This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I’m currently maxing out my 401k, Roth IRA, and have roughly $45k in a taxable brokerage account. Via my company’s ESOP, my company’s stock has become 20% of my brokerage account even after selling a good chunk steadily over the past several years. A reader asks: I’m a 30 year old living in Brooklyn making $175/year.

On the other hand, the term "financial advice" often refers to much more than assetallocation and wealth management. This principle extends across many aspects of a firm's value proposition, from client newsletters to account log-in frequency to other common metrics of interest.

tonyisola.com) Age is just one factor when it comes to your assetallocation. mrmoneymustache.com) Why you need to account for your Treasury income on your state taxes. fastcompany.com) What to consider when rolling over a 401(k) account to an IRA. readthejointaccount.com) When a second home makes financial sense.

podcasts.apple.com) Assetallocation Small assetallocation shifts don't matter much in the long run. awealthofcommonsense.com) Why assetallocation matters. barrons.com) Why couples could benefit from separate and joint accounts. semafor.com) Retirement Cognitive decline is inevitable.

Following the long run-up in the US equity markets since the bottom of the 2008–2009 financial crisis, many investors with taxable investment accounts have likely found themselves with high embedded gains in their portfolios. While the gains signal portfolio growth, they also create challenges for ongoing management.

standarddeviationspod.com) Christine Benz and Amy Arnott talk assetallocation and more with Matt Krantz. riabiz.com) Retirement accounts On the downside of holding non-traditional assets in an IRA. investmentnews.com) Why funds in pre-tax retirement accounts need to be adjusted for taxes.

(mrzepczynski.blogspot.com) There's not much to see in tactical assetallocation ETF performance. researchaffiliates.com) How does index fund ownership affect firm accounting quality? insights.factorresearch.com) Active share doesn't tell us anything about future performance. papers.ssrn.com).

What is in your control : Your Portfolio : You want to create something robust enough to withstand drawdowns and recessions; not necessarily the best possible set of assets but the ones you can live with day in and day out. This includes a broad AssetAllocation including full Diversification of asset classes, geographies, etc.

peterlazaroff.com) Investing There's no magic rule for assetallocation. crr.bc.edu) Saving for college How much should you save in 529 accounts? (podcasts.apple.com) Peter Lazaroff talks with Manisha Thakor author of “MoneyZen: The Secret to Finding Your “Enough.”

Every document that considers the facts around any particular asset class will invariably include that disclaimer, but constructing a portfolio consisting of a mix of equities, fixed income, and other assets requires investors and advicers to make some fundamental assumptions around long-term expected returns and correlations between assets.

Review your accounts and assess the extent of the damage that has been done. Investors who are well-diversified may be hurt but generally not to the extent of those who are highly allocated to stocks. Review your assetallocation . Step back, take a deep breath and relax. Take stock of where you are . Go shopping .

We also answered questions about 2025 retirement account limits, Coast FIRE strategies, when to take money off the table from the stock market, how to account for pension and Social Security income during retirement and how other economies impact the U.S.

