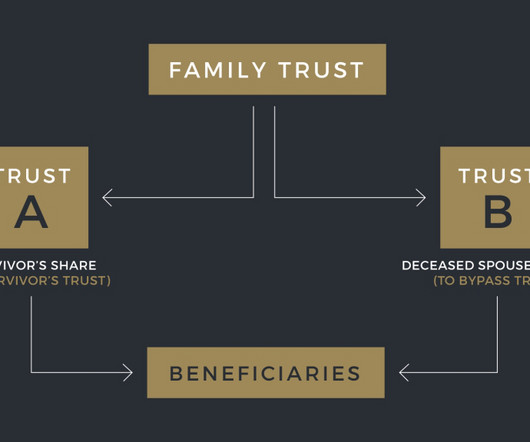

If Bill dies in 2026 without using any of his ~$7.5 Portability is now a permanent feature of federal estate tax law, but if your estate plan still includes AB Trust planning, it might now be doing more harm than good. million estate tax exemption, Alice can file a portability election with the IRS—without needing a separate trust.

The sooner you start saving and the more you save, the faster and larger your retirement nest egg will grow. At Sidoxia Capital Management , we view investing as a marathon, not a sprint. You cannot realize the benefits of compounding without having a long-term time horizon. Subscribe Here to view all monthly articles.

In this guide, we’ll explore the key tax changes in effect for 2025, how theyll influence your filing status, retirement savings, investment, and estate planningand offer strategic advice to help high-income and high-net-worth individuals prepare more effectively for upcoming coming tax changes. Minimizes taxes if rolled over promptly.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content