This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

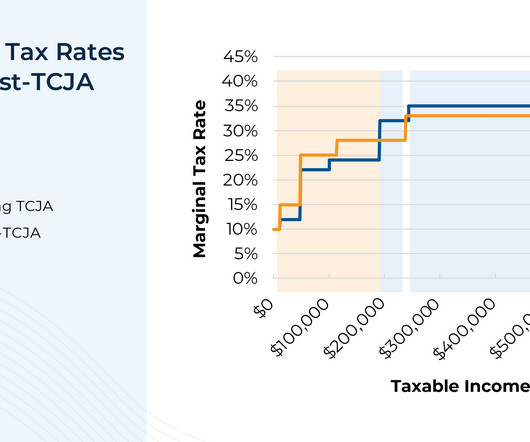

The Tax Cuts and Jobs Act (TCJA), passed in 2017, was one of the most extensive pieces of tax legislation to be passed in the last 30 years, touching many aspects of individual, corporate, and estate tax.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. For some, this may lead to more taxes paid on capital gains.

Tax planning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. In this episode, we talk about five strategies you can use during tax season to create opportunities to help you reach your financial goals.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Early retirement has become a popular financial goal. Even if you never retire early, just knowing that you can is liberating! Can You Really Retire at 50? Can You Really Retire at 50? Table of Contents Can You Really Retire at 50? FAQs on Retiring Early at 50 It’s a big bold claim – retire at 50?

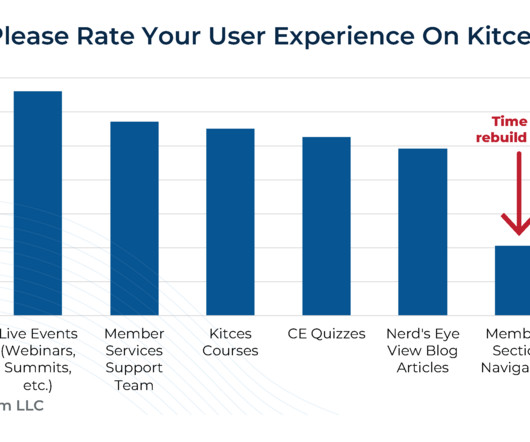

And also make it easier for us to redesign the Nerd's Eye View blog side of the website as well, in 2026!) Which means over the next 12 months, we're going to rebuild it all from scratch, with a modern technology foundation that will allow us to better scale over the next decade.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. For some, this may lead to more taxes paid on capital gains.

riabiz.com) Taxes How pre-taxretirement contributions provide flexibility down the road. kitces.com) Tax strategies if the TCJA expires in 2026. (riabiz.com) Charles Schwab ($SCHW) is mothballing the Institutional Intelligent Portfolios platform.

Key Takeaways: Even without new legislation, the prospect of higher taxes in the future is still looming. The impact of higher taxes on retirees could be substantial, so staying up to date on the current tax landscape is vital. But even without new legislation, the prospect of higher taxes in the future is still looming.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033.

That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). AGI impacts multiple other tax considerations.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement. The answer may be yes.

This is a major advantage as assets can be sold/diversified right away without tax implications. Jump-starting (or catching up on) retirement savings by investing the money in a brokerage account. Inherited IRA or retirement account. Prolong the benefits of tax-deferred growth as long as possible (all else equal).

in 2026, the eligibility age will be adjusted to 46. Tax-Advantaged Savings : Contributions to ABLE accounts are made with after-tax dollars, but the earnings on the account grow tax-free. Withdrawals are also tax-free if they are used for qualified disability expenses. With the passing of Secure Act 2.0,

Other pay : Certain employees can be eligible for “pay in lieu of redeployment” (9 weeks) and an “additional separation bonus” (8 weeks) It’s important to note that severance payouts are taxed as ordinary income in the year of payout. Tax planning for a transition out of Intel is critical.

Direct indexing assets, currently at $462 billion, are expected to rise up to $825 billion by 2026, according to Cerulli Associates data that is cited in the article, making its growth forecast the biggest out of ETFs, mutual funds, and separately managed accounts. The service costs $4.99

in 2025, 8% in 2026, 7.8% There was mention of the potential pain for people who retire before they can start Medicare for having to find health insurance either through Healthcare.gov or some other way. Healthview projects that the premium will rise 6.3% in 2024 and 6.2% in 2027, and around 6% annually through 2031."