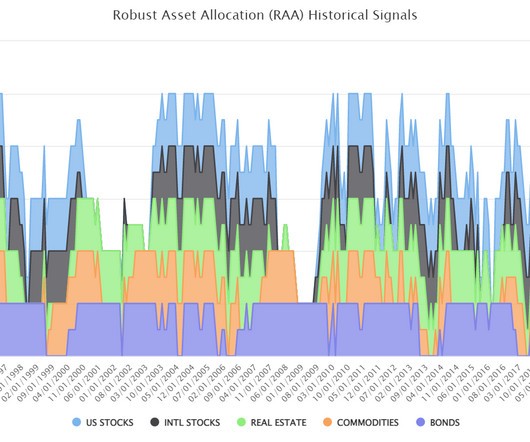

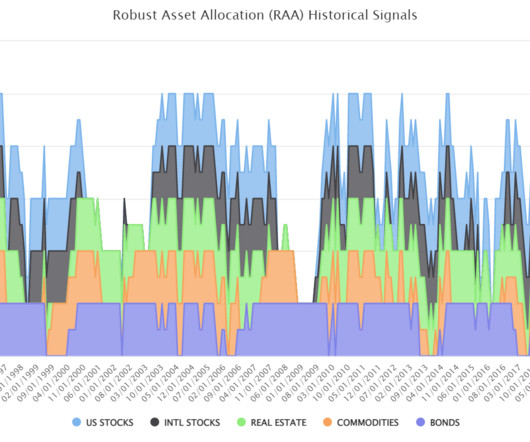

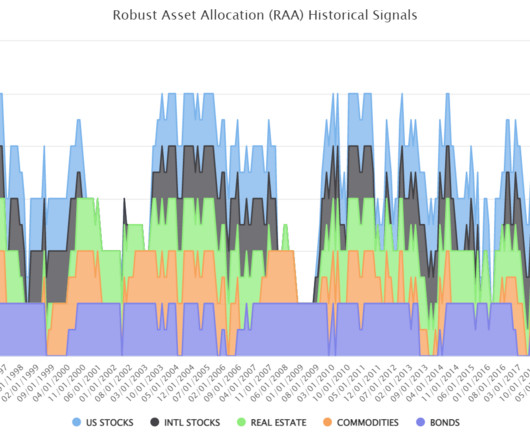

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. If you are an advisor and want help implementing our models, please get in touch with Ryan Kirlin.

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. If you are an advisor and want help implementing our models, please get in touch with Ryan Kirlin.

Hypothetical simulation assumes $1M was invested on 12/31/2004, 50% in SPY and 50% in AGG, portfolio was never rebalanced, dividends not reinvested, and no other contributions/withdrawals in the account. In another words, if your assetallocation is 60% stocks and 40% bonds, the current weighted average yield is 2.19%.

However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. Assetallocation aims to balance risk and reward through a portfolio composition of different kinds of assets. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

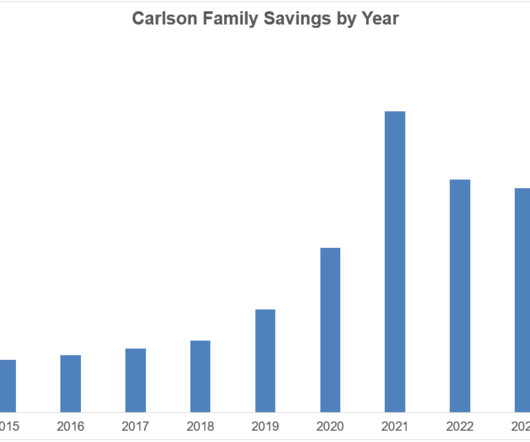

Just a collection of the holdings in our various accounts along with some simple calculations — net worth, annual retirement contributions, assetallocation, how much we’re saving each year, etc. Guess I’m old school and, yes, kind of a personal finance dork. I can’t help it. It’s nothing fancy.

alphaarchitect.com) Performance The performance of tactical assetallocation mutual funds has been no great shakes. evidenceinvestor.com) Research The accounting treatment of intangible investments is too conservative. Inflation Hedging inflation is harder than it looks.

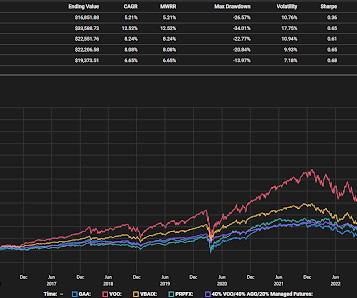

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

What to Do Instead: Stick to fundamentals: Learn about assetallocation, risk management, and diversification before investing. Keep it separate: Use a high-interest savings account or liquid mutual fundsbut not your main spending account. Use it only for real emergencies: If you have to ask, Is this an emergency? ,

Reevaluate Your AssetAllocation If watching your investment portfolio fluctuate causes anxiety, your current allocation might be too aggressive. You can reduce your stock exposure and increase investments in fixed income options, such as cash or bonds, within tax-advantaged accounts (like a 401(k), IRA, or Roth IRA).

Most individuals choose to have a certain amount of money transferred from each paycheck directly into their investment accounts so they don’t even have the option to spend it. Set Up Another Retirement Account Individual Retirement Accounts (IRAs) may offer tax advantaged savings as well. Again, I wish I had that crystal ball!

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The war in Ukraine is causing even more uncertainty. Rodrigo is now available. All investments involve risk.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . The themes and topics discussed include: The performance of various markets and asset classes over recent years and since the onset of the Ukraine conflict. Fri, 03/18/2022 - 06:42. Watch the Video.

Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. View all accounts as part of a total portfolio. This means IRAs, your 401(k) , taxable accounts, mutual funds , individual stocks and bonds, etc. Costs matter. Low cost index mutual funds and ETFs can be great core holdings.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

Review risk tolerance and current assetallocation strategy It’s important to ensure your clients’ portfolios align with their risk tolerance because taking too much risk can negatively impact their ability to navigate market fluctuations. You can help them start the year right by conducting a retirement checkup.

