This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

We also have a number of articles on retirementplanning: New research suggests that while the average senior will amass hundreds of thousands of dollars in health care expenses in retirement, the net cost they have to pay is not nearly as high.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

Attorneys are telling us that 2024 is the time to review and change your estate plan as the lines may be out the door in 2025 for taxpayers wanting to make last minute changes to take advantage of the higher exemption amount. Lastly, I allocate the retirementplan contributions between Roth and Traditional 401(k) accounts.

would keep the age 50 catch-ups and allow new ones: 401(k) & 403(b) plans: starting in 2025, the catch-up contribution will become the greater of $10,000 or 150% of the catch-up limit for individuals between age 60 – 63. Starting in 2026, the catch-up will be indexed by inflation. The Secure Act 2.0 The Secure Act 2.0

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

Taxes & RetirementPlans Tax law seems to get more complicated every year. As the Tax Cuts and Jobs Act (2017) sunsets in 2026, taxes will only become more complex. For low-income earners, look at marketplace policies that could offer you tax credits or subsidized state-run programs.

The stock market has returned an average of between 9% and 11% over the past 90 years and that’s the kind of growth that you’ll need to tap into if you want to retire at 50. Your retirementplan shouldn’t be. Get in touch with an Independent Financial Professional to see if you're on track to meet your retirement goals.

Effective ways to achieve this include: For employees : If your employer offers this option, request that your year-end bonus be deferred to January 2026. Capital Gains : If you have appreciated investments, holding onto them until 2026 can help you defer taxable gains.

in 2026, the eligibility age will be adjusted to 46. The beneficiary may only make this contribution if they are not participating in any employer sponsored retirementplan. The current tax law also allows for a rollover from a 529 plan to an ABLE account up to the annual limit amount. With the passing of Secure Act 2.0,

Additional ways to fund a Roth IRA For workers with access to a 401(k) or other qualified retirementplan, a designated Roth account can be a fantastic opportunity to create a larger Roth account balance for retirement. Without action by Congress, 2026 could usher in significantly higher tax rates. Is there a better way?

In 2026, the current larger exemption will be reduced from $12,920,000 in 2023 to about $6 million per person ($5 million per person adjusted for inflation). Tax season has begun, and it’s not too early to think about planning for the 2023 tax year.

in 2025, 8% in 2026, 7.8% Part G Medicare, the one I believe to be the most robust supplemental plan currently costs an average of $1517/yr with projections of 10+% increases over the next few years. "Currently, retirees with modified adjusted income below $97,000 pay $1,979 a year in Part B premiums. in 2024 and 6.2%

For example, there is going to be an increase in tax rates in 2026 due to the onset of the Tax Cuts and Jobs Act. Financial advisors play a pivotal role in helping clients navigate a spectrum of financial matters, from budgeting and investments to healthcare and retirementplanning.

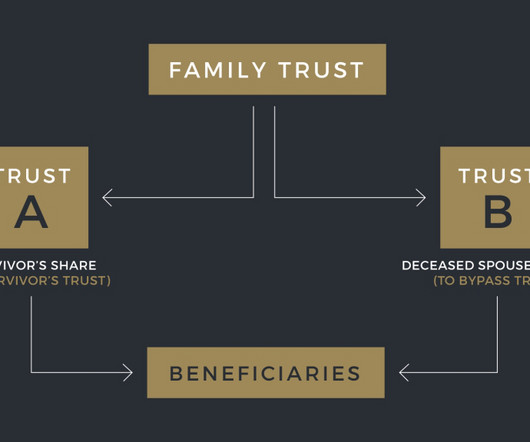

Portability is now a permanent feature of federal estate tax law, but if your estate plan still includes AB Trust planning, it might now be doing more harm than good. To illustrate how portability can simplify and enhance an estate plan, let’s look at Bill and Alice, who have been married for 40 years.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content