This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. For some, this may lead to more taxes paid on capital gains.

Taxplanning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. For some, this may lead to more taxes paid on capital gains.

That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). AGI impacts multiple other tax considerations.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033. The Secure Act 2.0

The stock market has returned an average of between 9% and 11% over the past 90 years and that’s the kind of growth that you’ll need to tap into if you want to retire at 50. Your retirementplan shouldn’t be. Get in touch with an Independent Financial Professional to see if you're on track to meet your retirement goals.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement. Is there a better way?

in 2026, the eligibility age will be adjusted to 46. Tax-Advantaged Savings : Contributions to ABLE accounts are made with after-tax dollars, but the earnings on the account grow tax-free. Withdrawals are also tax-free if they are used for qualified disability expenses. With the passing of Secure Act 2.0,

in 2025, 8% in 2026, 7.8% Part G Medicare, the one I believe to be the most robust supplemental plan currently costs an average of $1517/yr with projections of 10+% increases over the next few years. "Currently, retirees with modified adjusted income below $97,000 pay $1,979 a year in Part B premiums. in 2024 and 6.2%

Step 2: See if the financial advisor conducts an annual tax review Ensuring that your financial advisor reviews your tax return annually is a crucial step in maximizing your financial benefits. An effective financial advisor should be proactive in reviewing your taxplan before the year-end.

Even if a client believes they would not be subject to estate or gift tax under current law, you may want to re-examine the value of their assets to determine whether they exceed a lower exemption amount. Tax season has begun, and it’s not too early to think about planning for the 2023 tax year.

By Ryan Egolf, EA, Senior Tax Planner As the New Year quickly approaches, it’s time to put a bow on your 2023 financial plan. In some cases, those payments are tax-free. Check into your employer’s short- and long-term disability plans, as they are usually the most affordable options.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

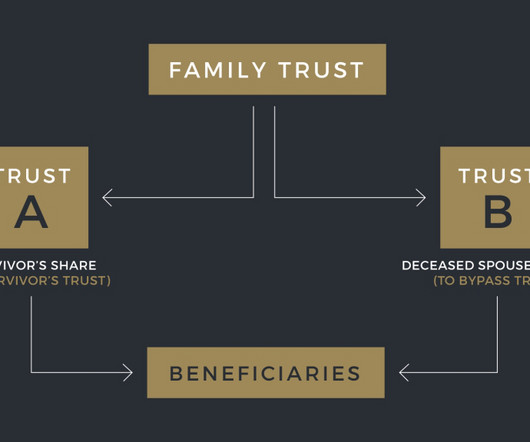

If so, there’s a good chance your plan includes the classic “AB Trust” structure, which—prior to 2011—was the primary way for married couples to double the value of their federal estate tax exemptions. But in 2011, the concept of “portability” changed the estate planning landscape. This election allows her to add Bill’s ~$7.5

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content