And my dad had always said, as many young kids get this advice, doctor, lawyer, accountant, engineer. SALISBURY: And accountant seemed like a reasonable option. And I kind of stumbled my way into accounting. That background of being an accountant was just great bedrock training. RITHOLTZ: Sure. Very different fields.

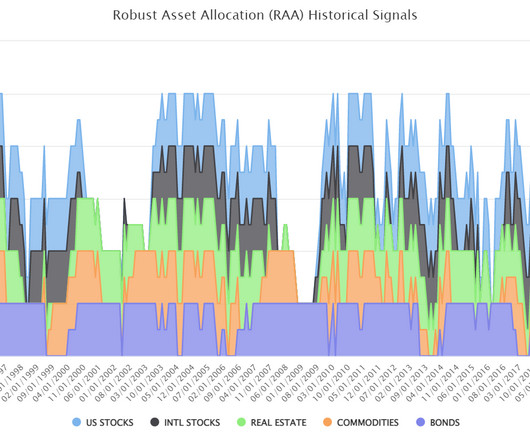

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. If you are an advisor and want help implementing our models, please get in touch with Ryan Kirlin.

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. If you are an advisor and want help implementing our models, please get in touch with Ryan Kirlin.

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. Our Advisor portal is available [.]

Provide insights on assetallocation and risk management. Their role includes: Providing accountability Keeping you focused on long-term goals. Managing Market Volatility Market fluctuations can impact your portfolio and long-term goals. A financial advisor can: Help you maintain a disciplined investment strategy.

I created this list of financial advisors for small accounts (less than $300,000 in assets) because there are alot of schmucks out there hawking crap products to people with portfolio of this size, and I don’t think it’s fair. Transform Retirement www.transformretirement.com Avg account size: Approx. 56 Capital Partners www.56capitalpartners.com

The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Those born between 1951 – 1959 can delay taking money from retirement accounts in their own name until 73. Remaining funds can be invested in a brokerage account. The Secure Act 2.0

Early on in my savings journey I prioritized tax-deferred retirement accounts over all else. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account. It’s easy to automate. Plus, I like the fact that it’s difficult to get the money out of these ac.

Callie Cox, our new Chief Market Strategist at Ritholtz Wealth, joined me on the show this week to discuss questions about the potential for a recession, what the Fed should do now, going all in on the Nasdaq 100 in your retirement accounts and how markets move in off hours. Further Reading: What’s the Worst Long-Term Return For U.S.

Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income. Contribute to Tax-Advantaged Retirement Accounts Do your best to fully contribute to one or multiple tax-advantaged retirement accounts, such as 401(k), 403(b), or IRAs.

Depending on your financial situation and the type of asset you inherit, your options may differ. Inherited cash, stocks, or a brokerage account. Inheriting money or taxable investment accounts has some big benefits. Further, many beneficiaries are eligible for a step-up in basis on eligible assets.

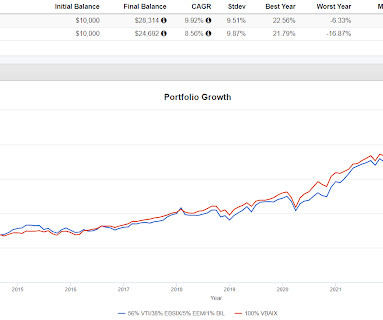

which accounts for about half of it's total outperformance since inception. Circling back to model ETF portfolio mentioned at the top of this post, the assetallocation was as follows. Right out of the starting block for GHTA, VBAIX fell off a small cliff and GHTA managed to avoid that decline.

Minimize Risk Implement an investment strategy that takes market risk, inflation risk and time horizon into account. As you get closer to retirement your assetallocation should change. Additionally, be sure to account for the tax confusions of different investments in taxable brokerage accounts and retirement accounts.

Further Reading: How Individual Retirement Accounts Changed the Stock Market Forever 1Assets did fall and then stagnated coming out of the Great Financial Crisis but that was a period with.

Overindulgence in information can lead to poor decisions, and excessive monitoring of your retirement account balance can result in stress. Checking your retirement account balance too often can have a psychological impact on you. Therefore, exploring the optimal frequency for checking your retirement account is essential.

A reader asks: Is it crazy to be 100% in stocks from age 32 to sometime in my 50s for my retirement accounts? And another reader asks a similar question: I don’t get why people work a 30+ year career while investing in stocks only to glide path into a heavier bond allocation around retirement.

Beef up your emergency fund – A good rule of thumb is to have between 3-6 months’ worth of expenses set aside in a high-yield savings account. The catch-up contribution (available for anyone over age 50) remains the same at $7500 for elective deferral account and $1k/year for Traditional and Roth IRAs.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content