This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By Jake Anderson, CFP ® , Wealth Planner When helping clients begin retirementplanning, the same questions often arise: What should my retirementplan look like? Your lifestyle, goals, family situation, and risk tolerance will give a unique signature to your retirementplan. How much should I be saving?

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Consider early retirement tax planning. Educate yourself about finances.

At 50 though, you do need to have some context for how viable your idea of retirement is. Certainly not from that account balance, a bunch of cash flow positive real estate could be a different story. Not sure I will participate because of how uninteresting our accounts are. Time and health are more important than money.

Hypothetical simulation assumes $1M was invested on 12/31/2004, 50% in SPY and 50% in AGG, portfolio was never rebalanced, dividends not reinvested, and no other contributions/withdrawals in the account. In another words, if your assetallocation is 60% stocks and 40% bonds, the current weighted average yield is 2.19%.

Early on in my savings journey I prioritized tax-deferred retirementaccounts over all else. I like the ease and simplicity of 401k contributions coming out of my paycheck before it ever even touches my checking account. The set-it-and-forget-it nature of a workplace retirementplan is one of my favorite features.

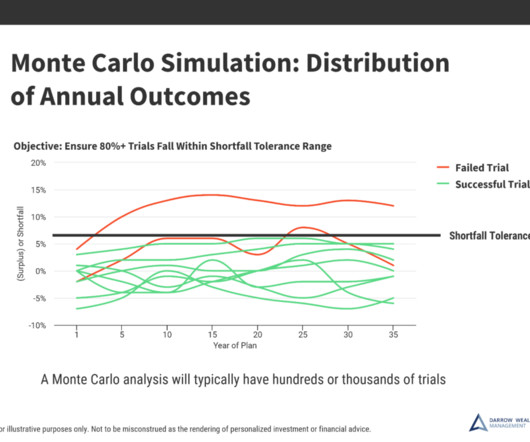

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. View all accounts as part of a total portfolio. This means IRAs, your 401(k) , taxable accounts, mutual funds , individual stocks and bonds, etc. Costs matter. Low cost index mutual funds and ETFs can be great core holdings.

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

As someone saving for retirement , what should you do now? During the financial crisis there were many stories about how our 401(k) accounts had become “201(k)s.” The PBS Frontline special The Retirement Gamble put much of the blame on Wall Street and they are right to an extent, especially as it pertains to the overall market drop.

This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! ) By rule, all matching contributions are made to a traditional 401(k) account regardless of whether some or all of your contributions are in the Roth 401(k).

Their role extends beyond investment managementthey can help with: RetirementPlanning : Structuring your assets to support your desired lifestyle. Estate Planning : Ensuring your wealth is passed on according to your wishes. Provide insights on assetallocation and risk management.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirementaccounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

A Contributory IRA, otherwise known as a traditional IRA , is a retirement savings account that allows individuals to make contributions from their earned income. Contributory IRA accounts are held by custodians, such as banks, brokerage firms, and mutual fund companies.

Minimize Risk Implement an investment strategy that takes market risk, inflation risk and time horizon into account. As you get closer to retirement your assetallocation should change. Additionally, be sure to account for the tax confusions of different investments in taxable brokerage accounts and retirementaccounts.

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Compounding interest can be power for Lisa.

I created this list of financial advisors for small accounts (less than $300,000 in assets) because there are alot of schmucks out there hawking crap products to people with portfolio of this size, and I don’t think it’s fair. Transform Retirement www.transformretirement.com Avg account size: Approx.

Look at those discretionary expenses that might not be necessary (cable TV, that Hulu account you never watch, the Pandora music you don’t listen to, etc). Nothing will nuke your financial plan like high credit card debts and other high rate liabilities. AssetAllocation and Goals. Kill high interest rate debts.

A point we've been making here for ages is that with an adequate savings rate, appropriate assetallocation and the ability to avoid succumbing to panic, an investor should be able to have retirementplan success as defined above. They've generally captured what the market has done since the inception of the account.

Overindulgence in information can lead to poor decisions, and excessive monitoring of your retirementaccount balance can result in stress. Checking your retirementaccount balance too often can have a psychological impact on you. When should you check your retirementaccount balance?

Investment strategy: Determine assetallocation and investment vehicles aligned with risk tolerance and financial goals. Retirementplanning: Calculate retirement needs and contribute regularly to retirementaccounts. What Could Happen if You Don’t Have a Financial Plan?

At 50, you can put more in to various accounts (55 for HSAs), that would stay the same but then at 62-64 which I guess is still be worked on, you'd be able to contribute quite a bit more to help catch up. While most of that is fantastic, you might not want to put more into qualified accounts in your 60's.