Pend-up demand, reopening, healthy corporate and consumer balance sheets, and relatively low tax rates , have economists forecasting real GDP slightly under the long-term average of 2% through 2026. The good news is that the US economy is in pretty good shape. US real GDP and forecast. What should you do until inflation subsides?

Step 2: See if the financial advisor conducts an annual tax review Ensuring that your financial advisor reviews your tax return annually is a crucial step in maximizing your financial benefits. An effective financial advisor should be proactive in reviewing your tax plan before the year-end.

trillion by 2021, it is expected to rise to $23 trillion by 2026. If you have long-term investment goals, such as funding retirement or building wealth over several years, alternative investments can offer unique growth and income potential and diversification benefits over time. between 2015 and the end of 2021.

trillion by 2021, it is expected to rise to $23 trillion by 2026. If you have long-term investment goals, such as funding retirement or building wealth over several years, alternative investments can offer unique growth and income potential and diversification benefits over time. between 2015 and the end of 2021.

That being said, you will still need to be cognizant of when they vest, how they can impact your tax bill, and when may be the best time to sell or hold shares. Taxes and Portfolio Concentration: The Importance of Managing Your RSUs RSUs are relatively simple to manage when compared to employees stock options.

Even if a client believes they would not be subject to estate or gift tax under current law, you may want to re-examine the value of their assets to determine whether they exceed a lower exemption amount. Tax season has begun, and it’s not too early to think about planning for the 2023 tax year.

By Ryan Egolf, EA, Senior Tax Planner As the New Year quickly approaches, it’s time to put a bow on your 2023 financial plan. In some cases, those payments are tax-free. One of the greatest things about insurance is the liquidity it provides when needed most and tax efficiency. Roth contributions are also dependent on MAGI.

just upended retirement planning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Those born between 1951 – 1959 can delay taking money from retirement accounts in their own name until 73. The Secure Act 2.0

In this guest post, Harness Tax Advisory Council member, Griffin Bridgers, J.D., covers some of the top estate planning trends that tax advisors should be tracking during the second half of 2024. On the estate planning front, chief among these potential changes is the sunset of the gift and estate tax basic exclusion amount for U.S.

For individuals, a permanent life insurance plan can play a key role in estate planning by helping reduce estate taxes. Offset Taxes in Estate Planning Estate taxes can be a problem for high-net-worth individuals passing on more than the IRS estate tax exclusion, after which the tax rate on transferred money is 40%.

The Roth IRA (Individual Retirement Account) is a tax-advantaged retirement savings account wherein you contribute after-tax dollars, earn tax-free growth, and make tax-free withdrawals (subject to fulfilment of certain conditions). If you want to make tax-free withdrawals from your Roth IRA, you must be 59.5

It is a process that can allow high-net-worth individuals to transfer their wealth to future generations while minimizing tax burdens, maximizing financial security, and protecting their hard-earned money. Estate planning can be hard to navigate with international laws, global market fluctuations, tax treaties, and legal systems.

In this guide, we’ll explore the key tax changes in effect for 2025, how theyll influence your filing status, retirement savings, investment, and estate planningand offer strategic advice to help high-income and high-net-worth individuals prepare more effectively for upcoming coming tax changes. That said, U.S.

Although Gen Xers are getting older, the majority of people using a financial advisor are retired or pre-retirees. Retirement for those people isn’t about capturing the highest rate of return – you’ve already won the race hopefully by that point – it’s about making that money survive because you are no longer working. . #1

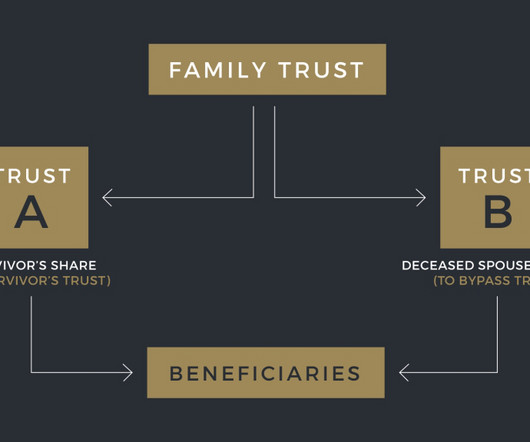

If so, there’s a good chance your plan includes the classic “AB Trust” structure, which—prior to 2011—was the primary way for married couples to double the value of their federal estate tax exemptions. If Bill dies in 2026 without using any of his ~$7.5 But in 2011, the concept of “portability” changed the estate planning landscape.

The sooner you start saving and the more you save, the faster and larger your retirement nest egg will grow. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content