One thing that I have craved for investors is a tool that allows you to sync all your financial accounts – your investment portfolio, checking and savings accounts, credit cards and other loan accounts – in one place, and then provides an investment-related analysis of your entire portfolio.

which accounts for about half of it's total outperformance since inception. Circling back to model ETF portfolio mentioned at the top of this post, the assetallocation was as follows. Right out of the starting block for GHTA, VBAIX fell off a small cliff and GHTA managed to avoid that decline.

A lot of this depends on which market you look at and what time horizon, but the global stock market has generated nowhere near 10% when you account for real factors like inflation, taxes and fees. And they’re the things that can blow up a retirementplan if you don’t make conservative estimates that properly account for them.

For people nearing retirement, these challenges can be even more daunting. A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors.

Don’t stress out about every headline, stress test your retirementplan instead.Markets move every day and the news cycle is 24-7. Even if actual average returns meet targets over time, market volatility can still derail your portfolio and retirementplans. The only factor is a static average annual return.

For the last couple of years, I think a lot of people gravitated to just using market cap weighted in their accounts, that seems like it has been the conversation and for 2023 and 2024 the returns for MCW have been great. MCW also did great in 2021, 2020 and 2019. Occasionally of course, MCW gets pasted.

Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. For example, you may invest in tax-advantaged accounts, such as a traditional IRA, because it will offer the most tax benefits.

Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. For example, you may invest in tax-advantaged accounts, such as a traditional IRA, because it will offer the most tax benefits.

Many people invest in their company-sponsored 401(k)s but only sometimes take the time to review the investments within the account. Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. We make it easy by matching you to vetted advisors that meet your unique needs.

LCSIX is a multi-manager fund which probably accounts for some of its 2.18% expense ratio. I've been critical of the actual FIG ETF, the Simplify Macro ETF, it is really struggling but I think the fund's idea for assetallocation works for the most part. I trust the standard deviation as being repeatable moreso than the CAGR.

For instance, they can guide you on leveraging employer-sponsored retirementplans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts. A strategic use of tax-advantaged accounts like the HSA can foster investment growth and also ensure tax efficiency.

The Wall Street Journal took what might be a sympathetic approach to 401k investors who might be feeling disillusioned by generally poor performance with the focus being on target date funds which have of course become a major staple of 401k plans. First, it's your retirement, how do you not care enough to engage just a little?

In our planning with clients, we like to employ a “pay yourself first” approach, especially as it relates to retirementplanning. You may have been contemplating starting contributions to a retirementplan, or you may have been contributing small amounts and are worried that you are behind in the game.

Long-term goals typically encompass retirementplanning, wealth preservation and estate planning. Your risk tolerance will influence your investment strategy and assetallocation. Certified Public Accountant (CPA) CPAs specialize in tax planning and accounting.

When applied to investing, many folks may come to the same conclusion that 80% of their returns are generated from only 20% of their assetallocations. Can the 80/20 rule be used for long-term investments and retirementplanning? The 80/20 rule can be helpful when planning for retirement or the long term.

The answer lies in smart and strategic retirementplanning. Gone are the days when retiring at 60 was a one-size-fits-all goal. It’s time to rethink when to start stashing away those savings and how to modify your plan in a world that’s constantly changing. So, how do we tackle this?

Quick disclaimer that I am test driving ISPY in one of my accounts for possible use for clients. I think solving the idea of how to derisk comes down to a couple of things, finding the more reliable derisking effect as well as maintaining the proper assetallocation for the investor in question.

An emergency fund is for those unexpected life events that can eat into your bank account. The investing world can be complex, so do your research about everything from bonds and mutual funds to assetallocation. Once you’ve set up a budget and paid off high-interest debt, it’s time to set up an emergency fund.

Check your credit report : People often neglect to monitor their financial accounts over the summer. Review your credit report following the peak travel season to make sure all your accounts are accurate. It’s a good idea to meet with your plan advisor to strategize about allocating your funds in the new year.

From retirementplanning to market volatility, equity compensation, family expenses, and major life transitions, it’s easy to feel overwhelmed with financial responsibilities. An advisor can answer questions like: When can I fully retire? When and how do I start planning & savings for my kids’ college?

Make funding tax-advantaged accounts a priority Tax-advantaged accounts are specifically designed to help savers build their retirement nest egg. Some common tax-advantaged retirement savings solutions include your 401(k), 403(b), and SIMPLE 401(k) plan. Once in the account, your contributions will grow tax-free.

Risk Tolerance: What is your assetallocation? If you are close to retirement, and you have too much exposure to equities, a retrenchment in the stock market could delay your retirementplans by years. This concept highlights the importance of rebalancing your portfolio as you get closer to retirement.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content